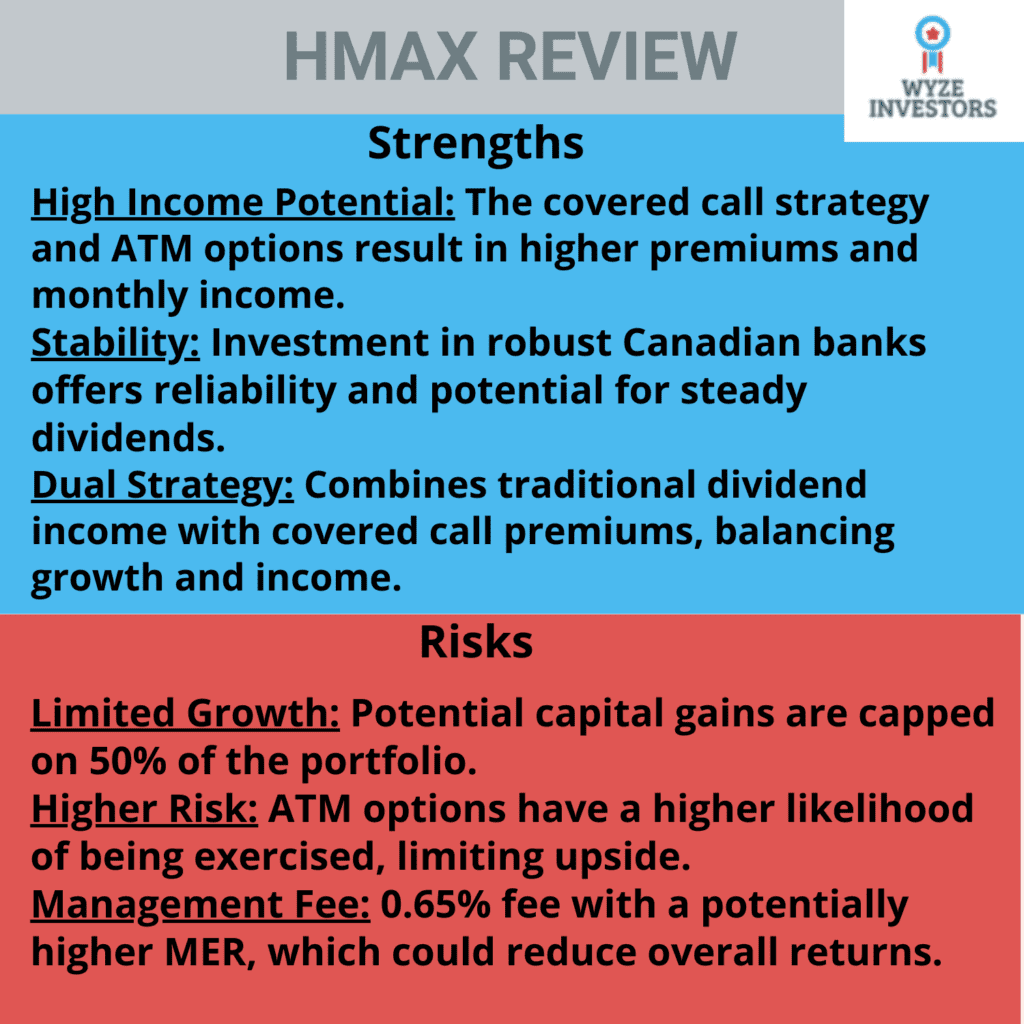

HMAX ETF Review (2026)

Hamilton Canadian Financials Yield Maximizer — Complete Analysis

| Target Yield ~12–14% | Management Fee 0.65% | Options Strategy 50% ATM | Distribution Monthly |

| ⚡ Bottom Line Up Front HMAX is one of Canada’s highest-yielding covered call ETFs, targeting 13–15% annual income through a unique at-the-money (ATM) options strategy on Canadian financial stocks. It is best suited for income-focused investors who can accept capped upside and moderate volatility — not for growth investors. |

What Is HMAX ETF?

HMAX — the Hamilton Canadian Financials Yield Maximizer ETF — is an actively managed covered call ETF listed on the Toronto Stock Exchange under the ticker HMAX.TO. Launched by Hamilton ETFs, it targets high monthly income by writing covered call options on approximately 50% of its portfolio of Canadian financial stocks, primarily the Big Six banks plus insurance and asset management companies.

What sets HMAX apart from most comparable Canadian ETFs is its use of at-the-money (ATM) options rather than the more common out-of-the-money (OTM) approach. This generates significantly higher option premiums — and therefore higher income — but with a tradeoff: a greater chance that shares get called away, limiting capital appreciation.

| 📌 Key Insight ATM options generate 2x to 3x more premium income than OTM options on the same underlying stock. This is why HMAX targets 13–15% yield while comparable ETFs like ZWB target only 6–7%. |

Executive summary

Videos

How HMAX Generates Its High Yield

HMAX’s income comes from two combined sources:

- Dividends from Canadian bank and financial stocks (approximately 4–5% annually from the underlying holdings)

- Option premiums from writing covered calls on 50% of the portfolio (generating the bulk of the remaining yield)

ATM vs OTM — Why It Matters

Most covered call ETFs in Canada write out-of-the-money (OTM) options — where the strike price is above the current stock price. This preserves more upside potential but generates lower premiums. HMAX instead writes at-the-money (ATM) options, where the strike equals or nearly equals the current price.

| Option Type | Premium Size | Assignment Risk | Upside Capture |

| ITM (In the Money) | Highest | Very High | Very Low |

| ATM (At the Money) ← HMAX | High | Medium-High | Low |

| OTM (Out of the Money) ← ZWB | Low-Medium | Low | Moderate |

What Does HMAX Hold?

HMAX holds a concentrated portfolio of Canadian financial services companies, weighted toward the Big Six banks. The fund provides modest diversification beyond pure bank exposure by including insurance and asset management companies.

| Ticker | Company | Weight |

| RY | Royal Bank of Canada | 22.7% |

| TD | Toronto-Dominion Bank | 17.2% |

| BMO | Bank of Montreal | 11.3% |

| BN | Brookfield Corporation | 11.1% |

| BNS | Bank of Nova Scotia | 10.1% |

| CM | CIBC | 7.6% |

| MFC | Manulife Financial | 7.1% |

| SLF | Sun Life Financial | 5.1% |

| GWO | Great-West Lifeco | 4.8% |

| IFC | Intact Financial | 4.7% |

| Sector | Allocation |

| Banks | 70.0% |

| Insurance | 20.8% |

| Asset Management | 10.6% |

HMAX Yield and Fees

Distribution Yield

HMAX targets an annual distribution yield of approximately 13%, paid monthly. Based on recent dividend history, the fund has consistently met or exceeded this target, with current yields running closer to 15% annually.

Management Fees

HMAX has a stated management fee of 0.65%. However, the full Management Expense Ratio (MER) — which includes trading costs and other fund expenses is 0.80%.

HMAX Total Return Performance

Total return includes both distributions received and changes in NAV. Here is HMAX’s recent performance:

Source: Yahoo Finance — monthly total returns. Past performance does not guarantee future results.

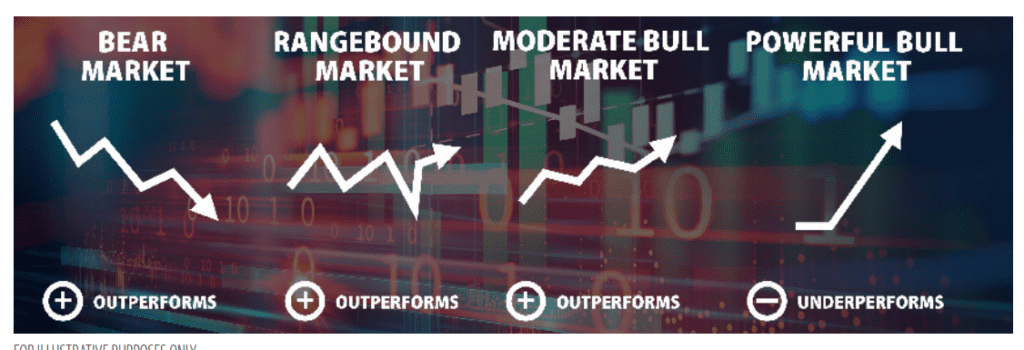

| 📊 When Covered Calls Outperform vs Underperform Covered call strategies like HMAX historically outperform in bear markets, sideways markets, and mild bull markets. They tend to underperform in strong bull runs where underlying stocks frequently exceed strike prices. For the Canadian banking sector — which tends toward moderate, steady growth — this strategy has historically been well-suited. |

HMAX vs ZWB — Which Canadian Bank ETF Is Better?

The most common comparison for HMAX is ZWB — the BMO Covered Call Canadian Banks ETF. Both target income from Canadian bank stocks using covered calls, but they differ significantly in strategy and yield.

| HMAX | ZWB | |

| Options Strategy | ATM (At the Money) | OTM (Out of the Money) |

| % Portfolio Covered | 50% | 50% |

| Target Yield | 13–15% | 6–7% |

| MER | ~1%+ (est.) | 0.72% |

| Holdings | Banks + Insurance + Asset Mgmt | Big Six Banks only |

| Upside Potential | Limited (ATM caps gains) | Moderate (OTM allows some gains) |

| Best For | Income maximizers | Income + moderate growth |

If your primary objective is maximum monthly income and you are comfortable with capped growth, HMAX is the stronger choice. If you want income with some capital appreciation potential, ZWB’s OTM strategy preserves more upside while still delivering a solid 6–7% yield.

HMAX vs HYLD — Canadian vs U.S. Exposure

Both HMAX and HYLD are Hamilton ETF products using similar covered call mechanics, but they target different geographies:

- HMAX focuses on Canadian financial stocks (banks, insurance, asset management) — approximately 75% banks

- HYLD focuses on U.S. equity markets with a sector mix broadly similar to the S&P 500, structured as a portfolio of Canadian covered call ETFs

Investors who want Canadian financial sector exposure with high income should choose HMAX. Those seeking broader U.S. market income with similar distribution mechanics should consider HYLD.

HMAX vs HCAL — Income vs Growth

HCAL (Hamilton Enhanced Canadian Bank ETF) and HMAX are often compared because both hold Canadian financial stocks, but their objectives differ fundamentally:

| HMAX | HCAL | |

| Primary Objective | High monthly income | Growth + income |

| Strategy | Covered calls (ATM, 50%) | 25% leverage, mean reversion |

| Yield | 13–15% | Lower, but growing |

| Growth Potential | Limited (options cap gains) | Higher (leverage amplifies gains) |

| Risk Profile | Income risk, moderate volatility | Leverage risk, higher volatility |

| Best For | Retirees, income seekers | Younger investors, growth focus |

For younger investors with a long time horizon, HCAL’s growth-oriented approach is generally more appropriate. For investors in or near retirement seeking reliable monthly cash flow, HMAX’s consistent high distributions make it worth considering.

Who Should Invest in HMAX?

| ✅ HMAX is a good fit if you: • Need consistent monthly income from your portfolio • Are comfortable with capped upside on the covered portion • Hold it in a TFSA or RRSP for tax efficiency • Have a long-term buy-and-hold mindset on Canadian financials • Understand and accept the mechanics of ATM covered calls |

| ❌ HMAX is NOT a good fit if you: • Are investing primarily for long-term capital growth • Expect to fully participate in bank stock rallies • Are sensitive to NAV erosion in down markets • Want the lowest possible MER • Are looking for broad market diversification beyond financials |

HMAX in a TFSA or RRSP

Because HMAX generates high monthly distributions, tax efficiency matters. Here’s how it fits in common Canadian registered accounts:

- TFSA — Distributions grow and can be withdrawn completely tax-free. Ideal for investors who want to use the income without triggering tax events.

- RRSP — Distributions are sheltered from tax until withdrawal. Good for investors who want to reinvest distributions and compound within the account.

- Non-registered account — Distributions are taxed as income in the year received. The high yield makes the tax drag significant — registered accounts are strongly preferred.

Frequently Asked Questions

Is HMAX a good investment?

HMAX is a solid choice for income-focused investors who understand and accept the tradeoffs of an ATM covered call strategy. It is not suitable for growth investors. The fund’s consistency in meeting its 13%+ target yield and its 24% one-year total return demonstrate that it can deliver strong results — but always evaluate against your personal risk tolerance and investment goals.

How often does HMAX pay dividends?

HMAX pays distributions monthly, typically at the end of each month. The amount varies slightly based on option premiums collected and underlying dividend income.

Does HMAX hold physical bank shares?

Yes. HMAX holds actual shares of Canadian financial companies. The covered call strategy is written on top of these holdings — approximately 50% of the portfolio is subject to covered calls at any given time. The remaining 50% is fully exposed to the underlying stock performance.

What happens if Canadian banks drop significantly?

If the underlying stocks fall, HMAX’s NAV will decline. The option premiums collected provide a partial buffer against losses, but they do not fully protect against a sharp market downturn. This is an important risk to understand — HMAX does not provide downside protection, only income enhancement.

Disclaimer

This article is for educational purposes only and does not constitute financial advice. ETF yields, fees, and holdings are subject to change. Always verify current data with the fund provider before making investment decisions. Past performance does not guarantee future results.

© 2026 WyzeInvestors.com

Is there fees from Hamilton ETF when share of that EFT are sold. The prospectus indicate when sahre are sale at a value 95% of share value. Does that means Hamilton take 5% of the shares are sold?

Hi Francis, The management fee is 0.65%. from their website:

You don’t pay these expenses directly. They affect you because they reduce the ETF’s returns. The ETF’s expenses are made up of the management

fee, operating expenses and trading costs.

The ETF’s annual management fee is 0.65% of the ETF’s value

As this ETF is new, its operating expenses and trading costs are not yet available

Thanks for this good video. Can you please comment on erosion of capital over time with HMAX . It *appears that HMAX’s ATM option strategy might erode capital more than a “safer” OTM fund. I am ok with little or no capital gain when focused on a high income ETF, but the last thing I want is steady erosion of capital over time. Your thoughts on what the ATM option strategy does to put capital at risk is appreciated.

Hi,

Thanks for your comments. As a reminder, I am not a financial advisor or an expert; please research before investing.

First, only 50% of the portfolio uses the options strategy, so there is some potential growth in the remaining 50%. Only time will tell if the managers can generate some growth with the ATM strategy. It’s an active strategy, so the manager’s experience and abilities will be essential.

All of these ETFs are legal scams, Hyld is a classic one, declining NAV and high pay out which is all destructive return of capital. If you’re using the money for other things such as expenses and don’t reinvest distributions these are basically just legalized Ponzi schemes.

Hi,

Thanks for your comment Paul. I would not go as far as calling these types of funds a scam! They fit long-term income-oriented conservative investors who don’t mind the dividend taxation impact.

I believe what’s happening is these types of funds are attracting high dividend yield chasers who don’t realize that they are losing on the growth component of their investment.

The underlying stocks are some of the most stable investments in the history of the stock market, the monthly income is a mix of dividend and capital gains. I could care less what the NAV is as long as I get my income. The dividends payments to the ETF will increase over time as well. I would say that the strategy of investing in stocks with little or no return in the hope that they will be worth much more than when you purchased them is not a great strategy for many of us over age 60. If you invested in RY 50 years ago and earn huge dividends today would you care what the stock price is? Getting regular monthly income is better for many investors sense of security and well being. To say these are scams a nonsense comment.

I echo your sentiments David however my concern is how sustainable is the dividend payout of $.18 a share gonna be for the next 10 years

Since I hold many of the stocks individually as found in my covered call ETF’s I get the best of both! The dividend AND the upside of advancement. What’s not to like?

Hello Stanley,

You’re absolutely right! Holding individual stocks alongside covered call ETFs truly lets you enjoy both worlds: consistent dividends from the covered call strategy and the potential upside from the individual stocks themselves. This approach can be a smart way to balance income generation with growth potential.