If you are looking to invest in the US stock market while staying aligned with Islamic finance principles, you have likely come across SPUS. It is one of the most popular halal ETFs available today, often seen as the go-to option for Sharia-compliant exposure to large US companies.

But is SPUS truly a strong long-term investment, or is it simply a filtered version of the S&P 500 with limitations investors often overlook? In this complete review, we will break down how SPUS works, what it holds, its performance, risks, and whether it deserves a place in your halal portfolio.

What is SPUS ETF?

SPUS, officially known as the SP Funds S&P 500 Sharia Industry Exclusions ETF, is a US-listed ETF designed to provide exposure to large-cap American companies while following Sharia-compliant investment principles.

In simple terms, SPUS tracks a modified version of the S&P 500 but removes companies that do not meet Islamic finance guidelines.

This includes:

Conventional banks and financial institutions

Companies with high levels of debt

Businesses involved in prohibited industries such as alcohol, gambling, or tobacco

The result is a portfolio that focuses heavily on growth-oriented companies, particularly in sectors like technology.

For halal investors, this offers a structured and accessible way to participate in the US equity market without compromising their values.

How SPUS Stays Sharia-Compliant

SPUS follows a multi-step screening process to ensure compliance with Islamic finance principles.

1. Industry Screening

The first step removes companies involved in non-compliant activities such as:

Interest-based financial services

Alcohol and tobacco

Gambling

Adult entertainment

This immediately eliminates a significant portion of the traditional market, especially the financial sector.

2. Financial Ratio Screening

The second step focuses on financial health. SPUS excludes companies that:

Have excessive debt levels

Generate significant income from interest

This is critical because Islamic investing avoids businesses that rely heavily on interest-based financing.

3. Purification Process

Even after screening, some companies may still earn a small portion of non-compliant income.

To address this, SPUS applies a purification process where a small percentage of income is identified. Investors are expected to donate this portion to maintain full compliance.

What Does SPUS Hold?

One of the most important aspects of any ETF is its underlying holdings.

Because SPUS excludes financials and other sectors, its portfolio looks quite different from the traditional S&P 500.

Top Holdings

SPUS is heavily concentrated in large technology and growth companies, including:

Apple

Microsoft

Nvidia

Amazon

Meta

Alphabet

These companies tend to have strong balance sheets and lower reliance on debt compared to traditional financial institutions.

Sector Allocation

The ETF has:

High exposure to technology

Reduced exposure to financials

Limited diversification across certain sectors

This creates a unique profile compared to traditional index ETFs.

Performance Overview

SPUS has delivered strong performance over recent years and has even outperformed the S&P 500 during certain periods.

The main reason is sector exposure. Because SPUS is heavily weighted toward technology and growth stocks, it has benefited from the strong performance of these sectors. Companies like Nvidia and Microsoft have been major drivers of returns, boosting overall performance.

Important Reality

However, this outperformance is not guaranteed.

If technology stocks underperform

If financial sectors outperform

SPUS may lag behind the broader market.

Fees and Expense Ratio

SPUS has an expense ratio of approximately 0.49 percent.

This is significantly higher than traditional S&P 500 ETFs, which often have fees below 0.10 percent.

Why Higher Fees?

The additional cost comes from:

Sharia screening processes

Ongoing compliance monitoring

Portfolio adjustments

Should You Be Concerned?

While fees do impact long-term returns, many investors accept higher costs in exchange for investing in a way that aligns with their values.

The key is understanding what you are paying for.

Key Advantages of SPUS

1. Halal Compliance

SPUS provides a straightforward way to invest in the stock market while respecting Islamic principles.

2. Access to US Market Growth

You gain exposure to some of the largest and most innovative companies in the world.

3. Simplicity

Instead of selecting individual halal stocks, SPUS offers a ready-made solution.

4. Strong Growth Potential

The ETF is positioned toward sectors that have historically delivered strong long-term returns.

SPUS vs S&P 500

Understanding the difference between SPUS and the traditional S&P 500 is essential.

S&P 500

Fully diversified

Includes all sectors

Strong exposure to financials

SPUS

Sharia-compliant filtering

Excludes financial sector

More concentrated portfolio

Key Trade-Off

The real difference is not performance versus underperformance.

It is: 👉 Growth exposure versus diversification

Risks to Consider

Like any investment, SPUS comes with risks.

1. Market Risk

SPUS is still an equity ETF. Its value can fluctuate with market conditions.

2. Sector Concentration

Heavy exposure to technology means:

Higher upside potential

Higher downside risk

3. Reduced Diversification

Excluding financials limits diversification compared to traditional ETFs.

4. Sharia Constraints

Because the investable universe is smaller, SPUS may miss opportunities available in the broader market.

Who Should Invest in SPUS?

SPUS is best suited for:

✔ Halal investors

Those who want to invest while following Islamic principles.

✔ Long-term investors

Investors focused on growth over time.

✔ Passive investors

Those who prefer a simple ETF instead of selecting individual stocks.

Who Should Avoid SPUS?

SPUS may not be ideal for:

Investors seeking maximum diversification

Investors focused on low fees

Those uncomfortable with sector concentration

Final Verdict: Is SPUS Worth It?

SPUS is one of the most accessible and well-structured halal ETFs available today.

It offers a powerful combination of:

Market exposure

Simplicity

Sharia compliance

However, it is not a perfect replacement for the S&P 500.

The Reality

SPUS is not about outperforming every index.

It is about:

👉 Investing with conviction 👉 Aligning your portfolio with your values

Video

🧠 Final Insight

For many investors, the best approach is not choosing between SPUS and other ETFs.

It is building a balanced halal portfolio that includes:

This content is for educational purposes only and does not constitute financial advice. Always conduct your own research before making investment decisions.

Canadian investors are increasingly interested in dividend stocks. And it makes sense: they offer a powerful double advantage:

Regular income in the form of dividends

Long-term capital growth potential

But not all dividends are created equal. Some companies have a high dividend… only because their stock price has fallen sharply. This is called a “dividend trap” : attractive yield, but dividend at risk of cut-off. That’s why, for 2026, the strategy we’re putting forward is simple:

👉 Prioritizing “quality” over “high yield”

This article focuses on:

financially strong companies

Sustainable and growing dividends

Robust balance sheets

High cash flow generation

In short: companies that are not only able to pay today… but also to continue to increase their dividends tomorrow.

Video

Why focus on “quality” in 2026?

The current economic environment is characterized by:

Interest rates still high

moderate economic growth

Geopolitical risks

Markets that are sometimes very volatile

In this context, high-quality companies offer three major advantages.

1. Protection contre les “yield traps”

Some companies advertise returns of 8%, 9%, 10% or more. This sounds very attractive to an investor looking for income, but such a level of return often hides a less positive reality. In many cases, this high yield is mainly due to a sharp drop in the share price. Since the return is calculated according to the price, when the stock falls, the percentage rises mechanically. It is therefore not necessarily a “good deal”, but sometimes a warning signal.

These companies often combine fragile profits with high debt. When profits fall or interest rates rise, it becomes difficult to maintain a high dividend. The consequence is known:

❌ Fall in the share price❌, reduction or cut of the dividend, lasting❌ loss for the investor

In their case, the dividend is sustainable and becomes a real tool for long-term wealth creation, rather than a hidden risk. The conclusion is clear: a reasonable and reliable dividend is better than an exceptionally high yield built on shaky foundations.

2. Stability of payments

Investors are increasingly looking for:

Predictability

Regular income

Low dividend volatility

Quality companies tend to:

✔ Weathering recessions ✔ Adjusting capital intelligently ✔ Maintaining dividends even in difficult times

3. Capital Growth Potential

Dividends represent only a portion of the total return on a stock market investment. The other essential component is the appreciation of the stock price over time. A quality investment is therefore not limited to receiving regular payments: it must also allow the value of the security to increase sustainably.

Strong companies often share several characteristics: they innovate, develop new products, improve efficiency, and defend strong competitive positions. They generate significant and recurring cash flows, which allows them to finance their growth, reduce their debt and remunerate shareholders. They intelligently reinvest their profits: modernization, expansion, targeted acquisitions, or share buybacks.

These companies thus offer a double efficiency engine :

For the patient investor, this combination is powerful. The dividend provides regular income, while the increase in the share price helps build wealth. This is why focusing only on the dividend rate can be misleading: it is better to favor companies that can grow their earnings, dividends and stock market value over time.

How we selected the titles: the “high quality” factor

Our criteria are based on the “Quality” factor studied by Fidelity and other institutional managers. It is based on four concrete financial pillars.

✔ 1. Strong balance sheets

We give priority to companies:

Well capitalized

with cash

Shock-absorbing

A strong balance sheet means:

👉 Ability to maintain the dividend even during a crisis

We favour companies with strong balance sheets, well capitalised and sufficient liquidity to weather difficult times. Such a financial profile offers significant room for manoeuvre in the event of a recession, a rise in interest rates or a sector shock. These companies can continue to invest, repay their debts and maintain their dividends without having to resort to emergency financing. In concrete terms, a strong balance sheet means the ability to absorb crises without massive shareholder dilution or abrupt cuts in payouts. For a dividend investor, this is a central criterion: it increases income security and sustainability.

✔ 2. Predictable cash flows

The selected companies show:

Recurring cash flows

from core or dominant activities

Examples:

Infrastructure energy

Big banks

Mining royalties

The successful companies generate stable and recurring cash flows, often from core or dominant activities in the economy. This type of cash flow makes it possible to simultaneously finance dividends, investments and debt reduction. It is frequently found in sectors such as energy infrastructure, large banks, telecommunications or mining royalties. The predictability of receipts greatly reduces the risk of dividend cuts. It also allows managers to gradually increase payments over time. For the long-term investor, this visibility is a major asset, as it promotes steady, growing and sustainable returns.

✔ 3. High profitability

We looked for companies that could:

Generate high margins

Turning revenue → profit

Financing Growth + Dividends

We look for companies that can effectively convert their revenues into net profits. High profitability translates into strong margins, disciplined cost management and the ability to maintain their prices even in challenging economic environments. These companies can finance their organic growth, make strategic acquisitions and continue to remunerate their shareholders through higher dividends. Sustainable profitability is also a sign of competitive advantage: a strong brand, a dominant network, unique assets or differentiated technology. For the investor, this means a greater likelihood of long-term value creation, beyond just the current return.

✔ 4. Debt under control

Low debt allows:

Greater strategic flexibility

resistance to rising rates

Controlled debt allows companies to remain flexible when economic conditions deteriorate or interest rates rise. Interest costs that are too high can eat into profits and threaten the dividend. Conversely, reasonable debt allows you to invest, acquire and weather economic cycles without undue pressure. Firms with low debt are less vulnerable to banks, markets, and costly refinancing. They can continue to pay their dividends even when the environment becomes more difficult. For an income-oriented portfolio, financial discipline is therefore a key factor in stability and resilience.

The 7 Best Canadian Dividend Stocks for 2026

1. Enbridge (ENB) — The Energy Infrastructure Pillar

Enbridge is one of Canada’s most popular companies among dividend investors. It operates an extensive network of:

pipelines

Gas infrastructure

Energy utilities

Why does it stand out?

✔ Dividend announced to increase towards 2026 ✔ More than 30 consecutive years of relatively ✔ predictable increase in cash flow distributed

The dividend is based on distributable cash flow (DCF), estimated between:

👉 $5.70 and $6.10 per share for 2026 (guidance)

Investment thesis

regulated activity

Structural energy demand

Long-term infrastructure projects

Enbridge operates in a largely regulated business, making its revenue streams more predictable than those of many energy companies. It benefits from a structural energy demand, linked to the transport of oil and gas necessary for the functioning of the North American economy. Its long-term infrastructure projects provide high visibility into future cash flows through often multi-year contracts. For these reasons, Enbridge is particularly appealing to investors who are looking for stability, resilience and a gradual increase in dividend over time, rather than rapid but uncertain growth.

2. Royal Bank of Canada (RY) — The Canadian Banking Reference

RBC is the country’s largest bank by market capitalization.

It benefits from:

of a dominant national network

an international presence

an image of solidity

Why is RY a “quality” stock?

✔ Uninterrupted dividends for more than 150 years ✔ High profitability ✔ Income diversification (retail banking, insurance, capital markets)

Its yield is not the highest in the industry, but:

👉 It is among the most reliable

Investment thesis

• Strong brand franchise

• Essential positioning

• Balance sheet strength

Royal Bank of Canada has an extremely strong brand franchise, built on more than a century of history and a dominant presence in the country. Its key positioning in personal, commercial and wealth management banking provides it with diversified and resilient revenue streams. The bank also stands out for the strength of its balance sheet, with high capital ratios and prudent risk management. RY is particularly suitable for long-term investors who are looking for security, consistency and regularity of the dividend, rather than speculative bets on more volatile securities.

3. Toronto-Dominion Bank (TD) — North American Growth

TD combine :

Strong Canadian platform

huge presence in the United States

It is one of the banks most exposed to the US market.

Key Points

✔ Yield around 4% ✔ Valuation has become attractive again after recent ✔ challenges Business model focused on retail banking

Investment thesis

future growth related to the United States

Recurring retail profits

Ability to Navigate Economic Cycles

The Toronto-Dominion Bank has significant growth leverage with its strong presence in the U.S., where it continues to expand its retail business. Its recurring profits from retail banking provide a stable revenue base that is less dependent on short-term capital markets. TD has repeatedly demonstrated its ability to navigate economic cycles, maintaining prudent risk management and disciplined capital policy. This stock is particularly suitable for investors looking for both a regular dividend and the potential for a medium-term recovery when economic conditions improve.

Build a reliable monthly income from your portfolio

I’ve created ready-to-use ETF portfolios and a passive income calculator designed specifically for Canadian investors.

4. Canadian Natural Resources (CNQ) — La machine à cash-flow

CNQ is one of the most profitable energy companies in the country.

Why does CNQ attract?

✔ Yield around 5% ✔ 23 consecutive years of dividend ✔ increase Low operating costs

CNQ is recognized for its financial discipline:

Deleveraging

Share buybacks

distributions progressives

Investment thesis

High correlation to the price of oil

Low-cost production

Shareholder-oriented management

Canadian Natural Resources (CNQ) remains highly correlated with the price of oil, which can lead to sharp swings in the stock in the short term. However, the company stands out for its very low-cost production, which allows it to remain profitable even when energy prices fall. Its management adopts a clear management approach to shareholders, combining debt reduction, share buybacks and regular dividend increases. This makes CNQ a flagship stock for investors who accept volatility in exchange for growing dividends and long-term value creation potential.

5. Power Corporation of Canada (POW) — The Heritage Conglomerate

Power Corp owns:

Great-West Lifeco

IGM Financial

Wealthsimple (partial)

Why is POW interesting?

✔ Returns often higher than banks ✔ Global exposure to asset ✔ management Diversified holding structure

Investment thesis

Profits linked to the global financial markets

Growth through acquisitions and subsidiaries

Profits redistributed via dividends

Power Corporation (POW) derives a large portion of its profits from global capital markets through its significant holdings in wealth management and insurance. Its model is based on growth through acquisitions and the development of its subsidiaries, which allows it to diversify its revenue sources and smooth out economic cycles. A significant portion of profits is returned to shareholders in the form of dividends, supported by strong cash flows. POW is therefore particularly attractive to investors who are looking for high returns, geographic and sector diversification, and a long-term stability approach.

6. Bank of Nova Scotia (BNS) — Highest Yield of the Big Banks

Historically, BNS has offered the most generous bank dividend among Canada’s major banks.

Why does SNB attract despite the challenges?

✔ high ✔ performance international presence (especially Latin America) ✔ strategic recovery plan underway

Points of vigilance

Exposure to emerging markets

Restructuring still in place

The Bank of Nova Scotia (NBS) is unique in its strong exposure to emerging markets, particularly in Latin America, which provides it with superior long-term growth opportunities, but with more volatility. The bank is also engaged in a strategic restructuring that is still being rolled out, aimed at improving its profitability, strengthening its risk management and refocusing its activities on its most profitable markets. On the other hand, this adjustment phase can create short-term stock market fluctuations. SNB is therefore mainly aimed at investors who accept a little more risk in exchange for a generally above-average dividend yield.

7. Labrador Iron Ore Royalty (LIF) — Les redevances minières

Unlike traditional mining producers, LIF generates revenue through a royalty model.

It benefits from iron ore sales without directly assuming the costs of operating a mine.

What makes LIF unique?

✔ High ✔ margins, commodity-price-sensitive dividend, ✔ low operating debt

Investment thesis

correlated with iron ore price

Few heavy assets to manage

Good redistributive capacity

Labrador Iron Ore Royalty (LIF) is highly correlated with the price of iron ore, which means that its revenue and distributions can fluctuate with commodity cycles. Its business model is unique: the company holds royalties and therefore few heavy assets to manage, which limits operating costs and operational risks. Thanks to this lean structure, LIF often has a good redistribution capacity in the form of variable dividends. This stock may be attractive to investors looking to add sector diversification related to natural resources, while benefiting from attractive income potential.

Comparison

Stock

Yield

Strength

Risk Level

ENB

~7%

Stable cash flow

Medium

RY

~4%

Strong balance sheet

Low

TD

~4%

US growth

Medium

CNQ

~5%

Cash machine

Cycle risk

POW

~5%

Diversified

Medium

BNS

~6%

High yield

Higher risk

LIF

Variable

Royalty model

High

Conclusion — Dividends yes… but with quality

For 2026, the most reasonable strategy is to focus on strength rather than the search for maximum return at all costs. The aim is to select companies that can maintain and increase their dividends over time, even in times of economic volatility. This means focusing on companies with strong balance sheets, stable cash flows and controlled debt. Conversely, it is prudent to avoid “high-yield traps” – securities that offer very attractive rates but are based on fragile or over-leveraged models.

The seven companies selected—Enbridge, RBC, TD, Canadian Natural Resources, Power Corporation, The Bank of Nova Scotia and Labrador Iron Ore Royalty—embody this central idea: financial quality remains a long-term investor’s best ally. They combine a strong competitive position, the ability to generate cash flow and discipline in the distribution of dividends. This approach does not promise quick wealth, but it does prioritize income sustainability and incremental capital growth. In 2026 and beyond, building wealth is above all about patience, diversification and the rigorous selection of solid companies.

Educational clause

This article is intended to be informative and educational. It does not constitute a recommendation to buy or sell. Each investor should evaluate:

their risk tolerance

its investment horizon

their personal situation

and consult a professional if necessary.

High-income ETFs have become extremely popular with investors looking for monthly cash flow, especially in an environment where market volatility remains elevated and traditional bonds no longer feel “safe enough.”

Among all income ETFs, JEPI and QYLD are two of the most discussed — and most misunderstood.

Both use covered call strategies to generate income. Both offer attractive yields. But their risk profiles, return drivers, and long-term outcomes are very different.

This article breaks down JEPI vs QYLD in plain English, without hype, and explains which ETF fits which type of investor.

Video

What Is a Covered Call Strategy?

Before comparing JEPI and QYLD, it’s critical to understand how covered calls actually work.

A covered call strategy involves owning a portfolio of stocks and selling call options on those holdings. The investor collects option premiums as income in exchange for agreeing to sell the stocks at a predetermined price, which partially caps the portfolio’s upside in strong market rallies.

Why Investors Use Covered Calls

Covered call strategies are most effective in flat, choppy, or slowly rising markets, where stock prices move within a relatively narrow range. In these conditions, option premiums provide a steady source of income, and the risk of missing large upside moves is limited. Investors are essentially being paid for giving up a portion of future gains that may never materialize if markets remain range-bound.

However, covered calls tend to underperform during strong bull markets and explosive rallies. When stocks surge sharply higher, the upside is capped by the call options that were sold, meaning the investor sacrifices capital appreciation in exchange for earlier income. This opportunity cost becomes more visible during sustained market advances, particularly in high-growth segments like technology.

This fundamental trade-off — income today versus growth tomorrow — sits at the core of the JEPI versus QYLD debate. JEPI prioritizes smoother income with some flexibility, while QYLD maximizes current cash flow at the expense of long-term growth potential.

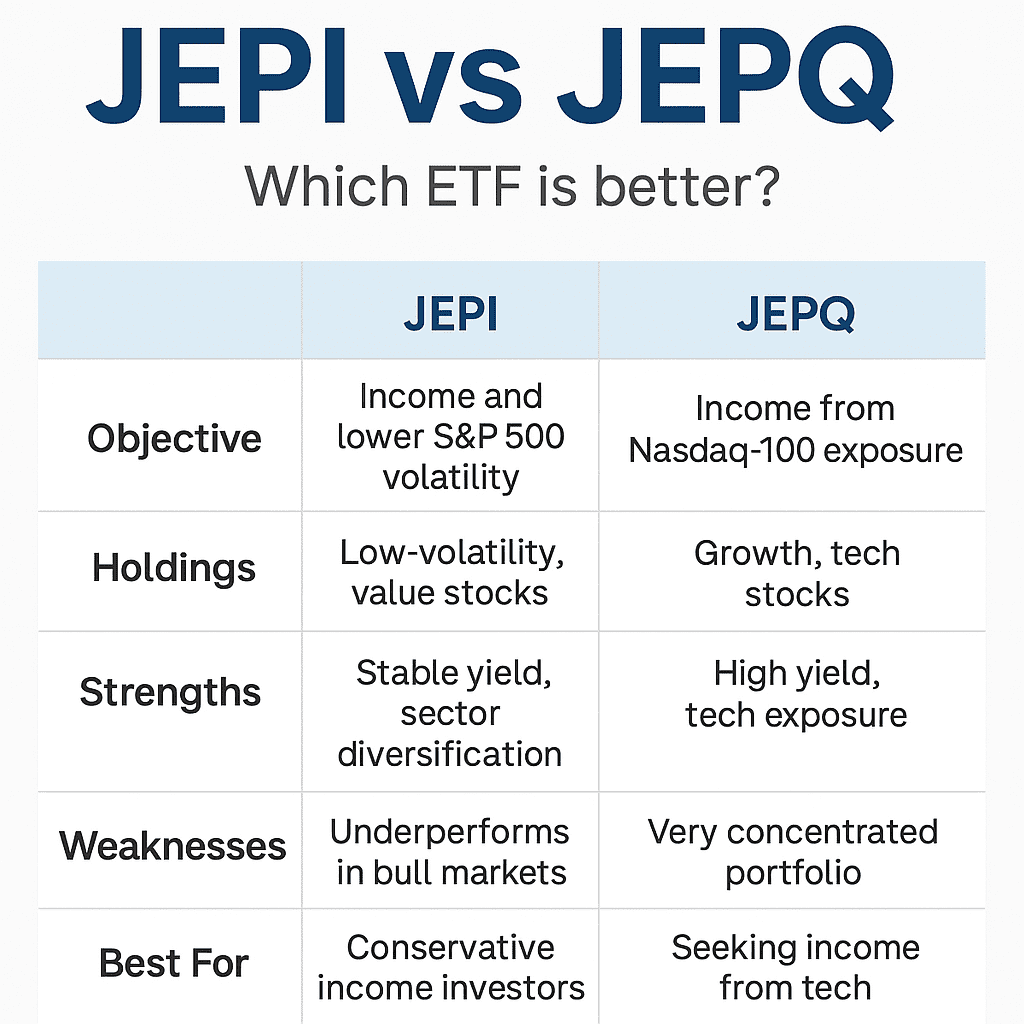

JEPI vs QYLD at a Glance

Feature

JEPI

QYLD

Index Exposure

S&P 500 (low volatility stocks)

Nasdaq 100

Strategy

Active + ELNs

Systematic ATM calls

Yield Range

~7–9%

~12–14%

Volatility

Lower

Higher

Growth Potential

Moderate

Limited

Expense Ratio

~0.35%

~0.60%

Management Style

Active

Passive

At first glance, QYLD looks “better” because of its higher yield. But yield alone does not tell the full story.

Underlying Index: Stability vs Volatility

JEPI: Defensive S&P 500 Exposure

JEPI focuses on low-volatility stocks within the S&P 500, emphasizing sectors such as consumer staples, healthcare, financials, and other defensive large-cap companies. These businesses tend to have stable cash flows, resilient demand, and lower sensitivity to economic slowdowns, which makes them well suited for an income-oriented strategy.

By prioritizing stability over aggressive growth, JEPI aims to reduce drawdowns during periods of market stress. When broader equity markets experience sharp declines, defensive stocks generally fall less, helping preserve capital. This positioning also supports a more consistent income profile, as option premiums and dividends are generated from less volatile underlying assets.

The result is lower overall volatility, smoother and more predictable income, and less capital erosion over time compared to higher-beta strategies. For investors seeking dependable monthly cash flow with reduced downside risk, JEPI’s defensive stock selection plays a critical role in its long-term risk-adjusted performance

QYLD: Nasdaq 100 Exposure

QYLD is tied to the Nasdaq 100, an index that is heavily weighted toward technology and growth-oriented companies. While these stocks offer strong long-term growth potential, they also come with significantly higher volatility and greater sensitivity to changes in interest rates, earnings expectations, and market sentiment.

This elevated volatility allows QYLD to generate larger option premiums, which supports its high headline yield. However, the trade-off is meaningful. During market downturns, Nasdaq-focused portfolios tend to experience deeper drawdowns, and covered call income is often insufficient to fully offset those losses. Over time, consistently capping upside in a volatile growth index can result in long-term capital decay.

This structural difference — defensive low-volatility exposure versus high-beta growth exposure — explains much of the persistent performance gap between JEPI and QYLD across full market cycles.

Strategy Mechanics: Active vs Mechanical

JEPI’s ELN-Based Approach

JEPI does not rely on a simple, mechanical covered call overlay on its stock holdings. Instead, it holds a diversified portfolio of large-cap U.S. equities and generates income primarily through Equity-Linked Notes (ELNs). These instruments are structured to provide option-like income while giving the portfolio manager greater flexibility in how and when upside is capped.

Because JEPI’s strategy is actively managed, exposure can be adjusted based on prevailing market conditions. In stronger or trending markets, the fund can reduce the degree of upside capping, allowing investors to participate more in equity appreciation. In contrast, during volatile or uncertain periods, income generation can be emphasized to enhance cash flow and stability.

This dynamic approach helps preserve capital more effectively, smooth returns across market cycles, and adapt income levels as volatility rises or falls. As a result, JEPI offers a more balanced income strategy than traditional systematic covered call ETFs.

QYLD’s Systematic ATM Calls

QYLD follows a strict, mechanical covered call strategy with no active decision-making. Each month, the fund sells at-the-money call options on the Nasdaq 100, regardless of market conditions, volatility levels, or broader economic trends. There is no discretion involved and no attempt to adjust strike selection or exposure when markets are trending strongly or experiencing regime changes.

This rigid structure produces high and relatively predictable monthly income, which is the primary appeal of QYLD. Option premiums from a volatile, tech-heavy index support an elevated yield that many income-focused investors find attractive. However, this benefit comes with clear trade-offs.

Because calls are sold at the money every month, upside is consistently capped, even during sustained bull markets. When the Nasdaq rallies, those gains are effectively exchanged for short-term income. Over time, this creates structural long-term underperformance in rising markets, particularly when growth stocks lead broader equity returns.

QYLD’s design prioritizes cash flow certainty over adaptability. It is built for investors who value immediate income and predictability, not for those seeking capital appreciation or long-term wealth growth.

Yield Comparison: Why Higher Is Not Always Better

JEPI Yield: 7–9%

JEPI’s yield is:

Lower than QYLD

More stable

Less destructive to capital

Its distributions fluctuate, but over time remain relatively consistent.

QYLD Yield: 12–14%

QYLD’s yield is:

Eye-catching

Very high

Partially a return of capital in many periods

A key issue with QYLD is that:

Income stays high

Net asset value (NAV) trends downward over long horizons

This creates the illusion of sustainability while slowly eroding principal.

Capital Growth and Total Return

JEPI: Income with Partial Growth

JEPI is structured to deliver consistent income while still preserving a degree of long-term growth. Unlike fully systematic covered call strategies, JEPI allows for some upside participation, particularly during moderately rising markets. Because the fund holds high-quality, dividend-paying companies, investors also benefit from dividend growth generated by the underlying equity portfolio. Over time, this combination of option income and equity returns contributes to a stronger long-term total return profile compared to more aggressive income products.

Across full market cycles, JEPI has historically demonstrated greater resilience. It tends to lose less during bear markets, supported by its defensive stock selection and flexible option strategy. When markets recover, JEPI often rebounds faster, as less upside is permanently forfeited. This balance between income generation and capital preservation helps investors maintain purchasing power more effectively, particularly in inflationary environments where pure income strategies may fall behind.

QYLD: Income at the Expense of Growth

QYLD takes a fundamentally different approach. Its strategy sacrifices growth almost entirely in exchange for maximum current income. By selling at-the-money calls on the Nasdaq 100 every month, upside is capped continuously, regardless of market strength. As a result, major technology rallies rarely translate into meaningful net asset value (NAV) growth.

Over long periods, this structure can be detrimental. While distributions remain high, capital erosion and inflation gradually reduce real returns. QYLD is therefore not designed for wealth accumulation or long-term purchasing power preservation. It functions strictly as a cash distribution vehicle, best suited for investors who prioritize immediate income and fully understand the long-term trade-offs.

Volatility and Risk Profile

JEPI: Lower Volatility

JEPI is designed with risk control as a central objective. It benefits from defensive stock selection, focusing on lower-volatility companies within the S&P 500 that tend to be more resilient during economic slowdowns. This is complemented by active option management, which allows the fund to adjust income generation and exposure based on market conditions rather than following a rigid rule set. Combined with its lower beta profile, JEPI typically experiences smaller price swings than the broader equity market.

This risk-aware construction makes JEPI particularly suitable for retirees, conservative income investors, and portfolios that prioritize capital stability alongside monthly income. The goal is not to eliminate volatility entirely, but to reduce it enough that income remains dependable through different market environments.

QYLD: Higher Volatility

Despite being marketed as an income ETF, QYLD can be surprisingly volatile. Its exclusive exposure to the Nasdaq 100 means drawdowns can be severe, especially during technology-led market corrections. Covered call income offers limited protection in these scenarios, as selling calls does not shield investors from sharp downside moves. In deep declines, option premiums are often insufficient to offset capital losses.

As a result, QYLD behaves less like a defensive income fund and more like a yield-enhanced technology product, with higher risk and greater sensitivity to market cycles.

Expense Ratios and Cost Efficiency

JEPI: ~0.35%

QYLD: ~0.60%

JEPI is:

Actively managed

Cheaper

More efficient

QYLD charges a higher fee for a fully mechanical strategy — something investors should factor into long-term returns.

Tax Considerations (High-Level)

Distributions from both ETFs are:

Mostly non-qualified

Often classified as ordinary income or return of capital

This makes them:

Less tax-efficient in taxable accounts

Better suited for tax-advantaged accounts (RRSP, IRA)

Tax treatment varies year to year, so investors should review official distribution breakdowns.

When JEPI Makes Sense

Choose JEPI if you:

Want consistent monthly income

Prefer lower volatility

Care about long-term capital preservation

Are building a core income position

JEPI works well as:

A retirement income foundation

A stabilizer in a broader portfolio

A defensive income ETF during uncertain markets

When QYLD Makes Sense

Choose QYLD if you:

Need maximum current cash flow

Are comfortable with NAV erosion

Understand the trade-offs

Use it as a satellite position, not a core holding

QYLD can be useful for:

Short-term income needs

Cash-flow-focused strategies

Investors who reinvest distributions elsewhere

The Best Strategy: Blend, Don’t Bet

For many investors, the optimal approach is not JEPI or QYLD, but a blend:

JEPI for stability and durability

A higher-yield ETF (like QYLD or alternatives) for incremental income

This balances:

Income

Risk

Capital preservation

The mistake is going all-in on maximum yield without understanding the long-term cost.

Final Verdict: JEPI vs QYLD

JEPI is the better choice for:

Sustainable income

Risk-adjusted returns

Long-term portfolios

QYLD is suitable for:

Aggressive income seekers

Tactical allocations

Investors who fully understand capital decay

For income-focused investors in Canada and the United States, covered call ETFs have gained massive popularity as a source of predictable monthly income. With assets under management reaching tens of billions of dollars, these strategies appeal to investors seeking cash flow and smoother returns in uncertain markets.

However, high income always comes with trade-offs. So how do covered call ETFs really work, and when do they make sense in a portfolio?

Executive Summary

Why Covered Call ETFs Are So Popular

High Income Potential

One of the main reasons covered call ETFs have become so popular is their ability to generate significantly higher income than traditional dividend ETFs. These funds boost cash flow by selling call options on their underlying holdings. The option premiums collected are distributed to investors, often resulting in yields well above standard equity income strategies.

While traditional dividend ETFs typically yield between 2% and 4%, covered call ETFs frequently offer 7% to 12% or more, depending on market conditions and how aggressively calls are written. This makes them especially attractive for investors who prioritize income over capital appreciation, such as retirees or those seeking predictable cash flow.

Lower Volatility Than Holding Stocks Directly

By selling upside potential in exchange for income, covered call ETFs tend to deliver a smoother return profile. The option premiums act as a partial buffer during sideways or mildly negative markets, helping reduce overall volatility compared to owning the underlying stocks outright.

This characteristic makes covered call ETFs appealing to investors who want equity exposure but prefer less dramatic market swings.

Predictable Monthly Cash Flow

Most U.S. covered call ETFs pay monthly distributions, which is a key advantage for income-focused investors. Regular payments simplify budgeting and portfolio planning, making these ETFs popular among retirees and those relying on investment income.

⚠️ Important Trade-Off The downside of this strategy is limited upside participation. In strong bull markets, covered call ETFs usually underperform their underlying indexes because gains above the option strike price are capped. As a result, they are best viewed as income tools, not long-term growth engines.

*Yields are indicative and can fluctuate significantly.

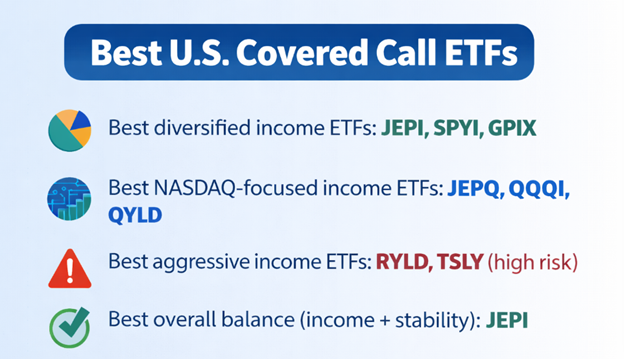

Best Diversified U.S. Covered Call ETFs

JEPI – The Gold Standard for Income Stability

JEPI is widely regarded as one of the most balanced U.S. covered call ETFs available. Rather than selling call options directly on the index, it uses a combination of equity-linked notes (ELNs) and active management to generate income while aiming to preserve capital. This structure allows JEPI to deliver consistent monthly income with lower volatility than traditional equity exposure.

While upside participation is more limited than a pure equity ETF, JEPI provides strong downside protection and a smoother return profile, making it well suited for income-focused investors.

Best for: Investors seeking stable income with lower risk.

SPYI – Higher Yield, More Aggressive

SPYI applies a more systematic covered call strategy on the S&P 500, writing options more aggressively than funds like JEPI. This approach typically results in higher income, especially during periods of elevated market volatility. The trade-off, however, is greater price fluctuation and less downside protection during market drawdowns. While SPYI can deliver attractive monthly distributions, its returns tend to be more sensitive to market movements than more conservatively managed income ETFs. As a result, SPYI is better suited as a satellite holding rather than a core income position.

Best for: Income investors willing to accept higher volatility in exchange for higher yield.

GPIX – Low Fees, Conservative Approach

GPIX stands out primarily for its very low expense ratio (0.29%), making it one of the most cost-efficient covered call ETFs in the U.S. market. Its premium-income strategy is more conservative, prioritizing capital preservation and steady income rather than maximizing yield. As a result, GPIX typically offers lower distributions than more aggressive peers, but with a smoother risk profile and improved long-term efficiency. This makes it an appealing option for investors who value cost control and stability over headline yield.

Best for:Cost-conscious investors prioritizing efficiency, discipline, and long-term sustainability over maximum income.

Best NASDAQ-Focused Covered Call ETFs

JEPQ – Tech Income, Done Right

JEPQ applies the same philosophy as JEPI but focuses on the NASDAQ-100, making it one of the most balanced ways to generate income from technology-heavy equities. Instead of writing calls directly on the index, JEPQ uses equity-linked notes (ELNs) and active management to generate option income while aiming to preserve capital. This structure allows the fund to deliver attractive monthly distributions without fully sacrificing downside protection.

Compared to more aggressive NASDAQ covered call ETFs, JEPQ tends to experience lower volatility and better capital stability, particularly during market drawdowns. While upside participation is capped, it is not eliminated entirely, making JEPQ more suitable for long-term income investors than pure buy-write strategies.

Best for: Investors seeking technology exposure with disciplined income generation and a more defensive risk profile.

QQQI – Higher Income, Higher Risk

QQQI is designed to maximize income from the NASDAQ-100 by writing call options more aggressively than funds like JEPQ. This results in higher yields, especially in volatile or range-bound markets, but also introduces greater sensitivity to market swings. The more assertive call-writing approach limits upside participation more quickly and provides less downside cushioning during sharp corrections.

As a result, QQQI can deliver impressive monthly income, but long-term capital preservation is less consistent than with more conservatively managed strategies. Investors should view QQQI as an income-focused satellite holding, rather than a core portfolio position.

Best for: Investors prioritizing maximum income from technology stocks, who are comfortable with higher volatility and capped growth.

QYLD – The Original, But Aging

QYLD is one of the earliest and most widely recognized covered call ETFs, built around a systematic at-the-money (ATM) call-writing strategy on the NASDAQ-100. While this approach produces consistently high income, it has historically resulted in weak long-term capital preservation, as gains are frequently capped and losses are not fully offset.

Over time, this structure has led to limited total return growth compared to newer, more flexible strategies. QYLD remains effective in flat or mildly bearish markets, but it tends to lag significantly during strong bull markets.

Best for:Short-term income seekers focused primarily on cash flow. Not ideal for: Investors targeting long-term total return or capital growth.

Sector & Aggressive Income ETFs

RYLD – Small Caps, Big Yield

RYLD applies a covered call strategy to the Russell 2000, an index composed of U.S. small-cap stocks. Because small caps tend to be more volatile than large caps, option premiums are generally higher, allowing RYLD to generate attractive monthly income compared to large-cap covered call ETFs. This makes RYLD an effective tool for boosting portfolio yield.

However, the higher income comes with greater volatility and weaker capital stability. Small caps are more sensitive to economic cycles, rising interest rates, and market stress, which can lead to larger drawdowns. While the covered call overlay helps monetize volatility, it does not eliminate downside risk.

RYLD works best in range-bound or choppy markets, but it often underperforms during strong small-cap bull markets due to capped upside.

Best for: Investors looking to diversify income sources beyond large caps, with an understanding of the higher risk profile.

TSLY – Extreme Income, Extreme Risk

TSLY is fundamentally different from traditional covered call ETFs. Instead of holding a diversified portfolio, it sells options on a single stock—Tesla. This concentrated approach can produce extremely high yields, especially during periods of elevated volatility, which is common for Tesla shares.

However, this income comes with very high capital risk. Because the strategy depends on one underlying stock, investors are exposed to sharp price swings, long drawdowns, and significant erosion of capital. While monthly distributions can appear impressive, total return can be highly unstable and unpredictable.

TSLY should not be viewed as a long-term income foundation. It is a tactical, speculative instrument, not a diversified ETF.

⚠️ This is not a core income ETF. Best for: Experienced investors who understand the risks and are seeking short-term, high-risk income exposure only.

Final Takeaways

overed call ETFs are best understood as income tools, not long-term growth vehicles. Their primary objective is to convert market volatility into regular cash flow, not to maximize capital appreciation. Investors who approach these ETFs with a growth mindset often end up disappointed, especially during strong bull markets where upside participation is capped.

One of the most important principles to remember is that higher yield usually comes with a higher opportunity cost. ETFs offering double-digit yields often achieve this by writing calls more aggressively or concentrating exposure, which limits upside and can weaken long-term total returns. Yield alone should never be the sole selection criterion.

Among the broad universe of U.S. covered call ETFs, JEPI and JEPQ remain the strongest core holdings. They strike a better balance between income generation, capital preservation, and volatility management, making them suitable as long-term income foundations for many investors.

More aggressive ETFs such as QYLD, RYLD, and TSLY should be treated as satellite positions only. While they can enhance portfolio income in the short term, their higher risk profiles and weaker capital preservation make them unsuitable as core income holdings.

📌 Best strategy: For balanced monthly income, consider blending one diversified covered call ETF (such as JEPI or SPYI) with one technology-focused income ETF (such as JEPQ or QQQI). This approach helps diversify income sources, smooth volatility, and avoid over-reliance on a single strategy.

When used intentionally and in moderation, covered call ETFs can play a valuable role in an income-focused portfolio.

Bottom Line

U.S. covered call ETFs can play a powerful role in an income-focused portfolio, but only when used with clear expectations. They are designed to monetize volatility, not to outperform in bull markets.

Used correctly, they provide:

Reliable cash flow

Lower volatility

Predictable monthly income

Used incorrectly, they can erode long-term returns.

For Canadian investors focused on maximizing income, covered call ETFs have become some of the most popular investment choices. Many of these funds now manage billions of dollars in assets, showing just how much demand there is for predictable cash flow.

But what makes them so attractive for income seekers?

1. High Dividend Yields

Covered call ETFs generate extra income by selling call options on their holdings. The premiums collected can significantly boost distributions, often resulting in yields much higher than traditional dividend ETFs.

2. Smoother Ride (Lower Volatility)

The covered call strategy is designed to provide more stability. By selling upside potential in exchange for income, these ETFs tend to be less volatile than holding the underlying stocks directly.

3. Reliable Passive Income

If your main objective is to earn high monthly or quarterly distributions, covered call ETFs can be an appealing choice. They’re especially popular among retirees and income-focused investors who prioritize cash flow over long-term growth.

⚠️ Important Trade-off: The high yields come at a cost—limited capital appreciation. Because the upside is capped when call options are exercised, these ETFs usually underperform in strong bull markets.

What We’ll Cover in This Post

In this article, we’ll go beyond theory and look at the most popular covered call ETFs in Canada. We’ll break them down into two categories:

Diversified Income ETFs – funds that provide broad exposure across sectors while still generating high income.

Sector-Specific Covered Call ETFs – funds that focus on one sector (like banks, energy, or tech) and use covered calls to maximize income from those industries.

Finally, we’ll highlight our top picks in each category, so you can see which covered call ETFs may fit best into your portfolio.

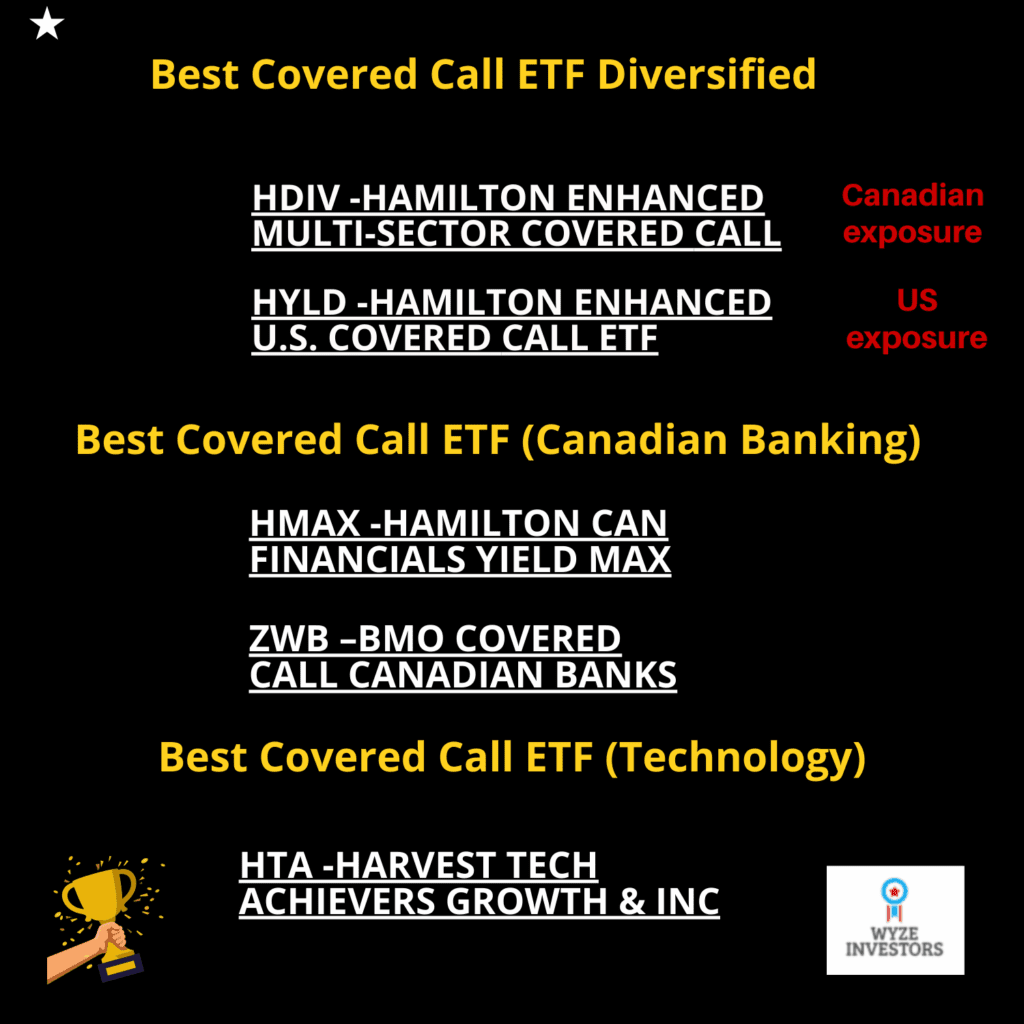

Among the diversified funds, HDIV (Hamilton Enhanced Multi-Sector Covered Call) really stands out. It invests in seven different sector ETFs and adds modest leverage (25%) to enhance both yield and performance. With a 10.02% yield and the best 3-year total return in the group (28.86%), HDIV remains the strongest all-around option for investors who want high monthly income without betting on a single sector.

For those seeking U.S. exposure, HYLD (Hamilton Enhanced U.S. Covered Call) deserves attention. It focuses entirely on U.S. covered call ETFs and, like HDIV, uses 25% leverage. The result is a very attractive 11.78% yield and a strong 3-year total return of 19.45% (with 20.78% over 5 years). This makes HYLD a convenient way for Canadians to tap into U.S. income opportunities without having to piece together multiple funds.

HYLD (Hamilton Enhanced U.S. Covered Call)

HDIF (Harvest Diversified Monthly Income) plays a similar role but without leverage. It’s built as a “fund-of-funds,” spreading investments across banks, utilities, technology, healthcare, and global brands. Its yield remains close to double-digits at 9.97%, and it posted a 3-year total return of 7.94% (5-year data not available). For more conservative income seekers, HDIF can offer peace of mind thanks to a diversified structure and monthly distributions.

ZWC (BMO Canadian High Dividend Covered Call)

If you prefer a purely Canadian option, ZWC (BMO Canadian High Dividend Covered Call) remains a reliable choice. With a 5.93% yield and steady total returns (17.49% over 1 year and 12.27% over 5 years), it offers broad Canadian exposure with a covered call overlay designed to smooth volatility. It won’t match the yield of HDIV or HYLD, but it can be a more conservative, Canadian-focused core income holding.

Finally, HBF (Harvest Brand Leaders Plus Income) offers something different: exposure to global “top brands” combined with a covered call strategy. With a 7.22% yield and a solid 3-year total return of 14.08% (and 9.49% over 5 years), it’s attractive for investors who want blue-chip global exposure while still receiving monthly income.

Verdict – Diversified ETFs (Updated):

Best overall:HDIV, thanks to top-tier diversification and the strongest 3-year performance (28.86%) alongside a 10.02% yield.

Best U.S. play:HYLD, for high monthly income (11.78% yield) plus strong multi-year returns (19.45% / 3Y; 20.78% / 5Y).

Best conservative Canadian core:ZWC, lower yield but steady long-term profile (12.27% / 5Y) and Canadian exposure.

Best Sector-Focused Covered Call ETFs

For investors who want to concentrate on specific industries, banks and technology continue to dominate the sector ETF space.

ZWB (BMO Covered Call Canadian Banks) remains the benchmark. It’s the most established bank covered call ETF built on Canada’s Big Six. With a 5.56% yield and an excellent 3-year total return of 15.66% (and 14.43% over 5 years), ZWB continues to be a strong core option for investors who want Canadian bank exposure with smoother volatility and consistent income.

For those prioritizing maximum cash flow, HMAX (Hamilton Enhanced Canadian Bank ETF) remains hard to beat. Its 12.56% yield is among the highest in the category, supported by aggressive call-writing and leverage. Performance data shows a strong 1-year total return of 21.99% (longer-term data not available). The trade-off remains the same: higher yield usually comes with higher strategy risk and less long-term upside capture.

On the technology side, HTA (Harvest Tech Achievers) remains one of the best “growth + income” covered call ETFs. Even with call-writing capping part of the upside, it has delivered an impressive 5-year total return of 16.02%, while still yielding 8.91%. For investors who want exposure to tech leaders but prefer more stability and monthly income, HTA continues to stand out.

Lastly, ZWK (BMO Covered Call U.S. Banks) provides targeted U.S. financial exposure. With a 6.71% yield, total returns are more modest (6.19% over 1 year, 7.52% over 3 years, 10.04% over 5 years). It can still be useful as a complement for investors who want U.S. bank diversification, but it has lagged Canadian bank options over the last few years.

Verdict – Sector ETFs (Updated):

Best Canadian bank play:ZWB for stability and long-term track record (14.43% / 5Y).

Best high-yield bank play:HMAX for maximum monthly income (12.56% yield) with strong recent performance (21.99% / 1Y).

Best technology play:HTA for a strong blend of income (8.91% yield) and long-term performance (16.02% / 5Y).

📘 Get your free guide to start investing

Includes 4 passive growth portfolios

Final Takeaways

If you want maximum yield, look at HMAX, HYLD, and HDIV, but be aware they rely on leverage and/or more aggressive call-writing.

If you want stability and Canadian exposure, ZWC and ZWB remain solid choices with more moderate yields.

If you want long-term growth with income, HTA and HDIV stand out based on the updated multi-year performance data.

📌 A practical approach for Canadian income investors is to blend diversified funds (HDIV, HYLD, ZWC) with sector-focused ETFs (ZWB, HMAX, HTA) to combine monthly cash flow, diversification, and exposure to sectors that tend to drive returns.

How had Covered call ETF’s performed historically?

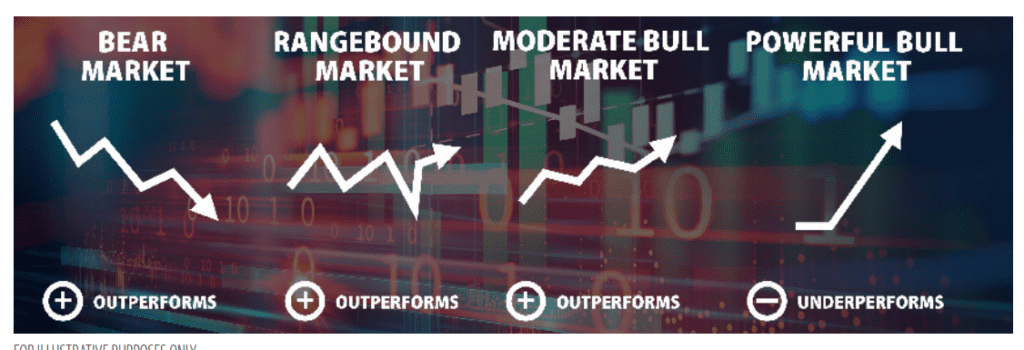

In historical contexts characterized by bear markets, range-bound markets, and moderate bull markets, a covered call strategy has typically demonstrated the ability to outperform its underlying securities. However, during robust bull markets, when the underlying securities experience frequent rises beyond their strike prices, covered call strategies have historically exhibited slower growth. Nevertheless, even in these bullish phases, investors typically realize moderate capital appreciation alongside the accrual of dividends and call premiums.

How writing a call option works?

Options make it possible to hedge a possible decline in a security and thus limit its loss through a gain on the option. To apply this hedging strategy, you have to take a short position on a call option, in other words sell a call.

The sale of calls achieves two objectives:

· Set the sale price of these securities (exercise price) and therefore set an acceptable loss.

· Collect a premium, i.e. additional income, or limit losses if the strike price is reached.

The option seller will be obligated to deliver the securities if exercised at the price fixed in advance. In this case the market will have evolved contrary to these expectations, it will have appreciated. The option investor will sell his securities for less than the market price.

Covered call options protect against downside risk. This being said, the covered call strategy provides limited downside protection. Also, when you write a covered call, you give up some of the stock’s potential gains. Covered call ETFs will tend to have a higher yield and a lower performance.

Popular Covered Call ETFs in Canada

ETF

Focus / Objective

Sectors / Geography

Investor Appeal

ZWB – BMO Covered Call Canadian Banks

Canadian banks + call premiums

100% Canadian Big 6 banks

Stable, income-focused play on Canadian banks

ZWC – BMO Canadian High Dividend CC

Broad Canadian high dividend portfolio

Financials & Energy = ~53%

Conservative, tax-efficient, steady monthly income

ZWP – BMO Europe High Dividend CC

European dividend payers + options

Switzerland, Germany, UK, France

Diversifies income outside North America

ZWH – BMO U.S. High Dividend CC

U.S. large-cap dividend names

Broad U.S. exposure, ~23% Tech

U.S. exposure with yield + lower volatility

ZWK – BMO Covered Call U.S. Banks

U.S. banking sector

100% U.S. banks (~38 names)

Higher yield (~6%), targeted U.S. financials

HTA – Harvest Tech Achievers

Global tech leaders + covered calls

Heavy in semis + software

Tech growth exposure with reduced volatility

HBF – Harvest Brand Leaders

20 global “top brands”

~20% Financials, 20% Tech, 15% Comm. Services

Blue-chip global exposure, monthly distributions

ZWB – BMO Covered Call Canadian Banks

The ZWB aims to provide exposure to a portfolio of dividend-paying securities (Canadian Banks), while collecting premiums related to call options. The portfolio is chosen on the basis of the criteria below:

• dividend growth rate; • yield; • payout ratio and liquidity.

ZWB holdings

Name

Weight

BMO Equal Weight Banks ETF

27.2%

Bank of Montreal

12.9%

Canadian Imperial Bank of Commerce

12.7%

Royal Bank of Canada

12.1%

National Bank of Canada

11.9%

The Toronto-Dominion Bank

11.9%

Bank of Nova Scotia

11.4%

Please visit issuers’ website for up-to-date figures – Best Covered Call ETF Canada

ZWC –BMO CDN High Div Covered Call

The BMO Canadian High Dividend Covered Call ETF (ZWC) has been designed to provide exposure to a dividend focused portfolio, while earning call option premiums. The underlying portfolio is yield-weighted and broadly diversified across sectors.

The fund selection methodology uses 4 factors: – Liquidity; – Dividend growth rate; – Yield and payout ratio.

ZWC is an excellent option for conservative investors looking for a steady income and low volatility. It’s tax-efficient because the dividends are all coming from Canadian companies. The financial sector and Energy represents 53% of the total overall sector allocation.

ZWC ETF Holdings

Company Name

Allocation

Canadian National Railway Co

5.4%

BCE Inc

5.2%

TELUS Corp

5.1%

Enbridge Inc

5.0%

Royal Bank of Canada

5.0%

Canadian Imperial Bank of Commerce

4.9%

Bank of Nova Scotia

4.7%

The Toronto-Dominion Bank

4.6%

Manulife Financial Corp

4.3%

Please visit issuers’ website for up-to-date figures – Best Covered Call ETF Canada

ZWP – BMO Europe High Dividend Covered Call ETF

The BMO Europe High Dividend Covered Call ETF (ZWP) has been designed to provide exposure to a dividend focused portfolio. These dividend paying companies are selected based on:

dividend growth rate,

yield,

payout ratio and liquidity.

ZWP Dividend ETF Holdings

Company Name

Allocation

Roche Holding AG

4.0%

Nestle SA

4.0%

Novartis AG

4.0%

GlaxoSmithKline PLC

4.0%

Sanofi SA

3.8%

TotalEnergies SE

3.7%

Unilever PLC

3.7%

Enel SpA

3.7%

Please visit issuers’ website for up-to-date figures – Best Covered Call ETF Canada

Geographic allocation

Countries

Weight

Switzerland

23.66%

Germany

24.24%

United Kingdom

18.76%

France

16.72%

Other (multiple countries)

16.62%

Please visit issuers’ website for up-to-date figures

Sector allocation

Type

Fund

Information Technology

6.22

Industrials

12.18

Consumer Discretionary

11.56

Consumer Staples

11.78

Health Care

16.56

Financials

14.79

Materials

9.48

Communication

8.10

Energy

3.89

Utilities

3.66

Please visit issuers’ website for up-to-date figures – Best Covered Call ETF Canada

ZWH – BMO US High Dividend Covered Call ETF

ZWH has been designed to provide exposure to a dividend focused portfolio, while earning call option premiums. The underlying portfolio is yield-weighted and broadly diversified across sectors. The Fund utilizes a rules-based methodology that considers the following criteria:

dividend growth rate,

yield,

payout ratio,

liquidity.

ZWH Dividend ETF Holding

Company Name

Allocation

Apple Inc

4.2%

Microsoft Corp

4.2%

Coca-Cola Co

4.1%

AbbVie Inc

4.1%

The Home Depot Inc

4.1%

Procter & Gamble Co

4.1%

Pfizer Inc

4.0%

Please visit issuers’ website for up-to-date figures

Geographic allocation

Country

Fund

USA

100.0%

Please visit issuers’ website for up-to-date figures

Please consult issuers’ website for up-to-date figures

ZWK -BMO Covered Call US Banks

The BMO Covered Call U.S. Banks ETF (ZWK) is professionally managed by BMO Global Asset Management. The fund has been designed to provide exposure to a portfolio of U.S. banks while earning call option premiums.

The fund invests in 38 US Banks. It’s ideal for investors looking for dividend income. The dividend yield on November 24th was 6.19%!

The fact that the fund uses call options accomplishes two things:

increases the dividend yield;

reduces volatility but also growth potential. So, it’s something to keep in mind.

HTA is an ETF that invests in an equally weighted portfolio of 20 large-cap technology companies (globally). In order to generate an enhanced monthly distribution yield, an active covered call strategy is engaged.

Covered call strategies are great as they generate additional income for investors (in the form of premiums). The strategy is somewhat conservative and aims at preserving the capital invested primarily. On the other hand, the strategy limits potential growth.

Name

Weight

Sector

NVIDIA Corporation

6.9%

Semiconductors

Advanced Micro Devices, Inc.

6.5%

Semiconductors

QUALCOMM Inc

6.5%

Semiconductors

Intuit Inc.

5.5%

Software

Apple Inc.

5.3%

Technology Hardware

Applied Materials

5.2%

Semiconductors

Keysight Technologies

5.2%

Electronic Equipment

Broadcom Inc.

5.1%

Semiconductors

Microsoft Corp

5.1%

Software

Adobe Inc.

5.0%

Software

HBF – Harvest Brand Leaders Plus Income

HBF is an equally weighted portfolio of 20 large companies selected from the world’s Top 100 Brands. The ETF is designed to provide a consistent monthly income stream with an opportunity for growth. In order to generate an enhanced monthly distribution yield, an active covered call strategy is engaged.

HDIF is a relatively new fund from Harvest ETFs (created on Feb 2022). It’s a covered call ETF and its main target audience are income/dividend investors.

HDIF is a fund of funds. It means this ETF invests in other ETFs to provide investors with diversification across various sectors of the economy ( Healthcare, Global Brands, Technology, Utilities, and US Banks). The primary objective is to provide a higher yield than traditional dividend ETFs by using a covered call strategy.

Additional facts about HDIF:

– The portfolio is reconstituted and rebalanced quarterly (minimum);

– The covered call strategy is applied on up to 33% of each equity securities held in underlying portfolios.

Sector allocation

Sector

% Allocations

Financial Services

31.8%

Healthcare

21.8%

Technology

23.4%

Comm. Services

15.0%

Utilities

13.7%

HDIF ETF review: Portfolio

ETF

Allocation

HUTL Harvest Equal Weight Glbl Utilts Inc

20.5

HHL Harvest Healthcare Leaders Inc

20.3

HBF Harvest Brand Leaders Plus Inc

20.7

HUBL Harvest US Bank Leaders Income Cl A

20.7

HTA Harvest Tech Achievers Gr&Inc

20.7

HLIF Harvest Canadian Equity Income Leaders ETF

23.3

Cash and other Liabilities

(26.2)

Please visit issuers’ website for most up-to-date data

HDIV -Hamilton Enhanced Multi-Sector Covered Call

HDIV is a passive covered call ETF. It’s ideal for investors who seek high dividend income and low volatility. HDIV invests in a basket of 7 covered call & sector focus ETFs. The fund manager uses also cash leverage of 25% to enhance yield and growth potential. The index tracked is The Solactive Multi-Sector Covered Call ETFs Index TR x 1.25.

The ETFs held within HDIV invest primarly in large corporations. In addition to using the covered call strategy, the funds ensure diversification of your investments across various sectors. See below the list of the 7 ETFs that make up HDIV:

All the funds that make up HDIV are covered call ETFs offered by various issuers such as: Harverst, BMO, CI Financial and Horizons.

Video HDIV overview

HMAX – Hamilton Canadian Financials Yield Maximizer

HMAX ETF is a new fund offered by Hamilton ETF. The fund invests in the Canadian banking sector. This fund aims to provide an attractive dividend yield (target 13%) using a covered call strategy. The strategy consists of writing call options on (50% of the portfolio) to collect premiums and maximize monthly distributions.

Objective: Designed to provide attractive monthly income by investing in a diversified portfolio of U.S. equity covered call ETFs and applying modest leverage (25%) to enhance yield and growth potential.

Strategy:

Invests primarily in U.S.-focused covered call ETFs across different sectors (technology, healthcare, financials, etc.).

Uses covered call writing to generate option premiums.

Adds 25% cash leverage to boost distributions.

Investor Appeal: Suitable for Canadian investors seeking high monthly distributions from U.S. equities, while accepting capped upside and slightly higher risk due to leverage.

Q&A

Do covered call ETFs pay dividends?

Yes, Covered call ETF’s offer an excellent dividend yield. Their dividend yield is usually superior to ‘regular’ dividend ETF’s. Thanks to premiums collected issuing covered calls, the manager boost the fund distributions (Dividends plus Premiums), thus the dividend yield is usually high.

Some Covered Call ETFs use leverage to enhance returns even higher.

Do covered calls beat the market?

During market corrections, the answer would be probably yes. In essence, the covered call strategy is a convervative strategy that tends to forego profits for stability and income.

In a bull markets, covered call ETFs would have a lousy performance. A ‘regular’ dividend ETF would definitely perform better in bull market that a Covered call ETF.

If you are retired or close to retiring, a covered call ETF could be a better option for you. For young investors building wealth, covered call ETFs are not a good choice because they deprive their holders of growth perspective.

How risky is covered calls?

Covered call ETFs are generally low to medium risk funds. However, if the fund manager uses leverage, the fund would be considered medium to high risk.

The Hamilton Enhanced U.S. Covered Call ETF (HYLD) is attracting a lot of investors in Canada, particularly for its high monthly return. But behind the impressive casts is a question that many are asking:

👉 Does HYLD really pay dividends… or is it mainly a return of capital (ROC)?

In this comprehensive analysis, based on your Q&A, we clarify how distributions actually work, the difference between price and total return, and why ROC is not a danger sign — contrary to what many believe.

🟨 1. HYLD: A high-income ETF

HYLD is designed to offer a monthly cash flow through a combination of:

🎯 Target: ~12% return per yearHYLD explicitly targets high income, not unit price growth.

🟦 2. Price performance: an incomplete indicator

Many investors judge HYLD based solely on price. For example, over 5 years, the graph shows a relatively stable or even slightly declining performance.

But here’s the problem:

👉 The price does NOT reflect the actual performance of an income-oriented ETF.

This is because HYLD redistributes a large portion of the earnings in the form of monthly distributions, resulting that:

The net asset value rises less

But the total cash flow generated is very high

Looking only at the price is therefore ignoring 80–90% of the real return.

🟧 3. Total Return = Price + Dividends

To understand HYLD, you have to think in terms of total return.

📌 Formula:

Price Performance + Dividends = Total Return

The table shown in the video shows higher total return returns:

1 year: +25.9%

3-year annualized: +23%

Since 2022: +11.5%/year

YTD: +21.9%

➡️ Very solid figures, despite a price that is not exploding.

🟩 4. Distribution history: what the numbers tell us

By analyzing the distribution history, we notice:

Stable monthly payments

sometimes a drop in distribution during difficult market periods

the introduction of ROC as a major component in some years

A clear example: 📉 In 2022, the bear market forced HYLD to reduce its distributions (visible in April).

This shows that distributions are not guaranteed. They depend on option premiums and the health of the US market.

🟥 Article 5. Return of Capital (ROC): danger or simple tax classification?

Among the elements that most resonate with investors: 👉 Why does HYLD distribute so much ROC?

Here is the essential clarification:

ROC does NOT mean that the fund gives you back your own money.

This is NOT a sign that the fund is in trouble.

This is often the consequence of hedged options strategies.

When the gains generated by the options offset the decline in the underlying assets, there may be no taxable net gain. As a result, the distribution is classified as an ROC.

🟩 Significant tax effect:

ROC reduces the adjusted cost base (ACB), which can defer tax later.

So that’s not a bad thing — it’s an accounting reality linked to the fund’s strategy.

🟫 6. Simple example: GOOGL to understand the ROC

In the video, a clear example with GOOGL illustrates the phenomenon:

The manager sells covered options.

It generates bonuses every month.

But if the stock falls during the year… → the options offset the loss→ there is no taxable gain

Distributions cannot be reported as dividends or capital gains

They therefore become Return of Capital

🎯 ROC = a tax adjustment, not a hidden risk.

🟦 7. Why HYLD Needs to Be Evaluated Differently

HYLD is not a growth ETF. It should not be evaluated as VFV or VOO.

Here’s what really matters:

stable distributions

Ability to generate bonuses

Total Yield

Adequacy with the income profile

The main conclusion:

👉 HYLD actually generates income through options. The ROC simply reflects how these revenues are classified.

HYLD is not a growth ETF and therefore should not be evaluated as VFV or VOO. Its main objective is to provide a high income, which involves using different criteria to measure its performance. What really matters is the stability of distributions, the fund’s ability to generate premiums, total return and its suitability for an income-oriented profile. In practice, HYLD does generate income through its hedged options strategies. The ROC is only a tax classification of these distributions, and not a sign of fragility.

🟨 8. Key points to remember

HYLD is designed for high income, not growth.

The ROC is not a sign of danger, but a fiscal reality.

Distributions vary by market.

The total return is much higher than the price suggests.

HYLD is suitable for income-oriented investors, not extreme growth hunters.

Hedged options limit upside potential, but stabilize revenues.

HYLD is primarily an ETF designed to generate high income, not to offer strong capital growth. This orientation explains why its price may seem stable or not very dynamic, while its total return, including monthly distributions, is actually much higher than what an investor who only sees the price chart. A point that is often misunderstood concerns the Return of Capital (ROC): far from being a sign of weakness, it reflects above all a tax reality resulting from the hedged option strategies used by the fund. Distributions can also vary over the course of the market, as they depend on the premiums generated and broader economic conditions. HYLD is therefore primarily suitable for investors focused on income and cash flow stability, rather than those looking for aggressive growth comparable to a traditional index ETF. Finally, it should be understood that the hedged options used in the fund’s strategy naturally limit the potential for appreciation in times of strong bullish rally, but they also help to stabilise income, making HYLD an attractive tool for a sustainable income strategy.

🟩 Conclusion

In conclusion, HYLD is a powerful ETF for investors looking for:

high monthly income

A simple solution to generate cash flow

A diversified and option-optimised strategy

An attractive total return despite a stable price

Return on Capital is an integral part of the operation of this type of fund and should be understood as a tax concept, not as an alarm.

➡️ HYLD can be a great component of an income portfolio, as long as you understand how it generates its distributions and what trade-offs this strategy entails.

Executive summary

JEPI and JEPQ are two leading income-focused ETFs using covered call strategies, but they serve different investors. JEPI offers stable income with broad diversification and lower volatility, while JEPQ provides higher yield driven by tech exposure. Understanding their objectives, risks, and market behavior helps identify which ETF fits your strategy best.

JEPI

Investment objective

The JPMorgan Equity Premium Income ETF (JEPI) is an income focused covered call ETF. It’s ideal for conservative investors who are seeking income and moderate growth. The manager of JEPI invests in a portfolio of stocks that combine 3 characteristics:

Part of the S&P 500, so in other word large cap stocks only;

Low volatility stocks, meaning, stocks that fluctuate far less than the market. This is generally the case of defensive stocks operating in stable industries. The main metric used by the fund manager of JEPI to assess volatility is the Beta. Beta is a coefficient risk, for instance a Beta of 0.5 would indicate that the stock exhibits 50% of the volatility of the stock market;

Value stocks: the analysts’ team of JEPI will conduct a fundamental bottom up approach to select only stocks that are considered undervalued.

Advantages

JEPI, an ETF focused on issuing call options, offers several advantages that might appeal to certain investors. Firstly, it boasts an attractive yield derived from the money earned through call option writing. Moreover, JEPI exhibits lower volatility compared to investing directly in an S&P 500 index ETF like SPY, making it a suitable option for conservative investors and income seekers.

Another positive aspect of JEPI is its ability to capitalize on high volatility, which often translates to increased premiums for the fund. Additionally, investors can save valuable time and effort by avoiding the need to personally write call options on the S&P 500, as JEPI handles this strategy on their behalf. Furthermore, with relatively low fees of 0.35% total expense ratio, JEPI presents a cost-effective investment choice. The ETF’s diversification across various sectors adds another layer of appeal, spreading risk across different industries.

However, JEPI does have some drawbacks that potential investors should consider. In bull markets, it is expected to underperform the S&P 500 index due to the call option writing strategy, which reduces volatility but also limits its performance during bullish periods.

Recap

Positives

Attractive yield thanks to money earned issuing call options;

Lower volatility than investing in a S&P500 index ETF such as SPY;