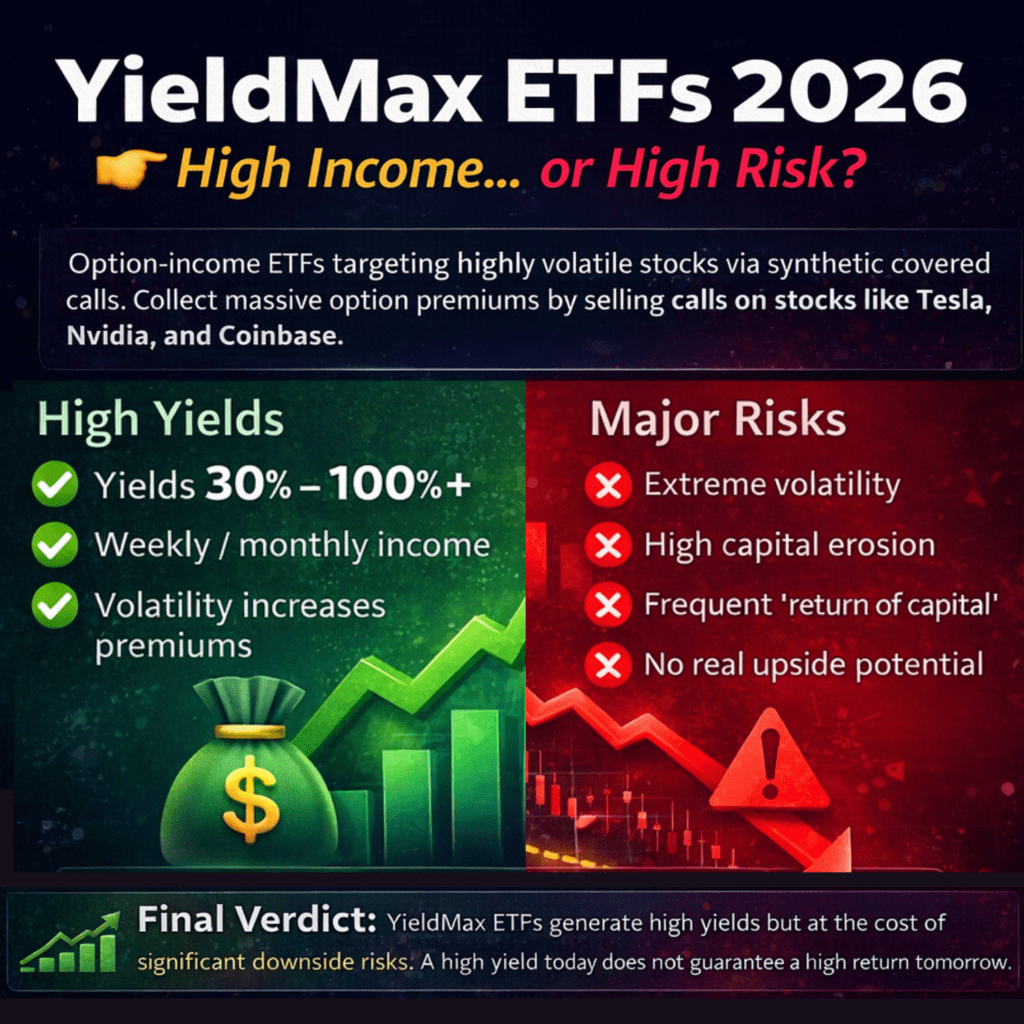

Income investing has changed — and it has changed fast. A few years ago, a 4% yield from a Canadian dividend ETF like VDY was considered solid. A 6% yield from a covered call strategy like ZWC felt aggressive. Today, we are talking about ETFs offering 30%, 50%, even 80%+ annual yields. Some even exceed 100%. At the center of this shift: YieldMax ETFs.

These funds have exploded in popularity, especially among retail investors chasing monthly or weekly income. With over 62 ETFs and $9 billion in assets under management, YieldMax has become one of the most talked-about — and most controversial — names in the ETF space. So the real question every income investor needs to answer in 2026 is this: are YieldMax ETFs the best income tools available right now, or are they simply the most dangerous? Let’s break it all down, clearly and honestly.

Executive summary

What Are YieldMax ETFs?

YieldMax ETFs are a category of option-income ETFs built around a very specific strategy. Instead of holding stocks and collecting dividends the traditional way, they use what is called a synthetic covered call strategy.

Here is how it works in plain language:

Rather than buying shares of Tesla, Nvidia, or Coinbase directly, YieldMax funds create a synthetic position that mimics owning the stock. They do this by simultaneously buying call options and selling put options on the same underlying asset at the same expiration date. On top of that synthetic position, they sell call options to collect premium income — and that premium gets distributed to shareholders as weekly or monthly income.

The key insight here is that YieldMax does not own the underlying stocks. This is fundamentally different from a traditional covered call ETF like JEPI or ZWC, which actually hold the underlying equities.

This structure allows YieldMax to target extremely high-volatility stocks — think Tesla, Nvidia, Coinbase, MicroStrategy — where option premiums are massive. And the more volatile the stock, the higher the premium income that can be collected.

The result: eye-catching yields that most investors have never seen before.

The Highest Yielding YieldMax ETFs Right Now (2026)

As of early 2026, here are some of the most extreme examples in the YieldMax lineup:

YMAX — YieldMax Ultra Option Income Strategy ETF A “fund of funds” that holds a basket of all individual YieldMax ETFs. This diversified approach still delivers yields in the 70–80%+ range, paid out weekly. It is often the starting point for investors who want broad YieldMax exposure without picking individual funds.

NVDY — YieldMax NVDA Option Income Strategy ETF Tied to Nvidia, one of the most volatile mega-cap stocks in the world. NVDY has shown strong performance, with the fund up roughly 40% over the past year on a total return basis. However, the most recent distribution contains approximately 94.67% return of capital, which is a critical detail we will discuss below.

TSLY — YieldMax TSLA Option Income Strategy ETF The original YieldMax ETF, launched in late 2022. TSLY is tied to Tesla and has delivered annualized yields cited as high as 75%. It has paid out over $10.78 in distributions in a single year. The most recent distribution contains approximately 92.66% return of capital. The fund now holds around $950 million in assets and has appreciated roughly 53% over the past year.

CONY — YieldMax COIN Option Income Strategy ETF Tied to Coinbase, one of the most volatile assets in the lineup. CONY has seen yields exceed 100% at various points. However, it has also experienced significant NAV erosion — the fund is down roughly 30% over the past year even after distributions. This is the starkest illustration of the risk embedded in single-name crypto-adjacent strategies.

MRNY — YieldMax MRNA Option Income Strategy ETF Based on Moderna, another extremely volatile underlying. MRNY offers yields in the 80%+ range, reflecting the massive implied volatility embedded in biotech stocks with high uncertainty around their pipelines.

Why Are the Yields So High? The Volatility Connection

The secret behind these extraordinary yields is not magic — it is volatility.

Option premiums are priced based largely on implied volatility. When a stock like Tesla or Coinbase swings 5–10% in a single day, options on that stock carry enormous premiums. When YieldMax sells those call options, they collect that premium and pass it along to shareholders.

In March 2026, the VIX — the broad market measure of volatility expectations — closed at approximately 29.49, up roughly 58% over the prior month. This elevated volatility environment is directly inflating the distributions these funds are generating right now.

The formula is simple: higher volatility = higher premiums = higher yield distributions.

This is why YieldMax yields surge during periods of market stress and compress during calm, trending bull markets. It is also why the current environment — characterized by macroeconomic uncertainty, trade policy disruption, and elevated market volatility — is in many ways ideal for this strategy on a short-term basis.

The Hidden Reality You Cannot Ignore

Here is where the conversation gets critical — and where many investors get hurt.

1. Capital Erosion and the Yield Illusion

High yield does not equal high return. This is the most important concept to understand about YieldMax ETFs.

When a fund distributes 80% of its value as income in a year, but its share price declines by 60%, you have not made money — you have lost it. This phenomenon is often called yield illusion: the income looks incredible, but the total picture tells a very different story.

CONY is the clearest example. Despite consistently high distributions, its share price is down roughly 30% over the past year. Investors who did not factor in NAV erosion alongside their income collected may be significantly underwater in total return terms.

2. Return of Capital (ROC) — Not All Income Is What It Seems

This is perhaps the most overlooked risk in the YieldMax story.

Look closely at the most recent distributions for NVDY and TSLY: approximately 94.67% and 92.66% respectively are classified as return of capital. This means the fund is essentially returning your own money to you, dressed up as a distribution.

Return of capital is not taxable in the year received (it reduces your adjusted cost base instead), but it is also not real income generated from the market. When the majority of a distribution is ROC, the fund is essentially liquidating itself slowly to maintain its payout schedule. Over time, this erodes the NAV and reduces future income potential.

This does not make these funds worthless — but it makes understanding your tax statements and total return calculations absolutely essential.

3. Capped Upside — You Miss the Rallies

Because YieldMax funds sell call options on their underlying positions, they cap how much they can participate in upside price movement. If Nvidia surges 40% in a quarter, NVDY will not capture that full return. The call options that were sold limit participation above the strike price.

This creates a fundamental asymmetry: you bear the downside risk of holding exposure to a volatile stock, but you give up much of the upside in exchange for current income. In a strong sustained bull market, this tradeoff becomes very expensive.

4. Single-Name Concentration Risk

Most individual YieldMax ETFs are tied to a single stock. TSLY lives or dies with Tesla. CONY is entirely dependent on Coinbase’s trajectory. MRNY is a pure play on Moderna.

These are not diversified income portfolios. They are concentrated bets on highly volatile, sentiment-driven assets. If Tesla drops 50% — which it has done before — TSLY will follow it down, and the option premiums collected along the way will not come close to making up the difference for most investors.

When Do YieldMax ETFs Actually Work?

To be fair, there are market environments where this strategy performs well:

Sideways or mildly bullish markets are the sweet spot. When the underlying stock moves in a tight range, the covered call strategy collects premium repeatedly without missing significant gains. The income accumulates without meaningful NAV erosion.

High volatility environments — like the current one in early 2026 — produce especially generous distributions. When implied volatility is elevated across the market, option premiums swell, and YieldMax payouts increase accordingly.

Short to medium-term income needs are best served by these funds. If your goal is to maximize cash flow over 12–24 months and you have a clear view of the risk, YieldMax can deliver on its promise.

Where they struggle: in a sustained, powerful bull run, covered call strategies consistently lag simple index investing. And in a sharp market crash, the income collected does not offset the rapid NAV decline, leaving investors worse off than if they had simply held the underlying stock or a diversified ETF.

YieldMax vs. Traditional Income ETFs: A Realistic Comparison

| Type | Yield | Risk Level | Stability | Capital Preservation |

| Dividend ETFs (VDY, XEI, SCHD) | 3–5% | Low | High | Strong |

| Covered Call ETFs (JEPI, QYLD, ZWC) | 6–10% | Medium | Medium | Moderate |

| YieldMax ETFs (NVDY, TSLY, CONY) | 30–100%+ | Very High | Low | Weak to None |

The right framework is not to ask which is better in absolute terms — it is to ask what role each plays in your specific portfolio, time horizon, and income objective.

So Which YieldMax ETF Is the “Best” Right Now?

There is no single correct answer, but here is a practical framework based on risk tolerance:

For a more balanced approach (still very risky): NVDY and TSLY offer exposure to two of the most widely followed stocks in the world. Both have shown positive price performance over the past year, which changes the total return math favorably compared to CONY and MSTY. If you are going to engage with YieldMax, these two offer slightly more stability relative to the group.

For maximum income (extremely aggressive): CONY (Coinbase) and MSTY (MicroStrategy) offer some of the highest yields in the entire ETF universe. But both have experienced severe NAV erosion — MSTY is down approximately 45% over the past year. These are speculative instruments, not income replacements.

For diversified YieldMax exposure: YMAX holds the entire basket of YieldMax funds and pays distributions weekly. It gives you exposure to the income strategy without betting everything on a single name. The yield remains extraordinary while spreading the concentration risk across multiple underlying assets.

The Right Way to Use YieldMax in a Portfolio

If you decide to include YieldMax ETFs in your strategy, the most responsible approach is to treat them as a satellite allocation — not a core holding.

A reasonable framework:

- Limit total YieldMax exposure to 5–20% of your overall portfolio

- Pair them with dividend ETFs (VDY, XEI, ZWC) that offer more stable income and better capital preservation

- Pair them with growth ETFs (XEQT, VFV, XQQ) that build long-term wealth even when YieldMax underperforms

- Track total return, not just distributions. Use a spreadsheet or tracker to monitor your cost basis, distributions received, and current NAV — the full picture, not just the income column

- Understand your tax situation. Return of capital impacts your adjusted cost base, which affects capital gains calculations when you eventually sell. Consult a tax professional if this is new territory for you

Final Verdict

YieldMax ETFs are a genuinely new category of investment product. They are not frauds, and they are not magic. They are volatility harvesting tools that convert market uncertainty into current income — with very real trade-offs attached.

If your goal is maximum monthly cash flow and you fully understand the risks — including NAV erosion, return of capital, capped upside, and concentration in volatile single stocks — YieldMax can deliver on its income promise in the right market conditions.

If your goal is long-term wealth building, capital preservation, or retirement income you can depend on for decades, YieldMax ETFs should represent a very small portion of your strategy at most.

The real skill in income investing in 2026 is not chasing the highest yield you can find. It is understanding exactly what you are buying — the mechanics, the risks, and the total return picture — before you commit your capital.

A 70% yield that destroys 60% of your capital has not made you wealthy. It has made you feel rich while quietly making you poorer.

Invest accordingly.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Always consult a qualified financial advisor before making investment decisions.