For a Canadian investor with $200,000, targeting $1,000 per month in passive income (about 6% annual yield) represents a real turning point.

At this level, you move:

From pure accumulation

To a strategic income management approach

The goal is no longer just growth, but predictable cash flow.

Here are three concrete portfolio structures, adapted to different investor profiles:

from direct stock ownership to hybrid models using covered call ETFs.

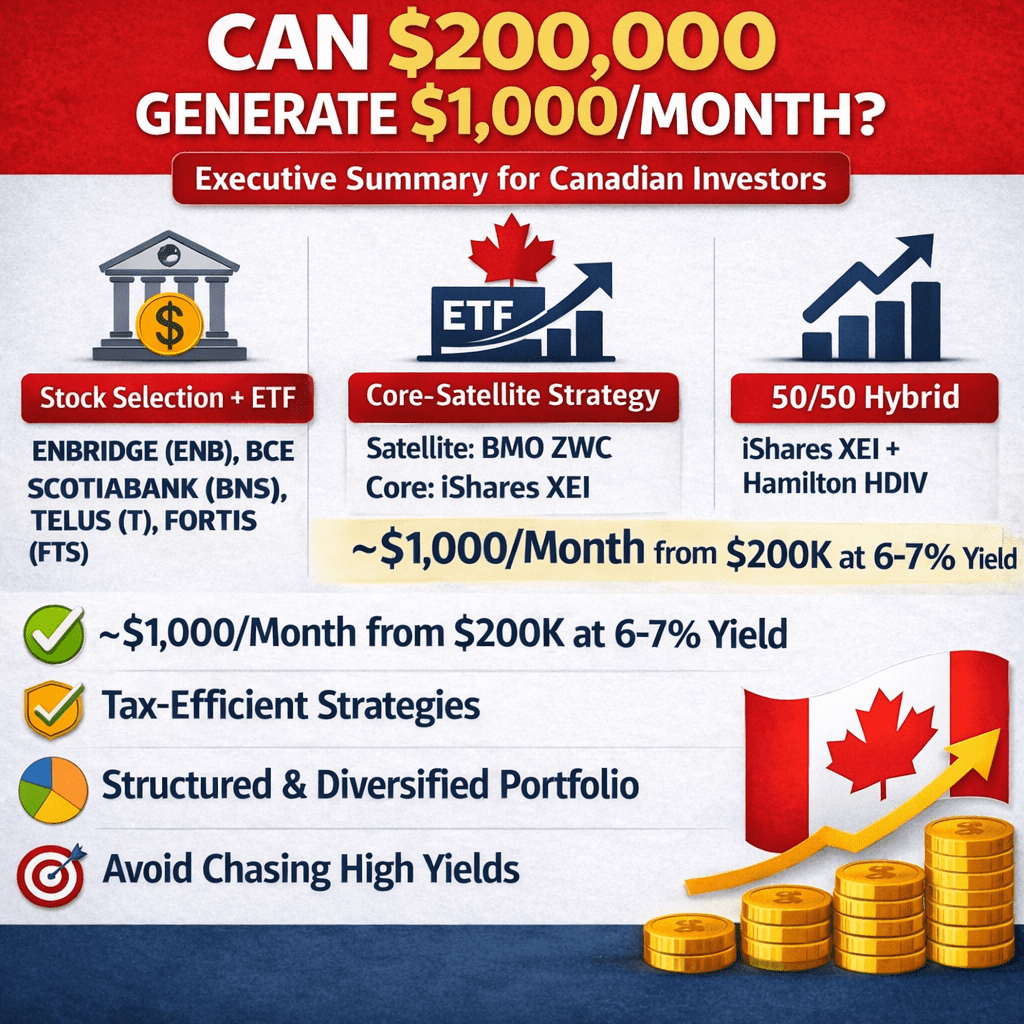

Executive summary

🔹 Model 1: Stock Selection

🎯 Who is it for?

This model is designed for investors who want to maintain some control over their portfolio while improving diversification through a dividend ETF. By combining a few strong Canadian stocks with a diversified ETF, it is possible to generate stable income while reducing the risk tied to any single company.

This approach suits investors who want to:

- limit sector concentration

- benefit from the Canadian dividend tax credit

- simplify portfolio management

The sectors historically known for strong dividends remain:

- Energy

- Telecommunications

- Banks

- Utilities

Adding an ETF like XEI helps create a diversified base composed of several major Canadian companies.

Example Allocation

This allocation prioritizes dividend stability and improved diversification.

| Stock / ETF | Allocation | % | Est. Yield | Annual Income |

|---|---|---|---|---|

| iShares XEI | $60,000 | 30% | 4.20% | $2,520 |

| Enbridge (ENB) | $30,000 | 15% | 5.33% | $1,599 |

| Bank of Nova Scotia (BNS) | $30,000 | 15% | 4.53% | $1,359 |

| Telus (T) | $30,000 | 15% | 9.28% | $2,784 |

| Fortis (FTS) | $30,000 | 15% | 3.25% | $975 |

| BCE (BCE) | $20,000 | 10% | 4.85% | $970 |

| Total | $200,000 | 100% | 5.10% | $10,207 |

💵 Estimated monthly income: ~ $850

This example highlights an important reality for income investors: with solid and diversified companies, portfolio yields often land around 5%. Reaching $1,000 per month purely from dividends would typically require about 6% yield, which often means higher concentration or more risk.

✅ Advantages

Combining individual stocks with an ETF allows investors to benefit from attractive dividends and better diversification.

- Instant diversification through the ETF

- Tax advantage from Canadian dividend credits

- Exposure to several key sectors of the economy

Investors can also adjust positions over time as market conditions evolve.

⚠️ Risks

Even with an ETF, certain risks remain.

Sector concentration

The Canadian market remains heavily exposed to a few sectors such as energy, banks, and telecommunications.

Interest rate sensitivity

High-dividend stocks can react negatively when interest rates rise.

Company-specific risk

Some stocks may show high yields because their share price is under pressure.

Income Enhancement with Covered Calls

To get closer to the $1,000 per month goal, some investors use a covered call strategy on certain portfolio positions.

The principle is to sell call options on stocks already owned, collecting an option premium. A conservative approach typically involves selling options with a 30% delta and about one-month expiration.

Depending on the stock’s volatility, this strategy can generate 0.5% to 1% additional income per month. On a $200,000 portfolio, that can represent $1,000 to $2,000 per year, helping close the gap between $850 and the $1,000 monthly target.

However, this strategy also has limitations. If the stock rises above the strike price, the shares may be called away, limiting capital gains. If the stock falls, the option premium only partially offsets the loss.

Covered calls can increase income, but they require active and disciplined management.

This approach still offers reasonable growth potential while generating attractive monthly income, making it suitable for investors seeking both stability and yield.

🔹 Model 2: Core–Satellite (Stability + Yield Boost)

🎯 Who is it for?

The Core–Satellite model is a strategic approach combining stability with improved yield. It allows investors to maintain a solid diversified base while using part of the portfolio to increase monthly distributions.

This structure reduces risk compared to a fully high-yield strategy, while still helping investors approach the $1,000 per month goal with $200,000 invested.

This model is especially suited for:

- investors seeking the stability of a diversified ETF

- those wanting to increase their monthly income

- those preferring a simple and structured portfolio

In practice, the portfolio is divided into two complementary components:

Core → diversified and relatively stable foundation

Satellite → strategies designed to enhance income

The core provides stability, while the satellite portion acts as a measured lever to increase total income.

Example Allocation

| Component | Type | Allocation | % | Est. Yield | Annual Income |

|---|---|---|---|---|---|

| iShares XEI | Core Foundation | $120,000 | 60% | 4.20% | $5,040 |

| BMO ZWC | Satellite (Stability) | $40,000 | 20% | 5.84% | $2,336 |

| Hamilton HDIV | Satellite (Diversified) | $40,000 | 20% | 10.55% | $4,220 |

| TOTAL | $200,000 | 100% | 5.80% | $11,596 |

💵 Estimated monthly income: ~ $966

CORE – Portfolio Foundation

iShares S&P/TSX Composite High Dividend ETF (XEI) forms the base of the portfolio. This ETF provides exposure to several dozen Canadian dividend-paying companies.

It includes:

- banks

- energy companies

- telecommunications

- utilities

- some industrial sectors

Advantages of the CORE:

- broad sector diversification

- exposure to strong Canadian companies

- regular distributions

- simple structure without leverage

XEI acts as the stable foundation of the portfolio, combining income with long-term growth potential.

SATELLITE – Yield Enhancement

The satellite portion aims to increase portfolio distributions using income-focused strategies.

BMO ZWC primarily invests in major Canadian banks while using covered calls to generate additional option premiums.

Hamilton HDIV adds further diversification by combining multiple sectors and income strategies, helping boost overall portfolio yield.

Advantages of the satellite portion:

- higher monthly distributions

- improved overall yield

- additional diversification

Total Income

Core: ~ $5,040

Satellite ZWC: ~ $2,336

Satellite HDIV: ~ $4,220

Total: ~ $11,596 per year

💵 Monthly income: ~ $966

Why This Model Works

This portfolio relies on a balance between stability and enhanced yield.

Most capital is invested in XEI, providing diversification across many strong Canadian companies.

The satellite portion, using strategies such as covered calls, increases monthly distributions without relying solely on individual stocks.

This structure provides a balanced approach between:

- diversification

- income

- risk management

- simplicity

while helping investors approach the goal of $1,000 in monthly income with $200,000 invested.

🔹 Model 3: The 50/50 Hybrid (Growth + Volatility Monetization)

🎯 Who is it for?

Investors who want:

- stable income

- protection in sideways markets

- a more robust strategy

Here, capital is divided between a base of dividend exposure and a higher-yield income strategy.

50% – XEI ($100,000)

iShares S&P/TSX Composite High Dividend (XEI)

Yield: ~4.20%

Annual income: $4,200

Exposure:

- about 70 Canadian companies

- broad sector diversification

- banks, energy, telecom, utilities

XEI acts as the portfolio foundation, providing stable income and growth potential.

50% – HDIV ($100,000)

Hamilton Enhanced Multi-Sector Covered Call ETF (HDIV)

Yield: ~10.50%

Annual income: $10,500

Strategy:

- multi-sector portfolio

- covered calls to generate option premiums

- exposure to banks, energy, and utilities

HDIV aims to monetize market volatility to increase monthly distributions.

Total Income

$4,200

$10,500

Total: $14,700

💵 Monthly income: ~ $1,225

Overall yield: ~7.35%

Why This Model Is Robust

- XEI captures growth and stabilizes the portfolio

- HDIV generates option premiums and boosts distributions

- the combination increases yield without relying only on traditional dividends

This model works particularly well if:

- markets stagnate

- volatility remains elevated

- interest rates remain relatively stable

In that environment, covered call strategies can continue generating additional income, allowing investors to achieve higher passive income while maintaining a diversified base.

⚠️ Risks and Limitations of Covered Call ETFs

Covered call ETFs can offer higher yields, but they also have limitations.

Limited upside potential

If markets rise strongly, shares may be called away due to the options sold, limiting participation in large market gains.

Income depends on volatility

Option premiums increase with volatility. In calmer markets, distributions may decline.

For this reason, covered call ETFs are often used as an income complement within a diversified strategy, rather than as the sole foundation of a portfolio.

📊 Strategy Comparison

| Strategy | Annual Income | Monthly Income | Complexity | Growth Potential | Diversification |

|---|---|---|---|---|---|

| Stock Selection + ETF | ~ $10,207 | ~ $850 | High | Good | Moderate |

| Core–Satellite | ~ $11,596 | ~ $966 | Low | Good | High |

| Hybrid 50/50 | ~ $14,700 | ~ $1,225 | Medium | Moderate | Very good |

Important Tax Note

The tax structure of the account used directly impacts the net return of your income strategy.

In a taxable account:

Canadian dividends benefit from the dividend tax credit, reducing taxes compared to interest income. Covered call premiums are often treated as capital gains when used non-speculatively, which can be tax-efficient. Only 50% of capital gains are taxable, improving after-tax returns.

👉 Models 1 (individual stocks) and 3 (hybrid approach with options) can therefore be more tax-efficient in a taxable account.

In a TFSA:

All income — dividends, capital gains, and option premiums — is 100% tax-free.

In an RRSP:

Taxes are deferred until withdrawal at retirement, which may be advantageous if your current tax rate is high.

⚠️ Common Pitfalls

Trying to generate $1,000 per month with $200,000 is realistic, but several pitfalls can undermine the strategy.

1. Chasing very high yields (>9%)

Very high yields often signal higher risk or potential dividend cuts.

2. Ignoring capital erosion

Stable income is not enough if portfolio value declines over time.

3. Underestimating sector cyclicality

Banks and energy can provide strong dividends but remain sensitive to economic cycles.

4. Not rebalancing annually

Without rebalancing, a portfolio may become overly concentrated.

🚀 Growth Strategy: From $200,000 to $500,000

If you reinvest:

Average return: 6%

Annual contributions: $10,000

Approximate projection:

~ $350,000 in 10 years

~ $500,000 in 15–18 years

At $500,000:

6% = $30,000 per year

$2,500 per month

That’s when passive income becomes truly transformative.

🎯 Conclusion: $1,000 per Month Is Realistic… but Strategic

Generating $1,000 per month with $200,000 is not unrealistic. It’s not marketing hype — it’s an achievable goal for a disciplined investor.

But the result does not rely solely on yield. It depends on portfolio architecture.

What makes the difference:

• Structure: choosing the right vehicles (stocks, ETFs, covered calls)

• Tax efficiency: optimizing account types

• Diversification: avoiding reliance on one sector

• Discipline: rebalancing and resisting market hype

The real challenge is not achieving 6% for one exceptional year, but building a durable, predictable, and resilient income stream.

A well-constructed $200,000 portfolio can become much more than an investment — it can become a financial freedom engine, funding projects, reducing career pressure, or accelerating financial independence.