When investors think about artificial intelligence, they tend to focus on what is most visible: AI models, software platforms, semiconductors, and cloud providers. Yet as we move into 2026, one of the most critical constraints on AI growth is not software or chips—it is something far more basic:

The electrical grid.

AI is an energy-intensive technology. Data centers consume enormous amounts of electricity, require near-perfect reliability, and concentrate demand in very specific geographic locations. Even if power generation (nuclear, gas, renewables) keeps pace, the existing grid was not designed for this type of load.

This makes electrical grid and transmission infrastructure one of the most underappreciated investment themes tied to AI—and one of the most durable.

In this article, we focus specifically on grid-focused ETFs, why they matter, how they benefit from AI, and why they deserve attention in 2026 portfolios.

1. Why the Grid Is the Real AI Bottleneck

Power generation often gets the headlines: nuclear plants, uranium, renewables. But electricity is useless if it cannot be delivered reliably and efficiently.

Most North American grids were built:

Decades ago

For centralized power plants

With predictable consumption patterns

Without massive 24/7 industrial-scale loads

AI data centers break all of those assumptions.

What AI Changes

AI infrastructure creates:

Extreme power density (especially for GPUs)

Constant demand (no downtime tolerance)

Localized demand spikes near data center hubs

Grid stability challenges

In many regions, the grid—not power generation—is now the limiting factor for new data center approvals. Utilities are delaying or rejecting projects simply because transmission and distribution systems cannot handle the load.

This is why capital spending is increasingly flowing not just into power plants, but into:

Transmission lines

Substations

Transformers

Grid automation

Energy management systems

And this is where grid-focused ETFs come into play.

2. GRID ETF: Pure Exposure to Grid Modernization

One of the most direct ways to invest in this theme is through GRID.

What GRID Actually Owns

GRID focuses on companies involved in:

Electrical transmission and distribution

Smart grid technologies

Power management systems

Grid automation and monitoring

Electrification infrastructure

Rather than owning utilities themselves, GRID targets the companies that build, upgrade, and manage the grid.

This is a critical distinction.

Utilities are regulated and often slow-growing. GRID, by contrast, holds firms that benefit from capex cycles, not rate approvals.

Why GRID Is Well Positioned for AI

AI-driven grid demand creates three powerful tailwinds for GRID holdings:

1️⃣ Massive Grid Upgrade Spending

Governments and utilities are committing hundreds of billions to grid modernization over the next decade. Much of this spending is non-discretionary—the grid must be upgraded, regardless of economic cycles.

2️⃣ Technology-Driven Grid Complexity

AI loads require:

Real-time monitoring

Advanced load balancing

Redundancy and resilience

This favors companies selling high-margin technology solutions, not just physical hardware.

3️⃣ Long Project Pipelines

Grid projects are multi-year undertakings. Once contracts are awarded, revenue visibility is high, supporting stable cash flows.

GRID effectively turns these structural realities into a diversified equity exposure.

3. PAVE ETF: Broader Infrastructure with Grid Leverage

While GRID is highly targeted, PAVE offers a broader approach.

PAVE is not a pure energy ETF—but that is part of its strength.

What PAVE Includes

PAVE holds companies involved in:

Infrastructure construction

Engineering and materials

Industrial equipment

Transportation and utilities support

Power and transmission infrastructure

Many of its holdings benefit directly from:

Substation construction

Transmission expansion

Data center site development

Grid hardening and resilience projects

Why PAVE Works for Grid Investors

PAVE’s value lies in indirect exposure.

AI-driven grid upgrades require:

Concrete

Steel

Construction equipment

Engineering services

Industrial components

PAVE captures this second-order demand, which is often overlooked when investors focus only on “energy stocks.”

It also provides:

Broader diversification

Less thematic concentration

Exposure to government infrastructure bills

For investors who want grid exposure without betting exclusively on energy technology, PAVE serves as a core infrastructure allocation.

4. Government Spending: A Structural Tailwind

One reason grid ETFs are attractive is that government spending aligns with AI needs.

Across North America and Europe, policy priorities include:

Grid resilience

Electrification

Energy security

Climate transition

National competitiveness in AI

Grid upgrades are politically favorable:

They create jobs

Improve reliability

Support industrial growth

Enable AI and digital infrastructure

Unlike speculative tech spending, grid investment is bipartisan and strategic.

This creates a rare alignment:

Private sector demand (AI data centers)

Public sector funding (infrastructure programs)

GRID and PAVE are positioned at the intersection of both.

5. AI Data Centers and Demand Concentration

One unique challenge of AI is demand concentration.

Traditional electricity demand is spread across millions of homes and businesses. AI data centers, by contrast:

Consume as much power as small cities

Are clustered geographically

Require dedicated transmission capacity

This forces utilities to:

Build new transmission corridors

Upgrade substations

Install high-capacity transformers

Invest in redundancy

Companies supplying these components often enjoy:

High barriers to entry

Long customer relationships

Recurring upgrade cycles

Grid ETFs aggregate exposure to these firms without requiring investors to pick individual winners.

6. Risk Profile: Why Grid ETFs Are More Defensive Than AI Tech

Compared to AI software stocks, grid ETFs have a very different risk profile.

Advantages

Less valuation risk

Real asset exposure

Revenue tied to physical necessity

Long-term contracts and project pipelines

Risks

Interest rate sensitivity

Regulatory delays

Slower growth than pure tech

Capital intensity

This makes grid ETFs particularly attractive as:

Portfolio stabilizers

Inflation-resilient assets

Complements to growth tech holdings

They may not deliver explosive returns—but they offer durable, structural growth.

7. How to Use GRID and PAVE in a Portfolio

Conservative Allocation

GRID as a thematic satellite

Combined with utilities or dividend ETFs

Balanced Allocation

GRID for targeted grid exposure

PAVE for broader infrastructure diversification

Growth-Oriented Allocation

Grid ETFs alongside AI, semiconductors, and energy

Focus on long-term structural demand rather than short-term cycles

For most investors, grid ETFs work best as complements, not standalone holdings.

8. Why the Grid Theme Extends Beyond 2026

The most important point is this:

Grid investment is not a one-cycle story.

Once AI infrastructure is built:

Power demand does not decline

Maintenance and upgrades continue

Redundancy requirements increase

In other words, the grid does not “finish” upgrading—it evolves continuously.

This gives grid-focused ETFs one of the longest runways of any AI-related investment theme.

Conclusion: Owning the Wires Behind AI

AI may be digital, but its backbone is physical.

No matter which AI models win, which software platforms dominate, or which chips outperform, electricity must flow—reliably, continuously, and at scale.

That reality makes electrical grid and transmission infrastructure one of the most critical—and investable—AI enablers.

ETFs like GRID and PAVE allow investors to own this backbone:

Without betting on individual projects

Without chasing AI hype

With exposure to long-term, unavoidable investment needs

For 2026 and beyond, grid ETFs are not just an energy play—they are a strategic AI infrastructure allocation.

With interest rates still elevated and market volatility remaining a reality in 2026, many Canadian investors are actively searching for reliable monthly income without having to sell their investments. As a result, monthly income ETFs—particularly those using covered call strategies—have gained significant traction among retirees and income-focused portfolios.

Among Canadian providers, Hamilton ETFs has emerged as a specialist in high-income, covered-call-based ETFs, offering sector-specific solutions designed to convert market volatility into consistent cash flow.

In this article, we review the best Hamilton ETFs for monthly income in 2026, explain how their covered call strategies work, and help you determine which ETF may align best with your income needs and risk tolerance. The goal is not to chase yield blindly, but to understand how these ETFs fit within a well-structured income strategy.

Why Income Investors Choose Hamilton Covered Call ETFs

1. HMAX ETF Review – Canadian Bank Covered Call Income

HMAX ETF focuses on Canada’s major banks and financial institutions (RBC, TD, BMO, Scotiabank, etc.) and uses an active covered call strategy to generate higher monthly income.

Here is the key point most investors misunderstand: HMAX typically sells call options on about 50% of the portfolio, not 100%.

What does that mean in simple terms?

On half of the holdings, the manager sells at-the-money call options (usually short-term, often monthly).

In exchange, the ETF collects option premiums, which are paid out as monthly income.

The other 50% of the portfolio remains uncovered, allowing some participation in upside when bank stocks rise.

This balanced approach helps:

boost income without fully eliminating growth potential,

reduce volatility compared to fully covered portfolios,

and smooth cash flow for income-focused investors.

Investors like HMAX because it transforms relatively stable Canadian banks into a predictable monthly income source, while still keeping partial exposure to long-term capital appreciation.

Why invest in financials in the first place?

Financials—especially Canadian banks and insurers—are often considered a core sector for income-oriented investors.

Here’s why many investors allocate to financials:

Essential role in the economy Banks sit at the center of economic activity: lending, mortgages, payments, credit cards, and wealth management. As long as the economy functions, financial institutions remain relevant.

Strong cash flows Large banks generate consistent earnings which supports reliable dividends.

Dividend history and discipline Canadian banks, in particular, have a long track record of paying dividends.

Inflation and rate sensitivity In certain environments, higher interest rates can improve bank margins, helping earnings and income generation.

Lower volatility than many sectors Compared to tech or commodities, financials tend to be more stable, making them suitable for income-focused portfolios.

Best for: Investors seeking reliable income from Canadian financials, especially retirees who value predictable cash flow.

Key risk: Limited upside during strong bank rallies due to covered calls.

2. QMAX ETF Review – Technology Covered Call ETF for Monthly Income

QMAX ETF targets large-cap U.S. technology stocks and uses an active covered call strategy to turn volatility into monthly income.

Here’s what many average investors misunderstand: QMAX typically writes call options on about 50 % of the portfolio rather than fully covering all holdings.

What this means in practice:

On roughly half of the tech shares, the ETF sells at-the-money call options with short expiries (often monthly),

It collects premium income from those sales,

While the other half remains uncovered, allowing the portfolio to benefit from potential upside if tech stocks rally.

This strategy helps balance income generation with growth potential. Investors like QMAX because:

It offers higher monthly distributions than owning the stocks outright,

It harnesses the volatility inherent in tech stocks to generate cash flow,

And it still retains participation in market upswings thanks to the uncovered portion of the portfolio.

Why invest in technology in the first place (for QMAX)?

Technology stocks, particularly large-cap U.S. tech companies, are a cornerstone of many long-term investment portfolios — and there are several reasons investors choose this sector before even considering income strategies like QMAX:

Long-term growth leadership Many tech firms are market leaders with innovative products and services, strong competitive moats, and global reach. Over the past decade, technology has consistently led market returns.

High profitability and reinvestment power Dominant role in the modern economy Tech companies power digital transformation across industries — cloud computing, artificial intelligence, digital payments, social media, and more — making them less cyclical and more resilient over time.

Innovation-driven earnings Diversification benefit Including technology exposure in a portfolio can help diversify risks associated with sectors like financials, utilities, and energy.

Best for: Income investors who still want exposure to technology, but with lower volatility than owning tech stocks outright.

Key risk: Strong tech bull markets may cap upside returns.

UMAX ETF focuses on utility companies and uses a covered call strategy with at-the-money (ATM) options to generate enhanced monthly income.

A key point many average investors miss: UMAX typically sells ATM call options on about 50% of the portfolio, not on all holdings.

In simple terms:

On roughly half of the utility stocks, the ETF sells ATM call options, meaning the strike price is close to the current market price.

ATM options generate higher option premiums than out-of-the-money calls, which boosts monthly income.

The remaining 50% of the portfolio stays uncovered, allowing some participation if utility stocks rise.

Why invest in utilities in the first place?

Utilities are often considered defensive investments because:

Demand for electricity, water, and gas is relatively stable, regardless of economic cycles.

Revenues are often regulated, which can lead to more predictable cash flows.

Utility stocks tend to be less volatile than the broader market.

Investors like UMAX because it combines the stability of utilities with enhanced income generation, making it appealing for conservative, income-focused portfolios.

Why invest in utilities in the first place (for UMAX)?

Utilities are a core defensive sector in many investment portfolios, and there are solid reasons investors allocate to them before even considering income strategies like UMAX:

Stable demand and essential services Utility companies provide electricity, water, gas, and related infrastructure—services people and businesses need regardless of economic conditions.

Predictable cash flows Because their services are essential and often regulated, utilities tend to generate steady, predictable income, which supports reliable dividends.

Lower volatility

Defensive characteristics during downturns

Dividend focus Many utility companies have a history of paying dividends, appealing to investors seeking income and stability.

Best for: Conservative investors prioritizing capital stability and income consistency.

Key risk: Interest-rate sensitivity typical of utility stocks.

SMAX ETF is designed for investors seeking attractive monthly income while maintaining diversified exposure to large-cap U.S. equities across multiple sectors. With a current yield of 10.79% and monthly distributions, SMAX aims to convert equity market volatility into consistent cash flow.

The ETF holds a broad mix of U.S. stocks that closely resembles the sector composition of the S&P 500, including technology, financials, healthcare, consumer sectors, and energy. Instead of concentrating on a single theme, SMAX provides diversification across the U.S. economy, reducing reliance on any one stock or sector.

To generate income and reduce volatility, SMAX employs an active covered call strategy. Importantly, the coverage ratio is flexible, meaning calls are written on only part of the portfolio and adjusted over time to balance income generation with upside participation.

Best for: Investors seeking diversified U.S. exposure with monthly income.

Key risk: Income may fluctuate depending on market volatility.

5. AMAX ETF Review – Gold Miners Covered Call ETF for Income

AMAX ETF stands out because it combines gold producer exposure with an active covered call strategy to generate monthly income—a rare combination in the Canadian ETF landscape.

Unlike physical gold or traditional gold ETFs, AMAX invests in gold-mining companies, whose revenues and cash flows are leveraged to the price of gold. This creates higher volatility, but also higher option premiums, which the fund monetizes by selling covered call options. Those option premiums are the primary driver of AMAX’s income distributions.

Key characteristics include:

Exposure to gold miners, not bullion

A potential hedge against inflation and currency weakness, as gold often performs well when real interest rates fall

Higher volatility than traditional income ETFs, due to both commodity price swings and equity market sensitivity

AMAX is best viewed as a diversification and inflation-protection tool, rather than a core income holding. It can complement traditional income ETFs by adding a non-correlated income source, but investors should be comfortable with larger price swings in exchange for income and diversification benefits.

Best for: Investors seeking diversification and inflation protection, with income.

Key risk: Commodity price fluctuations can impact NAV.

Important Risks of High-Yield Covered Call ETFs

While Hamilton ETFs are attractive tools for generating monthly income, it is essential for investors to clearly understand the trade-offs involved before allocating capital. These ETFs are designed primarily for cash flow, not for maximizing long-term capital appreciation.

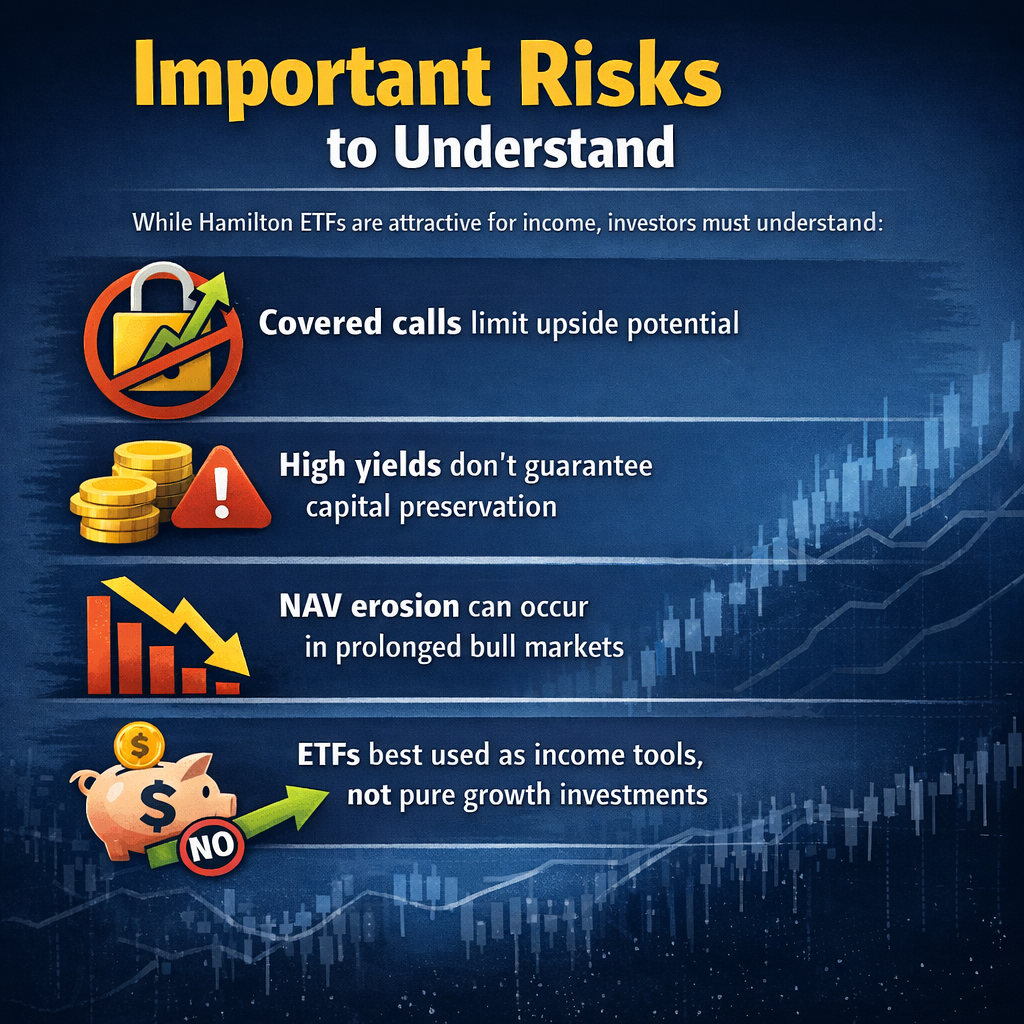

First, covered calls limit upside potential. By selling call options on a portion of the portfolio, the ETF collects option premiums that fund distributions. However, when markets rise sharply, gains on the covered portion are capped. This means investors may underperform the broader market during strong bull runs.

Second, high yields do not guarantee capital preservation. A double-digit yield can be appealing, but it does not imply safety. Distributions are generated from option premiums and dividends—not guaranteed returns—and market declines can still reduce the ETF’s net asset value (NAV).

Third, NAV erosion can occur in prolonged bull markets. When equities trend upward for extended periods, repeatedly selling calls can cause the ETF to lag the underlying stocks. Over time, this may result in slower NAV growth or even erosion compared to non-covered strategies.

Finally, these ETFs are best used as income tools, not pure growth investments. They are most effective when used intentionally—such as funding retirement income, enhancing portfolio cash flow, or replacing part of a bond allocation—rather than as long-term growth engines.

In short, Hamilton ETFs can play a valuable role in an income-focused portfolio, but success depends on understanding their mechanics and using them for the purpose they were designed for: reliable income, with controlled risk—not maximum growth.

Final Thoughts

Hamilton ETFs offer some of the most compelling monthly income solutions available to Canadian investors today. By combining sector-focused equity exposure with actively managed covered call strategies, these ETFs can play a meaningful role in:

retirement income planning,

cash-flow-focused portfolios,

and yield enhancement strategies.

However, they are not one-size-fits-all investments. The higher income comes with clear trade-offs, including capped upside and potential NAV erosion over time. Understanding how each ETF generates income, which sector it targets, and the risks involved is essential before allocating capital.

Used thoughtfully—often as part of a broader, diversified portfolio—Hamilton ETFs can help investors prioritize income without losing sight of long-term portfolio stability. The key is aligning the ETF selection with your objectives, time horizon, and tolerance for volatility, rather than focusing solely on headline yields.

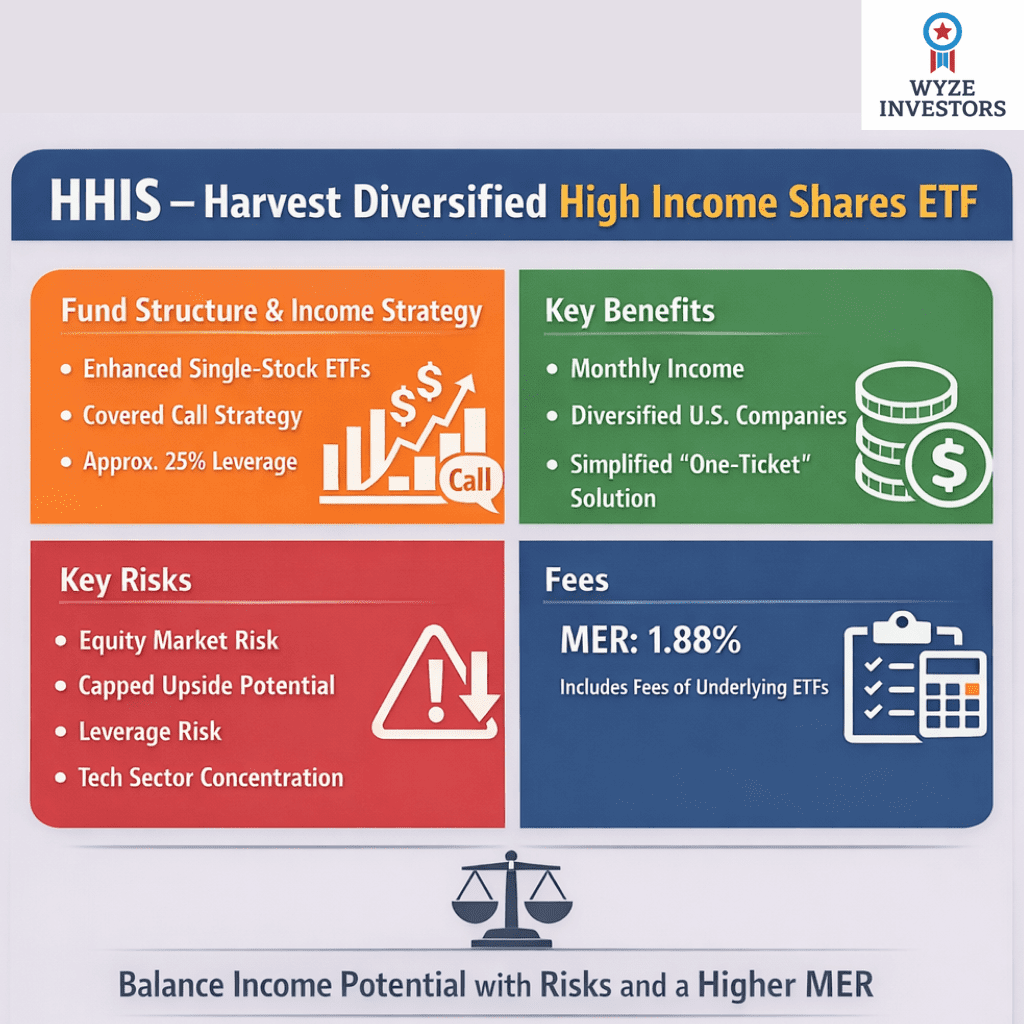

The Harvest Diversified High Income Shares ETF (TSX: HHIS) is designed to provide investors with diversified exposure to U.S. companies while generating a relatively high level of monthly income. It does this primarily through a portfolio of enhanced single-stock ETFs that use an active covered call strategy, and in certain cases, modest leverage. HHIS may appeal to investors looking for income from companies that are traditionally associated with growth rather than dividends.

This article provides an objective overview of how HHIS is structured, what it holds, how income is produced, potential advantages, risks, and how the ETF may fit within an investment portfolio.

Executive summary

ETF Objective and Investment Approach

HHIS seeks to combine three elements in one product:

exposure to large, well-known U.S. companies

monthly cash distributions

diversification through a basket of individual enhanced income ETFs

The ETF does not attempt to track a specific index. Instead, it is actively managed. Portfolio managers select and weight holdings and determine covered call activity levels. The primary income source is option premium generated by selling covered call options on the underlying positions.

HHIS is available in Canadian dollar and U.S. dollar trading classes, making it accessible to investors with income preferences in either currency.

Video

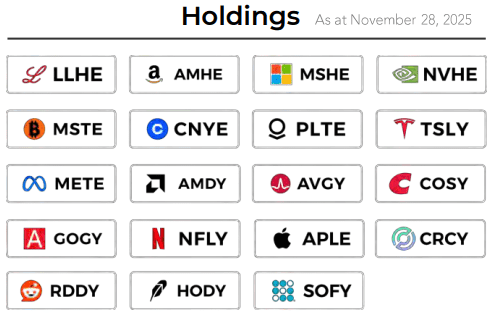

Portfolio Structure and Holdings

HHIS holds a portfolio of Harvest single-stock High Income Shares ETFs rather than owning individual securities directly. Each of those underlying ETFs typically:

focuses on one publicly listed U.S. company

writes covered calls on a portion of its position

may employ modest leverage (approximately 25% in enhanced series)

distributes income monthly

Therefore, HHIS functions as a fund-of-funds.

Holdings are diversified across several well-known U.S. companies in areas such as technology, e-commerce, semiconductors, pharmaceuticals, and fintech. Examples include ETFs tied to:

Allocations may change over time as the manager adjusts exposures. Investors should consult the most recent fact sheet or management report for precise weighting and current holdings.

Covered Call Strategy

The defining feature of HHIS is its covered call writing strategy implemented at the underlying ETF level. A covered call involves:

holding a stock or ETF

selling call options on that asset

collecting option premiums in exchange for giving up some potential upside

Option premiums collected contribute materially to monthly distributions. However, covered call writing also reduces participation in strong upside price movements because gains above the option strike price are limited or foregone when calls are exercised.

Harvest typically limits overwrite levels to a maximum of 50% of the portfolio, allowing some portion of assets to remain uncovered, which preserves participation in potential growth.

The strategy is actively managed, meaning:

coverage levels may be adjusted based on volatility

strike selection varies

expiration timing can change based on market conditions

When volatility increases, option income potential typically rises but so does equity risk. When volatility is low, premium income declines but market conditions may be calmer.

Use of Leverage

Some of the single-stock enhanced ETFs within HHIS use approximately 25% leverage. The stated goal is to:

increase exposure to core holdings

potentially increase option premium income

enhance total return over time

However, leverage also magnifies losses during market downturns and increases portfolio volatility. Borrowing costs associated with leverage can rise when interest rates increase, which can impact fund performance and net income.

Investors considering HHIS should be aware that leverage is a meaningful risk factor and contributes to both higher income potential and increased drawdown risk.

Return of Capital (ROC): What HHIS investors should know

Investors in HHIS will notice that distributions may sometimes include Return of Capital (ROC). This is common among covered-call income ETFs and fund-of-fund structures. Understanding ROC is important because it affects taxation, adjusted cost base, and long-term returns.

What ROC is (and isn’t)

ROC is a distribution that is not immediately taxed as income when received in a taxable account. Instead, it is treated as a return of your own invested capital. Because it is not taxed when paid, ROC reduces your Adjusted Cost Base (ACB). When you eventually sell units, a lower ACB may result in a larger capital gain.

ROC does not automatically mean the fund is “giving your money back.” In covered-call ETFs, ROC can result from:

option premium income

portfolio rebalancing

distribution-smoothing policy

fund-of-fund tax mechanics

However, if ROC remains persistently high and NAV declines over time, investors should evaluate whether distributions are being supported by option income or primarily by capital erosion

Key Advantages

Objectively, potential advantages of HHIS include:

Diversified exposure to leading companies

Investors gain access to multiple large-cap and innovative U.S. businesses in one ETF, which may reduce single-stock risk compared with owning only one growth company.

Monthly income distribution

The covered call strategy produces option premiums that support regular monthly cash flow, which can be attractive for those drawing income or reinvesting distributions.

Simplicity

HHIS combines:

security selection

option writing

rebalancing

distribution management

into one product, reducing the need for active involvement from the investor.

Lower capital threshold

Some underlying U.S. companies trade at high share prices. HHIS allows fractional exposure through an ETF trading on the TSX at a typically lower per-unit price.

Key Risks, Limitations and Fees

HHIS also carries meaningful risks. Key considerations include:

Equity market risk

The ETF primarily invests in equities. Market downturns can significantly reduce net asset value.

Capped upside potential

Covered call strategies limit capital appreciation during strong bull markets because option income is earned in exchange for foregoing some gains.

Leverage risk

Leverage magnifies returns in both directions. Losses are accelerated during market drawdowns and borrowing costs can affect returns when interest rates are high.

Sector concentration risk

Although diversified by issuer, many holdings are concentrated in technology-oriented industries. Sector-specific downturns can materially affect fund performance.

Distribution risk

Monthly distributions are not guaranteed and can fluctuate or be reduced depending on market conditions and option income availability.

Fees

Fees deserve special attention. HHIS has a Management Expense Ratio (MER) of 1.88%. This figure already includes its proportionate share of the fees of the underlying ETFs in which it invests. The MER is typical for actively managed, leveraged, covered-call fund-of-funds structures in Canada, but it is higher than broad index ETFs and some U.S.-listed covered call ETFs, which can be cheaper. Investors should weigh the higher cost against what they receive in exchange: professional options management, leverage handling, and a bundled one-ticket portfolio of single-stock covered call strategies.

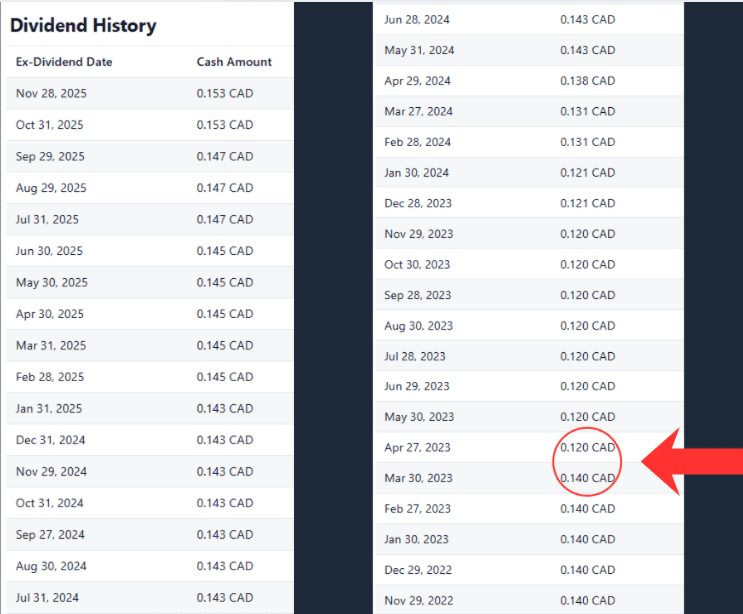

Performance / Distributions

The Performance / Distributions table provides information about HHIS’s cash-flow history rather than its total return, because performance figures cannot be shown until the ETF has completed one full year from its inception date of January 16, 2025. Until that milestone is reached, the table focuses on distributions. It lists the record date, ex-dividend date, payment date, monthly amount per unit, and the cumulative total since inception. The amounts shown indicate that HHIS has made consistent monthly distributions, with payments of $0.25 per unit initially and a gradual increase to $0.27 per unit later in the year. This table helps investors understand the income stream generated so far, the timing of distributions, and how much has been paid in total since launch, even though full performance metrics such as total return and risk statistics will only be available after the first year of operation.

are comfortable with equity risk and distribution variability

understand that upside potential may be partially capped

accept leverage as part of the strategy

It may appeal to:

income-focused investors

retirees or pre-retirees seeking cash flow

investors who hold traditional index ETFs but want income-tilted exposure

those seeking diversification among several well-known U.S. companies

Financial advisors and portfolio managers may also use HHIS in discretionary portfolios for income mandates.

About the ETF Provider

HHIS is managed by Harvest ETFs, an independent Canadian asset manager specializing largely in income-oriented exchange-traded funds. The firm emphasizes investment in established companies combined with disciplined options strategies. Harvest manages multiple High Income Shares ETFs and a variety of sector and thematic income funds.

Conclusion

HHIS offers a way to obtain diversified exposure to major U.S. companies while generating consistent monthly income through an active covered call approach. Its structure simplifies access to covered call strategies and enhanced single-stock ETFs in a single product. However, investors must balance the benefits of income and diversification against the trade-offs of capped upside, leverage, sector concentration, and equity market risk.

HHIS may be appropriate for investors seeking income-focused equity exposure who understand how covered calls and leverage affect risk and return. As with any investment decision, prospective investors should review the prospectus, management reports of fund performance, and risk disclosures, and consider how HHIS fits within their broader financial objectives and risk tolerance.

VOO is one of the most owned ETFs on the planet. Managed by Vanguard, it tracks the S&P 500 index — the 500 largest publicly traded companies in the United States. With an expense ratio of just 0.03%, it is among the cheapest investment products ever created. Warren Buffett has famously recommended it. Millions of American investors hold it as their core retirement position.

For Muslim investors in both the United States and Canada, VOO comes up constantly. It is simple, cheap, and widely recommended. But is it halal?

The answer is no — VOO is not halal in its standard form. But understanding why, and what to do instead, is what this article is about.

What Does VOO Actually Hold?

VOO tracks the S&P 500 index, which includes 500 of the largest U.S. companies weighted by market capitalization. As of 2026, the top holdings include Apple, Microsoft, Nvidia, Amazon, Alphabet (Google), Meta, Berkshire Hathaway, and JPMorgan Chase.

At first glance this looks promising — tech companies dominate the top of the list, and many of them pass Sharia screening individually. But the S&P 500 is a broad market index, which means it holds companies from every sector of the economy — including sectors that are categorically excluded under Islamic finance principles.

Why VOO Is Not Considered Halal

There are two main reasons VOO fails Sharia screening.

Problem 1 — Financial Sector Holdings

The S&P 500 includes a significant allocation to the financial sector — approximately 12-15% of the total index depending on market conditions. This includes:

JPMorgan Chase — the largest U.S. bank by assets, whose primary business is interest-based lending

Bank of America, Wells Fargo, Citigroup — all excluded for the same reason

Berkshire Hathaway — Warren Buffett’s conglomerate, which owns major financial businesses including insurance companies and a large stake in Bank of America

Goldman Sachs, Morgan Stanley — investment banking and financial services

Visa and Mastercard — these are sometimes considered borderline, but they facilitate interest-bearing transactions at scale

Conventional banking is categorically excluded under Islamic finance because the entire business model is built on charging interest — Riba. Owning an index that includes a 12-15% allocation to conventional banks means owning a fundamentally non-compliant portfolio, regardless of how strong the tech component is.

Problem 2 — Other Prohibited Sectors

Beyond financials, the S&P 500 also includes allocations to:

Alcohol companies — companies with significant alcohol revenue within consumer staples and other sectors

What About the Fact That Tech Makes Up 30%+ of VOO?

This is the most common argument we hear: ‘But VOO is mostly tech now — Apple, Microsoft, Nvidia, Amazon make up over 30% of it. Doesn’t that make it mostly okay?’

The answer is no, and here is why. Owning a fund that is 30% halal tech and 70% uninvestigated (with 15% in clearly haram financials) is not the same as owning a halal fund. The fund holds the haram companies just as definitively as it holds the halal ones.

Think of it this way: if you bought a basket of mixed fruit that included some rotten pieces, you would not eat the whole basket just because most pieces were fresh. You would either remove the rotten pieces — which is exactly what a halal ETF does — or buy a basket that only contained fresh fruit.

A halal ETF removes the prohibited companies and gives you only the compliant ones. VOO does not do this.

The Halal Alternative to VOO

The good news is that there is now a direct halal equivalent to VOO. In fact, there are several.

Ticker

Fund Name

vs VOO

MER

Notes

SPUS

SP Funds S&P 500 Sharia ETF

Closest equivalent

0.49%

Screens S&P 500 for Sharia — best substitute

HLAL

Wahed FTSE USA Shariah ETF

Very similar

0.50%

U.S. large & mid-cap, FTSE methodology

ISUS

iShares MSCI USA Islamic ETF

Similar scope

0.50%

BlackRock’s Islamic U.S. equity ETF

SPRE.TO

SP Funds S&P 500 Sharia (CAD)

For Canadians

~0.49%

Same as SPUS but trades in CAD on TSX

SPUS — The Most Direct VOO Substitute

SPUS is managed by SP Funds and applies AAOIFI Sharia screening to the S&P 500 universe. It removes the prohibited companies — primarily financial stocks, defense contractors, alcohol, and tobacco — and holds the remaining compliant companies.

The result is a portfolio that looks quite similar to VOO’s top holdings, but without the haram exposure. Apple, Microsoft, Nvidia, Amazon, Alphabet, and Meta remain prominent holdings (subject to their passing Sharia screening at each quarterly review). The financials are removed.

The cost is slightly higher than VOO — 0.49% versus VOO’s 0.03% — but this is a necessary price for the screening infrastructure. And compared to most actively managed funds, 0.49% is still very low.

SPUS has grown to over $2 billion in assets under management, making it the largest halal ETF listed on U.S. exchanges. It is available at Fidelity, Charles Schwab, Robinhood, and most other U.S. brokers.

What About VTI — Vanguard Total Stock Market ETF?

Some investors ask about VTI — Vanguard’s Total Stock Market ETF, which holds virtually every publicly traded U.S. company (around 3,700 stocks). If VOO is not halal, VTI is even further from compliance. It holds every financial company, every weapons manufacturer, every tobacco and alcohol company in the U.S. market with no filtering whatsoever.

VTI has the same fundamental problem as VOO, amplified. More companies means more prohibited holdings, not fewer. The answer is the same: not halal, replace with a Sharia-screened equivalent.

Canadian Investors — A Special Note on VOO

Canadian investors sometimes hold VOO directly through their RRSP or TFSA at Questrade or Wealthsimple. Beyond the Sharia compliance issue, there are also practical reasons why a Canadian-listed equivalent may be preferable.

SPRE.TO — the Canadian-listed version of the SPUS strategy — trades in CAD on the Toronto Stock Exchange. It eliminates the need for currency conversion, which can cost 1.5-2% at most bank brokerages if not using Norbert’s Gambit. It also functions cleanly inside a TFSA without the U.S. dividend withholding tax applying in the same way.

For Canadian Muslim investors who were holding or considering VOO: SPRE.TO in your TFSA, or SPUS in your RRSP (to benefit from the Canada-U.S. tax treaty waiving the withholding tax), are the recommended replacements.

What About Performance? Is SPUS Competitive With VOO?

This is a fair and important question. The honest answer is that SPUS has underperformed VOO in some periods and outperformed it in others. The difference in long-term compound returns has been small.

The reason performance tracks closely is that the financial sector — the main thing being removed — is not the primary driver of S&P 500 returns over most long-term periods. Technology has been the dominant driver, and halal indices are effectively overweight technology relative to conventional indices. In technology bull markets, halal ETFs often outperform. In periods when financials do well, they may lag slightly.

What matters for Muslim investors is not that SPUS perfectly matches VOO — it is that SPUS gives you competitive exposure to U.S. equities without compromising your principles. The expected long-term return difference is small. The principle difference is significant.

Final Verdict

Is VOO Halal? — The Bottom Line VOO is NOT halal. It holds a significant allocation to conventional banks, insurance companies, weapons manufacturers, and other prohibited sectors that cannot be corrected through purification. The direct halal substitute is SPUS (in USD) or SPRE.TO (in CAD for Canadian investors). Both apply AAOIFI Sharia screening to the S&P 500 universe and are available at major brokers. The performance difference relative to VOO has historically been small. The principled difference is significant — and it is entirely possible to build a competitive long-term portfolio without VOO.

To check the current Sharia compliance status of any ETF or individual stock, use our Free Halal ETF & Stock Screener at halaletfhub.com/screener — updated regularly for both Canadian and U.S. investors.

If you are looking to invest in the US stock market while staying aligned with Islamic finance principles, you have likely come across SPUS. It is one of the most popular halal ETFs available today, often seen as the go-to option for Sharia-compliant exposure to large US companies.

But is SPUS truly a strong long-term investment, or is it simply a filtered version of the S&P 500 with limitations investors often overlook? In this complete review, we will break down how SPUS works, what it holds, its performance, risks, and whether it deserves a place in your halal portfolio.

What is SPUS ETF?

SPUS, officially known as the SP Funds S&P 500 Sharia Industry Exclusions ETF, is a US-listed ETF designed to provide exposure to large-cap American companies while following Sharia-compliant investment principles.

In simple terms, SPUS tracks a modified version of the S&P 500 but removes companies that do not meet Islamic finance guidelines.

This includes:

Conventional banks and financial institutions

Companies with high levels of debt

Businesses involved in prohibited industries such as alcohol, gambling, or tobacco

The result is a portfolio that focuses heavily on growth-oriented companies, particularly in sectors like technology.

For halal investors, this offers a structured and accessible way to participate in the US equity market without compromising their values.

How SPUS Stays Sharia-Compliant

SPUS follows a multi-step screening process to ensure compliance with Islamic finance principles.

1. Industry Screening

The first step removes companies involved in non-compliant activities such as:

Interest-based financial services

Alcohol and tobacco

Gambling

Adult entertainment

This immediately eliminates a significant portion of the traditional market, especially the financial sector.

2. Financial Ratio Screening

The second step focuses on financial health. SPUS excludes companies that:

Have excessive debt levels

Generate significant income from interest

This is critical because Islamic investing avoids businesses that rely heavily on interest-based financing.

3. Purification Process

Even after screening, some companies may still earn a small portion of non-compliant income.

To address this, SPUS applies a purification process where a small percentage of income is identified. Investors are expected to donate this portion to maintain full compliance.

What Does SPUS Hold?

One of the most important aspects of any ETF is its underlying holdings.

Because SPUS excludes financials and other sectors, its portfolio looks quite different from the traditional S&P 500.

Top Holdings

SPUS is heavily concentrated in large technology and growth companies, including:

Apple

Microsoft

Nvidia

Amazon

Meta

Alphabet

These companies tend to have strong balance sheets and lower reliance on debt compared to traditional financial institutions.

Sector Allocation

The ETF has:

High exposure to technology

Reduced exposure to financials

Limited diversification across certain sectors

This creates a unique profile compared to traditional index ETFs.

Performance Overview

SPUS has delivered strong performance over recent years and has even outperformed the S&P 500 during certain periods.

The main reason is sector exposure. Because SPUS is heavily weighted toward technology and growth stocks, it has benefited from the strong performance of these sectors. Companies like Nvidia and Microsoft have been major drivers of returns, boosting overall performance.

Important Reality

However, this outperformance is not guaranteed.

If technology stocks underperform

If financial sectors outperform

SPUS may lag behind the broader market.

Fees and Expense Ratio

SPUS has an expense ratio of approximately 0.49 percent.

This is significantly higher than traditional S&P 500 ETFs, which often have fees below 0.10 percent.

Why Higher Fees?

The additional cost comes from:

Sharia screening processes

Ongoing compliance monitoring

Portfolio adjustments

Should You Be Concerned?

While fees do impact long-term returns, many investors accept higher costs in exchange for investing in a way that aligns with their values.

The key is understanding what you are paying for.

Key Advantages of SPUS

1. Halal Compliance

SPUS provides a straightforward way to invest in the stock market while respecting Islamic principles.

2. Access to US Market Growth

You gain exposure to some of the largest and most innovative companies in the world.

3. Simplicity

Instead of selecting individual halal stocks, SPUS offers a ready-made solution.

4. Strong Growth Potential

The ETF is positioned toward sectors that have historically delivered strong long-term returns.

SPUS vs S&P 500

Understanding the difference between SPUS and the traditional S&P 500 is essential.

S&P 500

Fully diversified

Includes all sectors

Strong exposure to financials

SPUS

Sharia-compliant filtering

Excludes financial sector

More concentrated portfolio

Key Trade-Off

The real difference is not performance versus underperformance.

It is: 👉 Growth exposure versus diversification

Risks to Consider

Like any investment, SPUS comes with risks.

1. Market Risk

SPUS is still an equity ETF. Its value can fluctuate with market conditions.

2. Sector Concentration

Heavy exposure to technology means:

Higher upside potential

Higher downside risk

3. Reduced Diversification

Excluding financials limits diversification compared to traditional ETFs.

4. Sharia Constraints

Because the investable universe is smaller, SPUS may miss opportunities available in the broader market.

Who Should Invest in SPUS?

SPUS is best suited for:

✔ Halal investors

Those who want to invest while following Islamic principles.

✔ Long-term investors

Investors focused on growth over time.

✔ Passive investors

Those who prefer a simple ETF instead of selecting individual stocks.

Who Should Avoid SPUS?

SPUS may not be ideal for:

Investors seeking maximum diversification

Investors focused on low fees

Those uncomfortable with sector concentration

Final Verdict: Is SPUS Worth It?

SPUS is one of the most accessible and well-structured halal ETFs available today.

It offers a powerful combination of:

Market exposure

Simplicity

Sharia compliance

However, it is not a perfect replacement for the S&P 500.

The Reality

SPUS is not about outperforming every index.

It is about:

👉 Investing with conviction 👉 Aligning your portfolio with your values

Video

🧠 Final Insight

For many investors, the best approach is not choosing between SPUS and other ETFs.

It is building a balanced halal portfolio that includes:

This content is for educational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

Canadian investors are increasingly interested in dividend stocks. And it makes sense: they offer a powerful double advantage:

Regular income in the form of dividends

Long-term capital growth potential

But not all dividends are created equal. Some companies have a high dividend… only because their stock price has fallen sharply. This is called a “dividend trap” : attractive yield, but dividend at risk of cut-off. That’s why, for 2026, the strategy we’re putting forward is simple:

👉 Prioritizing “quality” over “high yield”

This article focuses on:

financially strong companies

Sustainable and growing dividends

Robust balance sheets

High cash flow generation

In short: companies that are not only able to pay today… but also to continue to increase their dividends tomorrow.

Video

Why focus on “quality” in 2026?

The current economic environment is characterized by:

Interest rates still high

moderate economic growth

Geopolitical risks

Markets that are sometimes very volatile

In this context, high-quality companies offer three major advantages.

1. Protection contre les “yield traps”

Some companies advertise returns of 8%, 9%, 10% or more. This sounds very attractive to an investor looking for income, but such a level of return often hides a less positive reality. In many cases, this high yield is mainly due to a sharp drop in the share price. Since the return is calculated according to the price, when the stock falls, the percentage rises mechanically. It is therefore not necessarily a “good deal”, but sometimes a warning signal.

These companies often combine fragile profits with high debt. When profits fall or interest rates rise, it becomes difficult to maintain a high dividend. The consequence is known:

❌ Fall in the share price❌, reduction or cut of the dividend, lasting❌ loss for the investor

In their case, the dividend is sustainable and becomes a real tool for long-term wealth creation, rather than a hidden risk. The conclusion is clear: a reasonable and reliable dividend is better than an exceptionally high yield built on shaky foundations.

2. Stability of payments

Investors are increasingly looking for:

Predictability

Regular income

Low dividend volatility

Quality companies tend to:

✔ Weathering recessions ✔ Adjusting capital intelligently ✔ Maintaining dividends even in difficult times

3. Capital Growth Potential

Dividends represent only a portion of the total return on a stock market investment. The other essential component is the appreciation of the stock price over time. A quality investment is therefore not limited to receiving regular payments: it must also allow the value of the security to increase sustainably.

Strong companies often share several characteristics: they innovate, develop new products, improve efficiency, and defend strong competitive positions. They generate significant and recurring cash flows, which allows them to finance their growth, reduce their debt and remunerate shareholders. They intelligently reinvest their profits: modernization, expansion, targeted acquisitions, or share buybacks.

These companies thus offer a double efficiency engine :

For the patient investor, this combination is powerful. The dividend provides regular income, while the increase in the share price helps build wealth. This is why focusing only on the dividend rate can be misleading: it is better to favor companies that can grow their earnings, dividends and stock market value over time.

How we selected the titles: the “high quality” factor

Our criteria are based on the “Quality” factor studied by Fidelity and other institutional managers. It is based on four concrete financial pillars.

✔ 1. Strong balance sheets

We give priority to companies:

Well capitalized

with cash

Shock-absorbing

A strong balance sheet means:

👉 Ability to maintain the dividend even during a crisis

We favour companies with strong balance sheets, well capitalised and sufficient liquidity to weather difficult times. Such a financial profile offers significant room for manoeuvre in the event of a recession, a rise in interest rates or a sector shock. These companies can continue to invest, repay their debts and maintain their dividends without having to resort to emergency financing. In concrete terms, a strong balance sheet means the ability to absorb crises without massive shareholder dilution or abrupt cuts in payouts. For a dividend investor, this is a central criterion: it increases income security and sustainability.

✔ 2. Predictable cash flows

The selected companies show:

Recurring cash flows

from core or dominant activities

Examples:

Infrastructure energy

Big banks

Mining royalties

The successful companies generate stable and recurring cash flows, often from core or dominant activities in the economy. This type of cash flow makes it possible to simultaneously finance dividends, investments and debt reduction. It is frequently found in sectors such as energy infrastructure, large banks, telecommunications or mining royalties. The predictability of receipts greatly reduces the risk of dividend cuts. It also allows managers to gradually increase payments over time. For the long-term investor, this visibility is a major asset, as it promotes steady, growing and sustainable returns.

✔ 3. High profitability

We looked for companies that could:

Generate high margins

Turning revenue → profit

Financing Growth + Dividends

We look for companies that can effectively convert their revenues into net profits. High profitability translates into strong margins, disciplined cost management and the ability to maintain their prices even in challenging economic environments. These companies can finance their organic growth, make strategic acquisitions and continue to remunerate their shareholders through higher dividends. Sustainable profitability is also a sign of competitive advantage: a strong brand, a dominant network, unique assets or differentiated technology. For the investor, this means a greater likelihood of long-term value creation, beyond just the current return.

✔ 4. Debt under control

Low debt allows:

Greater strategic flexibility

resistance to rising rates

Controlled debt allows companies to remain flexible when economic conditions deteriorate or interest rates rise. Interest costs that are too high can eat into profits and threaten the dividend. Conversely, reasonable debt allows you to invest, acquire and weather economic cycles without undue pressure. Firms with low debt are less vulnerable to banks, markets, and costly refinancing. They can continue to pay their dividends even when the environment becomes more difficult. For an income-oriented portfolio, financial discipline is therefore a key factor in stability and resilience.

The 7 Best Canadian Dividend Stocks for 2026

1. Enbridge (ENB) — The Energy Infrastructure Pillar

Enbridge is one of Canada’s most popular companies among dividend investors. It operates an extensive network of:

pipelines

Gas infrastructure

Energy utilities

Why does it stand out?

✔ Dividend announced to increase towards 2026 ✔ More than 30 consecutive years of relatively ✔ predictable increase in cash flow distributed

The dividend is based on distributable cash flow (DCF), estimated between:

👉 $5.70 and $6.10 per share for 2026 (guidance)

Investment thesis

regulated activity

Structural energy demand

Long-term infrastructure projects

Enbridge operates in a largely regulated business, making its revenue streams more predictable than those of many energy companies. It benefits from a structural energy demand, linked to the transport of oil and gas necessary for the functioning of the North American economy. Its long-term infrastructure projects provide high visibility into future cash flows through often multi-year contracts. For these reasons, Enbridge is particularly appealing to investors who are looking for stability, resilience and a gradual increase in dividend over time, rather than rapid but uncertain growth.

2. Royal Bank of Canada (RY) — The Canadian Banking Reference

RBC is the country’s largest bank by market capitalization.

It benefits from:

of a dominant national network

an international presence

an image of solidity

Why is RY a “quality” stock?

✔ Uninterrupted dividends for more than 150 years ✔ High profitability ✔ Income diversification (retail banking, insurance, capital markets)

Its yield is not the highest in the industry, but:

👉 It is among the most reliable

Investment thesis

• Strong brand franchise

• Essential positioning

• Balance sheet strength

Royal Bank of Canada has an extremely strong brand franchise, built on more than a century of history and a dominant presence in the country. Its key positioning in personal, commercial and wealth management banking provides it with diversified and resilient revenue streams. The bank also stands out for the strength of its balance sheet, with high capital ratios and prudent risk management. RY is particularly suitable for long-term investors who are looking for security, consistency and regularity of the dividend, rather than speculative bets on more volatile securities.

3. Toronto-Dominion Bank (TD) — North American Growth

TD combine :

Strong Canadian platform

huge presence in the United States

It is one of the banks most exposed to the US market.

Key Points

✔ Yield around 4% ✔ Valuation has become attractive again after recent ✔ challenges Business model focused on retail banking

Investment thesis

future growth related to the United States

Recurring retail profits

Ability to Navigate Economic Cycles

The Toronto-Dominion Bank has significant growth leverage with its strong presence in the U.S., where it continues to expand its retail business. Its recurring profits from retail banking provide a stable revenue base that is less dependent on short-term capital markets. TD has repeatedly demonstrated its ability to navigate economic cycles, maintaining prudent risk management and disciplined capital policy. This stock is particularly suitable for investors looking for both a regular dividend and the potential for a medium-term recovery when economic conditions improve.

Build a reliable monthly income from your portfolio

I’ve created ready-to-use ETF portfolios and a passive income calculator designed specifically for Canadian investors.

4. Canadian Natural Resources (CNQ) — La machine à cash-flow

CNQ is one of the most profitable energy companies in the country.

Why does CNQ attract?

✔ Yield around 5% ✔ 23 consecutive years of dividend ✔ increase Low operating costs

CNQ is recognized for its financial discipline:

Deleveraging

Share buybacks

distributions progressives

Investment thesis

High correlation to the price of oil

Low-cost production

Shareholder-oriented management

Canadian Natural Resources (CNQ) remains highly correlated with the price of oil, which can lead to sharp swings in the stock in the short term. However, the company stands out for its very low-cost production, which allows it to remain profitable even when energy prices fall. Its management adopts a clear management approach to shareholders, combining debt reduction, share buybacks and regular dividend increases. This makes CNQ a flagship stock for investors who accept volatility in exchange for growing dividends and long-term value creation potential.

5. Power Corporation of Canada (POW) — The Heritage Conglomerate

Power Corp owns:

Great-West Lifeco

IGM Financial

Wealthsimple (partial)

Why is POW interesting?

✔ Returns often higher than banks ✔ Global exposure to asset ✔ management Diversified holding structure

Investment thesis

Profits linked to the global financial markets

Growth through acquisitions and subsidiaries

Profits redistributed via dividends

Power Corporation (POW) derives a large portion of its profits from global capital markets through its significant holdings in wealth management and insurance. Its model is based on growth through acquisitions and the development of its subsidiaries, which allows it to diversify its revenue sources and smooth out economic cycles. A significant portion of profits is returned to shareholders in the form of dividends, supported by strong cash flows. POW is therefore particularly attractive to investors who are looking for high returns, geographic and sector diversification, and a long-term stability approach.

6. Bank of Nova Scotia (BNS) — Highest Yield of the Big Banks

Historically, BNS has offered the most generous bank dividend among Canada’s major banks.

Why does SNB attract despite the challenges?

✔ high ✔ performance international presence (especially Latin America) ✔ strategic recovery plan underway

Points of vigilance

Exposure to emerging markets

Restructuring still in place

The Bank of Nova Scotia (NBS) is unique in its strong exposure to emerging markets, particularly in Latin America, which provides it with superior long-term growth opportunities, but with more volatility. The bank is also engaged in a strategic restructuring that is still being rolled out, aimed at improving its profitability, strengthening its risk management and refocusing its activities on its most profitable markets. On the other hand, this adjustment phase can create short-term stock market fluctuations. SNB is therefore mainly aimed at investors who accept a little more risk in exchange for a generally above-average dividend yield.

7. Labrador Iron Ore Royalty (LIF) — Les redevances minières

Unlike traditional mining producers, LIF generates revenue through a royalty model.

It benefits from iron ore sales without directly assuming the costs of operating a mine.

What makes LIF unique?

✔ High ✔ margins, commodity-price-sensitive dividend, ✔ low operating debt

Investment thesis

correlated with iron ore price

Few heavy assets to manage

Good redistributive capacity

Labrador Iron Ore Royalty (LIF) is highly correlated with the price of iron ore, which means that its revenue and distributions can fluctuate with commodity cycles. Its business model is unique: the company holds royalties and therefore few heavy assets to manage, which limits operating costs and operational risks. Thanks to this lean structure, LIF often has a good redistribution capacity in the form of variable dividends. This stock may be attractive to investors looking to add sector diversification related to natural resources, while benefiting from attractive income potential.

Comparison

Stock

Yield

Strength

Risk Level

ENB

~7%

Stable cash flow

Medium

RY

~4%

Strong balance sheet

Low

TD

~4%

US growth

Medium

CNQ

~5%

Cash machine

Cycle risk

POW

~5%

Diversified

Medium

BNS

~6%

High yield

Higher risk

LIF

Variable

Royalty model

High

Conclusion — Dividends yes… but with quality

For 2026, the most reasonable strategy is to focus on strength rather than the search for maximum return at all costs. The aim is to select companies that can maintain and increase their dividends over time, even in times of economic volatility. This means focusing on companies with strong balance sheets, stable cash flows and controlled debt. Conversely, it is prudent to avoid “high-yield traps” – securities that offer very attractive rates but are based on fragile or over-leveraged models.

The seven companies selected—Enbridge, RBC, TD, Canadian Natural Resources, Power Corporation, The Bank of Nova Scotia and Labrador Iron Ore Royalty—embody this central idea: financial quality remains a long-term investor’s best ally. They combine a strong competitive position, the ability to generate cash flow and discipline in the distribution of dividends. This approach does not promise quick wealth, but it does prioritize income sustainability and incremental capital growth. In 2026 and beyond, building wealth is above all about patience, diversification and the rigorous selection of solid companies.

Educational clause

This article is intended to be informative and educational. It does not constitute a recommendation to buy or sell. Each investor should evaluate:

their risk tolerance

its investment horizon

their personal situation

and consult a professional if necessary.

The Hamilton Enhanced U.S. Covered Call ETF (HYLD) is attracting a lot of investors in Canada, particularly for its high monthly return. But behind the impressive casts is a question that many are asking:

👉 Does HYLD really pay dividends… or is it mainly a return of capital (ROC)?

In this comprehensive analysis, based on your Q&A, we clarify how distributions actually work, the difference between price and total return, and why ROC is not a danger sign — contrary to what many believe.

🟨 1. HYLD: A high-income ETF

HYLD is designed to offer a monthly cash flow through a combination of:

🎯 Target: ~12% return per yearHYLD explicitly targets high income, not unit price growth.

🟦 2. Price performance: an incomplete indicator

Many investors judge HYLD based solely on price. For example, over 5 years, the graph shows a relatively stable or even slightly declining performance.

But here’s the problem:

👉 The price does NOT reflect the actual performance of an income-oriented ETF.

This is because HYLD redistributes a large portion of the earnings in the form of monthly distributions, resulting that:

The net asset value rises less

But the total cash flow generated is very high

Looking only at the price is therefore ignoring 80–90% of the real return.

🟧 3. Total Return = Price + Dividends

To understand HYLD, you have to think in terms of total return.

📌 Formula:

Price Performance + Dividends = Total Return

The table shown in the video shows higher total return returns:

1 year: +25.9%

3-year annualized: +23%

Since 2022: +11.5%/year

YTD: +21.9%

➡️ Very solid figures, despite a price that is not exploding.

🟩 4. Distribution history: what the numbers tell us

By analyzing the distribution history, we notice:

Stable monthly payments

sometimes a drop in distribution during difficult market periods

the introduction of ROC as a major component in some years

A clear example: 📉 In 2022, the bear market forced HYLD to reduce its distributions (visible in April).

This shows that distributions are not guaranteed. They depend on option premiums and the health of the US market.

🟥 Article 5. Return of Capital (ROC): danger or simple tax classification?

Among the elements that most resonate with investors: 👉 Why does HYLD distribute so much ROC?

Here is the essential clarification:

ROC does NOT mean that the fund gives you back your own money.

This is NOT a sign that the fund is in trouble.

This is often the consequence of hedged options strategies.

When the gains generated by the options offset the decline in the underlying assets, there may be no taxable net gain. As a result, the distribution is classified as an ROC.

🟩 Significant tax effect:

ROC reduces the adjusted cost base (ACB), which can defer tax later.

So that’s not a bad thing — it’s an accounting reality linked to the fund’s strategy.

🟫 6. Simple example: GOOGL to understand the ROC

In the video, a clear example with GOOGL illustrates the phenomenon:

The manager sells covered options.

It generates bonuses every month.

But if the stock falls during the year… → the options offset the loss→ there is no taxable gain

Distributions cannot be reported as dividends or capital gains

They therefore become Return of Capital

🎯 ROC = a tax adjustment, not a hidden risk.

🟦 7. Why HYLD Needs to Be Evaluated Differently

HYLD is not a growth ETF. It should not be evaluated as VFV or VOO.

Here’s what really matters:

stable distributions

Ability to generate bonuses

Total Yield

Adequacy with the income profile

The main conclusion:

👉 HYLD actually generates income through options. The ROC simply reflects how these revenues are classified.

HYLD is not a growth ETF and therefore should not be evaluated as VFV or VOO. Its main objective is to provide a high income, which involves using different criteria to measure its performance. What really matters is the stability of distributions, the fund’s ability to generate premiums, total return and its suitability for an income-oriented profile. In practice, HYLD does generate income through its hedged options strategies. The ROC is only a tax classification of these distributions, and not a sign of fragility.

🟨 8. Key points to remember

HYLD is designed for high income, not growth.

The ROC is not a sign of danger, but a fiscal reality.

Distributions vary by market.

The total return is much higher than the price suggests.

HYLD is suitable for income-oriented investors, not extreme growth hunters.

Hedged options limit upside potential, but stabilize revenues.

HYLD is primarily an ETF designed to generate high income, not to offer strong capital growth. This orientation explains why its price may seem stable or not very dynamic, while its total return, including monthly distributions, is actually much higher than what an investor who only sees the price chart. A point that is often misunderstood concerns the Return of Capital (ROC): far from being a sign of weakness, it reflects above all a tax reality resulting from the hedged option strategies used by the fund. Distributions can also vary over the course of the market, as they depend on the premiums generated and broader economic conditions. HYLD is therefore primarily suitable for investors focused on income and cash flow stability, rather than those looking for aggressive growth comparable to a traditional index ETF. Finally, it should be understood that the hedged options used in the fund’s strategy naturally limit the potential for appreciation in times of strong bullish rally, but they also help to stabilise income, making HYLD an attractive tool for a sustainable income strategy.

🟩 Conclusion

In conclusion, HYLD is a powerful ETF for investors looking for:

high monthly income

A simple solution to generate cash flow

A diversified and option-optimised strategy

An attractive total return despite a stable price

Return on Capital is an integral part of the operation of this type of fund and should be understood as a tax concept, not as an alarm.

➡️ HYLD can be a great component of an income portfolio, as long as you understand how it generates its distributions and what trade-offs this strategy entails.

Executive summary

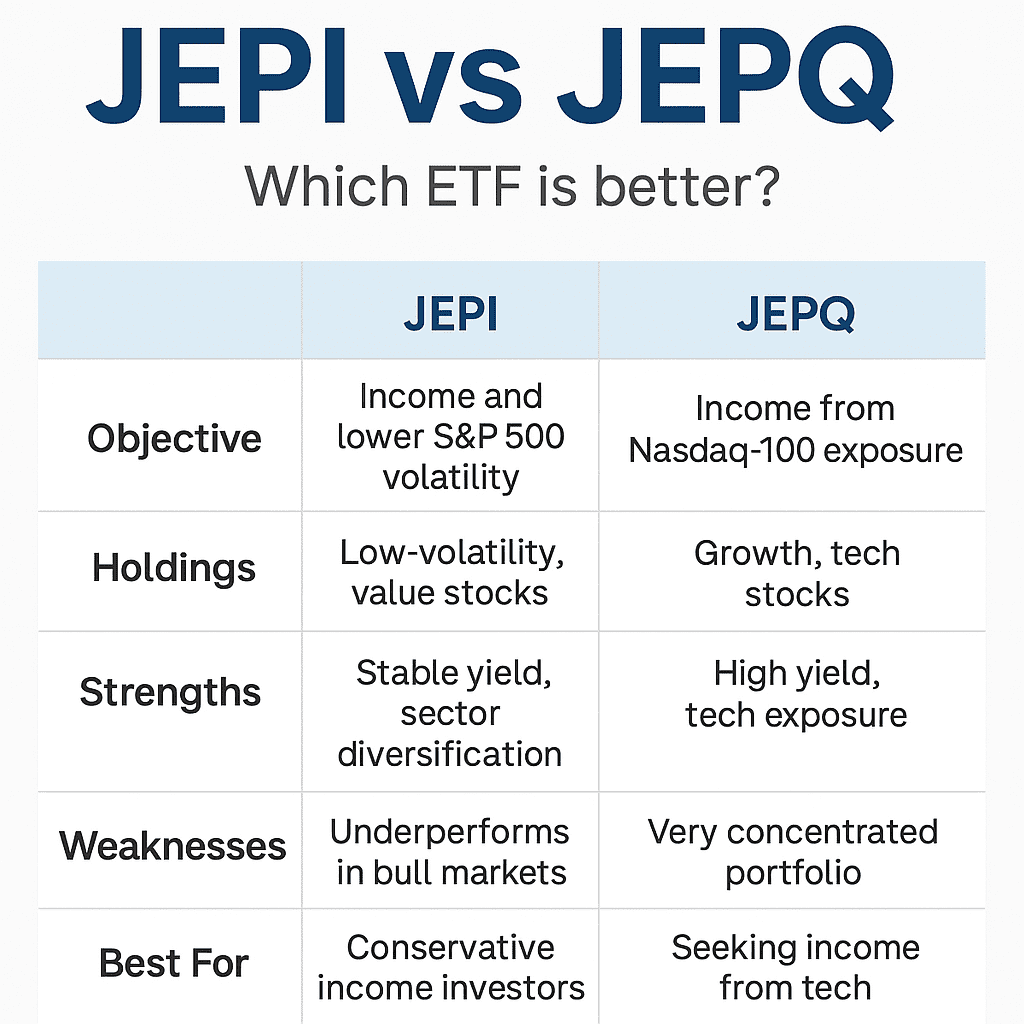

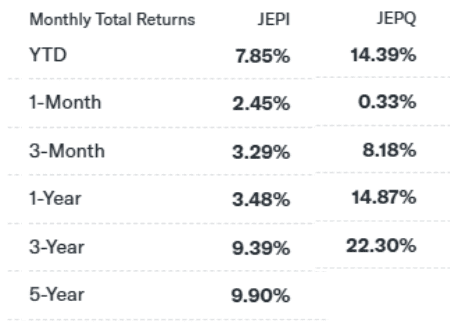

JEPI and JEPQ are two leading income-focused ETFs using covered call strategies, but they serve different investors. JEPI offers stable income with broad diversification and lower volatility, while JEPQ provides higher yield driven by tech exposure. Understanding their objectives, risks, and market behavior helps identify which ETF fits your strategy best.

JEPI

Investment objective

The JPMorgan Equity Premium Income ETF (JEPI) is an income focused covered call ETF. It’s ideal for conservative investors who are seeking income and moderate growth. The manager of JEPI invests in a portfolio of stocks that combine 3 characteristics:

Part of the S&P 500, so in other word large cap stocks only;

Low volatility stocks, meaning, stocks that fluctuate far less than the market. This is generally the case of defensive stocks operating in stable industries. The main metric used by the fund manager of JEPI to assess volatility is the Beta. Beta is a coefficient risk, for instance a Beta of 0.5 would indicate that the stock exhibits 50% of the volatility of the stock market;

Value stocks: the analysts’ team of JEPI will conduct a fundamental bottom up approach to select only stocks that are considered undervalued.

Advantages

JEPI, an ETF focused on issuing call options, offers several advantages that might appeal to certain investors. Firstly, it boasts an attractive yield derived from the money earned through call option writing. Moreover, JEPI exhibits lower volatility compared to investing directly in an S&P 500 index ETF like SPY, making it a suitable option for conservative investors and income seekers.

Another positive aspect of JEPI is its ability to capitalize on high volatility, which often translates to increased premiums for the fund. Additionally, investors can save valuable time and effort by avoiding the need to personally write call options on the S&P 500, as JEPI handles this strategy on their behalf. Furthermore, with relatively low fees of 0.35% total expense ratio, JEPI presents a cost-effective investment choice. The ETF’s diversification across various sectors adds another layer of appeal, spreading risk across different industries.

However, JEPI does have some drawbacks that potential investors should consider. In bull markets, it is expected to underperform the S&P 500 index due to the call option writing strategy, which reduces volatility but also limits its performance during bullish periods.

Recap

Positives

Attractive yield thanks to money earned issuing call options;

Lower volatility than investing in a S&P500 index ETF such as SPY;

Suits conservative investors and income seekers;

High volatility usually increases the premiums earned by the fund;

Saves you time and effort (if you were yourself interested on writing call options on the S&P 500);

Relatively low fees (0.35% total expense ratio);

Diversification: JEPI is highly diversified across various sectors.

Negatives

In bull market, investors should expect a lower performance than the S&P 500 index. Issuing call options reduces volatility at the expense of higher performance in bull markets;

JEPQ

Investment objective

JEPQ (JPMorgan Nasdaq Equity Premium Income ETF) is a high distribution yield ETF. It focuses on providing investors with a monthly income stream using covered call strategies. These strategies enhance yield by collecting premiums on call options. JEPQ invests in large cap Teck stocks that are part of the NASDAQ. Using a proprietary selection criteria, the manager would select companies with the highest prospects for growth seeking the highest adjusted return possible (low volatility combined with high returns).

Advantages

JEPQ ETF, focused on writing call options on the NASDAQ 100, offers similar benefits to JEPI. It provides an attractive yield from call option writing and boasts lower volatility compared to a NASDAQ 100 ETF like QQQ, appealing to conservative investors and income seekers.

However, JEPQ has some significant negatives that investors need to be aware of. It tends to perform poorly during bullish market conditions, as the covered call strategy curtails the upside potential of the NASDAQ 100.

Furthermore, JEPQ’s lack of diversification is a notable concern, with a heavy concentration in tech firms dominating the fund. This lack of diversification exposes investors to higher risks compared to a more balanced investment approach.

Recap

Positives

Attractive yield thanks to money earned issuing call options;

Lower volatility than investing in a NASDAQ 100 ETF such as QQQ;

Suits conservative investors and income seekers;

High volatility usually increases the premiums earned by the fund;

Saves you time and effort (if you were yourself interested on writing call options in the NASDAQ 100;

Relatively low fees (0.35% total expense ratio).

Negatives

Poor performance (compared to the index in bull markets). You are essentially giving up on the upside potentiel of the NASDAQ 100;

The strategy of covered calls becomes ineffective in an unpredictable market;

JEPQ is dominated by Tech firms so it’s far from being a diversified investment;

Yahoo finance as of December 10th

Conclusion

Ultimately, whether JEPI or JEPQ is a good investment depends on individual investor preferences, risk tolerance, and market outlook. JEPI’s lower volatility and diversification across sectors could be attractive to those seeking stability and income, while JEPQ’s focus on the NASDAQ 100 may appeal to tech-focused investors. It is crucial for investors to conduct thorough research, consider their financial goals, and consult with a financial advisor to make informed investment decisions.

Dividend investing is one of the most popular strategies in personal finance. The idea is simple: own shares in profitable companies, and those companies pay you a portion of their earnings on a regular basis — monthly, quarterly, or annually. You build wealth and generate income simultaneously.

For Muslim investors, the question is whether this strategy is compatible with Islamic finance principles. The answer, as with most things in halal investing, depends on the details.

The short answer: yes, dividend investing can be halal — but not all dividends are created equal. The permissibility depends on what company is paying the dividend, how that company earns its money, and whether the dividend itself represents a share of real business profits.

What Is a Dividend — And Why It Matters for Halal Investing

A dividend is a distribution of a company’s profits to its shareholders. When a company earns more money than it needs to reinvest in its business, it can return that surplus to the people who own shares.

From an Islamic finance perspective, this is fundamentally different from interest. Interest is a guaranteed, predetermined payment that has no connection to actual business performance. A dividend, by contrast, is a share of real profit — it goes up when the business does well, it can be cut or eliminated when the business struggles, and it reflects genuine economic activity.

This distinction — profit-sharing versus interest — is at the heart of why dividend investing can be permissible while bond investing is not.