A yield north of 70% will stop any income investor mid-scroll. That is the number currently attached to MSTE, the Harvest Strategy Inc. Enhanced High Income Shares ETF, and it is not a typo, a marketing exaggeration, or a short-term anomaly. It is a real, published figure, calculated the way current-yield figures are always calculated: by annualizing the most recent monthly distribution and dividing it by the fund’s market price.

That single sentence contains almost everything you need to understand about MSTE — and almost everything that gets misunderstood about it. A 70% current yield is not a forecast of your annual return. It is not “free income” generated by owning MicroStrategy stock. It is the output of a specific, mechanical options strategy applied to one of the most volatile large-cap stocks trading on any North American exchange, and it comes bundled with risks that are just as extreme as the yield itself.

This article is not a recommendation to buy or avoid MSTE. It is an attempt to explain, in plain language, exactly what this ETF does, why it can pay distributions this large, why “high yield” and “high total return” are two entirely different things, and how an investor should think about whether — and how much — of a fund like this belongs in a portfolio.

Video

What Is MSTE ETF?

MSTE is the TSX ticker for the Harvest Strategy Inc. Enhanced High Income Shares ETF, managed by Harvest Portfolios Group Inc., a Toronto-area investment fund manager. The fund was previously named Harvest MicroStrategy Enhanced High Income Shares ETF and was renamed in February 2026 to reflect the renaming of its underlying company from MicroStrategy Incorporated to Strategy Incorporated — the business itself did not change, only its corporate name.

Here are the fund’s key characteristics as of its most recent published fact sheet (data as at June 30, 2026):

| Feature | Detail |

|---|---|

| TSX Ticker | MSTE |

| Inception Date | March 5, 2025 |

| Distribution Frequency | Monthly |

| Distribution Method | Cash or DRIP |

| Management Fee | 0.40% |

| Max Covered Call Write Level | 50% of the portfolio |

| Leverage | Modest, targeted around 25% (up to 33% per the fund’s prospectus) |

| Risk Rating | High |

| Registered Account Eligibility | RRSP, RRIF, RESP, TFSA, FHSA |

| Underlying Holding | Common stock, Class A, of Strategy Incorporated (NASDAQ: MSTR) |

MSTE’s investment objective, as defined in its prospectus, is twofold: to provide unitholders with long-term capital appreciation by investing, directly or indirectly and on a levered basis, in the Class A common stock of Strategy Incorporated, and to generate high monthly cash distributions through an active covered call writing program.

What makes MSTE structurally distinct from a typical dividend or covered call ETF is that it concentrates up to 100% of its assets in a single company — Strategy Incorporated — and then layers modest leverage and an aggressive options overlay on top of that concentrated position. This is not a diversified equity fund with an income sleeve. It is a single-stock alternative ETF, and understanding that distinction is the single most important thing an investor can take away from this section.

How Does the Strategy Actually Work?

To understand MSTE, you first need to understand what it owns, and then understand what the fund manager does with that ownership.

What MSTE owns. At its core, MSTE holds — directly or through derivative exposure — shares of Strategy Incorporated, the company formerly known as MicroStrategy. Strategy is technically classified as an enterprise analytics and business intelligence software company, but in practice, the market treats it primarily as a leveraged proxy for Bitcoin, because the company has accumulated an enormous corporate Bitcoin treasury and its share price has become tightly correlated with the price of Bitcoin — often amplified in both directions.

MSTE adds a layer of leverage on top of this already-volatile stock, targeting roughly 25% additional exposure. In practical terms, if you put $100 into MSTE, the fund may be managing closer to $125 of effective exposure to MSTR shares, using borrowed capital through its prime brokers.

How covered calls generate income

Once the fund holds its MSTR position, the manager writes (“sells”) call options against up to 50% of that position every month. Here is the plain-language mechanics of a covered call, for anyone who has never traded an option:

Imagine you own 100 shares of a stock trading at $50. You sell someone else the right — but not the obligation — to buy those 100 shares from you at, say, $52, any time before a set date a few weeks away. In exchange for granting that right, the buyer pays you cash upfront. That cash is the “option premium,” and you get to keep it no matter what happens next.

If the stock stays below $52, the option expires worthless, the buyer walks away, and you keep both your shares and the premium. If the stock rises above $52, the buyer will likely exercise their right, and you are obligated to sell your shares at $52 — missing out on any gain above that price, but still keeping the original premium you collected.

Why the yield is so high. Option premiums are priced largely based on the volatility of the underlying stock. The Black-Scholes model and its variants — the standard frameworks used to price options — treat volatility as one of the single biggest drivers of premium size. A stable blue-chip utility stock generates tiny option premiums because there’s little uncertainty about where the price will be in a month. MSTR is about as far from that description as a stock can get: it can move 10%, 20%, or more in a single week, driven by swings in Bitcoin’s price, corporate financing announcements, and broad crypto sentiment.

Impact of volatility

That volatility is exactly what makes MSTE’s premiums so large. The fund’s own literature is explicit that higher volatility in the underlying stock results in higher option premiums — and it’s writing those options on a stock that is one of the most volatile large-cap names on any North American exchange, then adding leverage to the underlying position before doing so.

Why the income is not “free money.” This is where investors most often get confused, and it deserves the clearest possible explanation. There are two separate costs baked into every dollar of MSTE’s distribution:

First, every call option written caps the fund’s upside. If MSTR stock rallies sharply, MSTE does not fully participate — the shares subject to written calls are effectively sold at the strike price, and the fund forgoes the gain above that level. Investors are trading upside potential for current income, dollar for dollar.

Second, and more importantly for MSTE specifically, distributions in a fund like this are frequently paid out of a mix of option premium, and — when premiums and any dividend income aren’t sufficient to cover the target payout — a return of capital. A return of capital is not a form of investment “profit” the way a covered dividend is; it’s effectively a partial return of your own invested principal, paid back to you. Over time, if a fund’s total return (share price plus distributions) is negative while distributions continue to be paid, that is a strong signal that at least part of what you’re receiving is your own capital being handed back to you, not new income being generated.

Why Is MSTE Different From the Alternatives?

Versus owning MSTR directly. If you buy MSTR shares outright, you get full exposure to any price appreciation, no leverage unless you apply it yourself, no monthly income, and no cap on your upside. MSTE trades some of that upside away in exchange for monthly cash flow and adds leverage you did not necessarily ask for.

Versus a Bitcoin ETF. A spot or futures-based Bitcoin ETF gives you more direct crypto exposure without the operational and equity-specific risks tied to a single company (executive decisions, corporate debt structure, dilution, insider actions). MSTE’s Bitcoin exposure is entirely indirect, filtered through MSTR’s corporate structure and financing decisions, and further modified by leverage and options overlays.

Versus a traditional dividend ETF. A traditional Canadian dividend ETF holding 20-plus established companies generates income from real, recurring corporate earnings distributed as dividends. Its yield is typically in the 3–6% range, reflects genuine profit-sharing, and comes with far lower concentration risk. MSTE’s yield is an order of magnitude larger because its income source and its risk profile are fundamentally different animals.

Versus other covered call ETFs. Many popular covered call ETFs (on the Nasdaq-100 or S&P 500, for example) write options against a diversified basket of dozens or hundreds of stocks. MSTE writes options against one single, highly volatile stock. Diversified covered call ETFs typically yield somewhere in the high single digits to mid-teens. A yield many multiples higher than that, from a single-stock covered call fund, is a direct reflection of concentrated, extreme volatility — not a “better” version of the same strategy.

Quick Comparison Table

| Feature | MSTE | Owning MSTR Directly | Diversified Covered Call ETF (e.g., broad index) |

|---|---|---|---|

| Underlying exposure | Single stock (MSTR), levered | Single stock, no leverage | Dozens/hundreds of stocks |

| Income source | Option premiums + possible return of capital | None (unless MSTR pays a dividend) | Option premiums |

| Upside participation | Capped, partial | Full | Capped, partial |

| Volatility | Very high | High | Moderate |

| Diversification | None | None | High |

| Leverage | Yes (~25–33%) | No (unless self-applied) | Typically none |

| Feature | MSTE | Spot Bitcoin ETF |

|---|---|---|

| Underlying exposure | Single stock (MSTR), levered | Bitcoin directly |

| Income source | Option premiums + possible return of capital | None |

| Upside participation | Capped, partial | Full |

| Volatility | Very high | High |

| Diversification | None | None |

| Leverage | Yes (~25–33%) | No |

Advantages of MSTE

Access at a lower entry price. MSTR has historically traded at a high per-share price. MSTE offers indirect exposure through a Canadian-dollar-denominated unit, often at a more accessible price point per unit.

High monthly cash flow. For investors specifically seeking monthly income rather than growth, the covered call overlay converts a portion of the underlying stock’s volatility into a recurring cash distribution rather than leaving all potential value locked in unrealized share price movement.

Tax treatment of option premiums. Under current CRA administrative policy, and as described in the fund’s prospectus, option premiums received from covered call writing in this structure are generally treated as capital gains rather than fully taxable income — which, for a taxable account, can mean a more favourable tax rate than ordinary income, though this depends entirely on individual circumstances and is not guaranteed to remain CRA’s treatment indefinitely.

Professional, active management. The manager actively decides monthly how much of the portfolio to write calls against (up to the 50% ceiling) and at what strike prices, adjusting to prevailing volatility and market conditions rather than following a fixed mechanical formula.

Canadian-dollar, TSX-listed convenience. For Canadian investors, MSTE trades in CAD on the TSX and is eligible for registered accounts including the TFSA, RRSP, RRIF, RESP, and FHSA — removing the need to hold U.S.-dollar positions or navigate a U.S. exchange directly.

Risks: What This Article Would Be Irresponsible to Skip

This is the section that matters most, and the fund’s own recent performance data makes the case better than any risk disclaimer could.

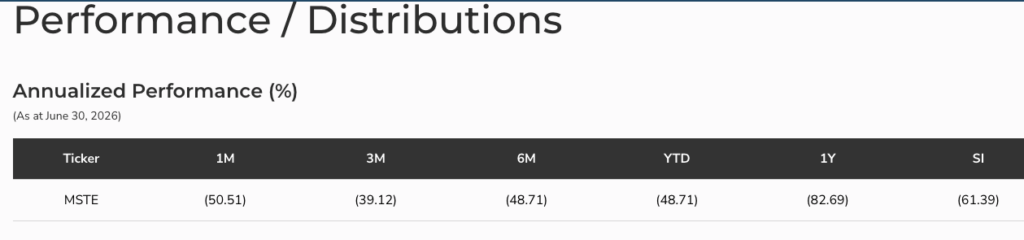

Performance since inception has been severe. As at June 30, 2026, MSTE’s own published fact sheet reported the following returns: down 50.51% over one month, down 39.12% over three months, down 48.71% over six months, down 48.71% year-to-date, down 82.69% over one year, and down 61.39% since inception. These are not hypothetical stress-test numbers — they are the fund’s actual, realized results. A fund that has lost more than four-fifths of its value over a trailing year, even while paying a headline yield above 70%, is the clearest possible illustration of why yield and total return are not the same thing.

Limited upside.

Every call option written against the portfolio caps how much the fund benefits from a rally in the underlying stock. In a strongly rising market for MSTR, MSTE will typically underperform simply holding MSTR shares directly.

Extreme volatility, amplified by leverage. MSTR is already one of the more volatile large-cap U.S. equities, given its function as a leveraged Bitcoin proxy. MSTE adds roughly 25–33% additional leverage on top of that position. Leverage magnifies both gains and losses — and in a falling market, it accelerates the pace of capital erosion.

Total dependence on one company and one asset.

Because MSTE concentrates up to 100% of assets in a single issuer, any company-specific event — a change in corporate strategy, a large debt issuance, an accounting concern, a change in leadership, or a forced sale of Bitcoin holdings — could disproportionately affect the fund in a way that a diversified holding never would.

Indirect dependence on Bitcoin. Because Strategy’s business is now inseparable from its Bitcoin treasury, MSTE’s fortunes are tied not just to a single company but, through that company, to the price of a single, highly volatile digital asset.

NAV erosion and distribution sustainability. When a fund’s distributions are not fully covered by option premiums and any dividend income, the difference is often paid out as a return of capital, which reduces the fund’s net asset value over time. Investors chasing the advertised yield without checking whether NAV is also shrinking can end up receiving what looks like “income” that is, in substance, their own money being returned to them — while the underlying investment shrinks. MSTE’s own performance figures, with steep losses across every time frame reported, suggest this dynamic has been very much in play.

Distributions are not fixed or guaranteed. The fund’s prospectus is explicit that distributions may fluctuate monthly, quarterly, or annually, and that there is no assurance any distribution will be paid in any given period. The current 70%+ “current yield” figure is an annualization of the most recent single monthly payment — not a promise of what the next twelve months will bring.

Concentration and liquidity risk. As an alternative mutual fund holding up to 100% of its assets in one issuer, MSTE also carries elevated liquidity risk relative to broadly diversified funds, since the fund’s ability to meet redemptions is tied to the trading liquidity of a single underlying stock.

Historical Performance: What the Numbers Actually Show

MSTE launched on March 5, 2025, giving it a relatively short track record. Since inception, the fund’s cumulative return has been negative 61.39% (as at June 30, 2026), while the fund has continued paying monthly distributions throughout — most recently $0.10 per unit, translating into that headline 70.59% annualized current yield.

Why can both of these things be true at once? Because current yield is a snapshot calculation based on the most recent distribution and the current, much-lower unit price — it says nothing about the trajectory that got the fund to that lower price in the first place. A shrinking NAV mechanically inflates the percentage yield even if the dollar distribution itself is falling, simply because the yield is being calculated against a smaller denominator.

The steep declines across every measured period — one month, three months, six months, year-to-date, one year, and since inception — line up closely with the well-documented volatility in MSTR and Bitcoin more broadly over the same window, compounded by MSTE’s leverage. This is precisely the volatility that generates MSTE’s large option premiums in the first place; it is the same volatility that has driven the fund’s NAV sharply lower. The income and the risk in this fund are not separate phenomena — they are two expressions of the same underlying force.

Who Should Consider MSTE?

Potentially suitable for:

- Experienced, tactical investors who already understand options mechanics and are using MSTE as a deliberate, small, satellite position rather than a core holding

- Investors who already hold direct MSTR or Bitcoin exposure and are comfortable with the asset class’s volatility

- Income-focused traders seeking short-term cash flow who actively monitor their position and are prepared to reassess frequently

- Investors who fully understand that the “yield” figure is not equivalent to expected total return

Likely unsuitable for:

- Beginner investors, or anyone new to ETFs, options, or leveraged products

- Conservative investors prioritizing capital preservation

- Long-term buy-and-hold investors seeking growth exposure to technology or crypto themes

- Retirees or near-retirees relying on the distribution as a stable, dependable income stream

- Anyone allocating based primarily on the advertised yield percentage without reviewing total return history

How Much Should You Allocate?

There is no universal answer here, and any article claiming otherwise should be treated with skepticism. What follows are illustrative starting points, not personalized advice, and any allocation decision should account for your own risk tolerance, time horizon, and full financial picture — ideally with input from a qualified advisor.

| Portfolio Type | Illustrative MSTE Allocation | Rationale |

|---|---|---|

| Conservative / capital preservation | 0% | Volatility and concentration risk are incompatible with the mandate |

| Balanced, diversified portfolio | 0–2% | If included at all, sized as a small speculative satellite, not a core income holding |

| Income-focused portfolio | Generally avoided or held at a minimal, tightly monitored weight | High current yield does not equate to reliable or sustainable income |

| Aggressive / tactical portfolio | Small, actively monitored position (commonly cited rules of thumb in the ETF-education space suggest single-digit percentages for any single speculative satellite holding) | Suited only for investors who can tolerate the fund’s demonstrated volatility and actively manage position sizing |

The underlying principle that should guide any allocation decision: MSTE should generally represent a small satellite position at most within a diversified portfolio, sized so that even a severe drawdown — of the magnitude the fund has already experienced since inception — would not meaningfully derail your broader financial plan.

Canadian Investors: Account Considerations

MSTE is eligible for the TFSA, RRSP, RRIF, RESP, and FHSA, per the fund’s fact sheet and prospectus. A few practical considerations for Canadian investors:

TFSA. Distributions and capital gains inside a TFSA are not taxed, which can be appealing given the fund’s high headline yield — but this also means any losses inside a TFSA cannot be claimed against other capital gains, an important consideration given the fund’s performance history.

RRSP/RRIF. Income compounds tax-deferred, which can help offset some of the tax drag on frequent monthly distributions, though eventual withdrawals are taxed as ordinary income.

Taxable (non-registered) account. As discussed above, option premiums received by the fund are generally treated under current CRA administrative policy as capital gains rather than fully taxable income when distributed, which may be more tax-efficient than ordinary dividend or interest income for some investors — though the composition of any given distribution (income, capital gains, or return of capital) can vary and will be reported to unitholders after year-end.

U.S. withholding tax. Because MSTE is a Canadian trust structured to hold U.S. equity exposure indirectly (rather than a U.S.-domiciled fund), Canadian investors do not face the same direct U.S. withholding tax treatment on distributions that they would face holding a U.S.-listed ETF; however, tax treatment always depends on account type and individual circumstances, and investors should confirm specifics with a tax professional.

Given the fund’s realized volatility, the account-type decision matters less than the position-sizing decision — but for investors proceeding regardless, understanding these distinctions is worthwhile.

Alternatives Worth Comparing

- MSTY (YieldMax MSTR Option Income Strategy ETF): A U.S.-listed fund pursuing a broadly similar single-stock options-income approach on MSTR, though through a different structure and issuer; useful as a direct comparison point for investors specifically drawn to MSTR-linked income products.

- QDTE / XDTE: U.S.-listed ETFs employing short-dated options income strategies on broader indices rather than a single stock, offering diversification MSTE does not provide.

- JEPI / JEPQ: Diversified, actively managed covered call ETFs on U.S. large-cap indices, generating more moderate (typically high single-digit to low-double-digit) yields with substantially lower single-issuer concentration risk.

- Direct Bitcoin ETFs: For investors whose actual objective is crypto exposure rather than income, a spot Bitcoin ETF removes the equity-specific and options-related layers of complexity entirely.

Each of these serves a different objective — some investors want diversified income, others want direct crypto exposure, and others specifically want the amplified, single-stock options-income profile MSTE provides. The right comparison depends entirely on which of those objectives you’re actually trying to solve for.

Frequently Asked Questions

Is MSTE safe?

No investment offering a yield this large should be described as “safe.” MSTE carries a High risk rating from its own manager, uses leverage, and has experienced steep losses since inception. It should be evaluated as a high-risk, speculative holding.

Why is the yield so high?

Because it is calculated from option premiums generated by writing calls against one of the most volatile large-cap stocks on the market, further amplified by leverage — not because the fund is generating extraordinary underlying business profit.

Can the distribution decrease?

Yes. The fund’s prospectus explicitly states distributions may fluctuate and are not guaranteed in any period. Distribution amounts have already varied, and given the fund’s NAV trajectory, sustainability of the current payment level is a legitimate open question.

Does MSTE outperform MicroStrategy (MSTR)?

Based on the return data disclosed by the fund itself, MSTE’s total return since inception has been sharply negative, and its capped-upside structure means it will typically lag a straightforward long position in MSTR during strong rallies, while distribution income only partially offsets downside during declines.

Is it better than owning MSTR directly?

“Better” depends entirely on objective. If the goal is monthly cash flow and some risk mitigation via reduced volatility exposure at the cost of upside, MSTE is structurally designed for that trade-off. If the goal is maximum long-term capital appreciation potential, direct MSTR ownership preserves more of that upside.

Is MSTE appropriate for retirement income?

Given its high risk rating, demonstrated volatility, leverage, and single-issuer concentration, it is generally not well-suited as a dependable retirement income source, particularly for investors who cannot tolerate significant capital drawdowns.

Final Verdict

MSTE is not a scam, and it is not mispriced marketing. It is exactly what its prospectus says it is: a leveraged, single-stock, actively managed covered call fund built on one of the most volatile equities trading on a major exchange. The mechanics are transparent and well-documented — the fund genuinely does generate the large premiums its strategy implies, and it genuinely does pass much of that premium through to unitholders as monthly cash distributions.

Important

The biggest misconception investors bring to a fund like MSTE is treating the yield figure as a return figure — assuming that a 70%+ annualized yield means the investment is “earning” 70% per year. It does not. The fund’s own performance history, with losses exceeding 80% over the trailing year and more than 60% since inception, demonstrates precisely why yield and total return must always be evaluated separately, especially in any fund built around a single volatile underlying stock.

Investors who understand options mechanics, who are comfortable with concentrated single-stock and crypto-adjacent risk, and who size the position as a small, actively monitored satellite holding may find MSTE does exactly what it was designed to do. Investors drawn in primarily by the headline yield, without appreciating the volatility, leverage, and capital-erosion risk sitting underneath that number, are taking on a very different — and considerably larger — risk than the yield figure alone would suggest.

As with any high-yield, single-stock, or leveraged product, the right first step isn’t deciding whether to buy or sell — it’s making sure you fully understand what you’d actually be holding.

note

This article is for educational purposes only and does not constitute financial, investment, or tax advice. WyzeInvestors is not affiliated with, and does not endorse, Harvest Portfolios Group Inc. or any ETF discussed. Fund data referenced is drawn from Harvest ETFs’ publicly available fact sheet and prospectus as at their most recent publication dates. Investors should consult the fund’s full prospectus, ETF Facts document, and a qualified financial or tax advisor before making any investment decision.