At first glance, DGS (Dividend Growth Split Corp.) looks like a powerful income vehicle. It offers high monthly distributions, exposure to well-known Canadian dividend growth companies, and a long operating history.

However, DGS is not a traditional ETF, and it does not behave like one. It is a split share corporation, a structure that can enhance income and returns in favorable markets—but also introduces unique risks that investors must understand before allocating capital.

This article explains how DGS works, where its income really comes from, and the key risks embedded in the structure, so investors can evaluate whether it fits their portfolio objectives. DGS is issued and managed by Brompton Funds, a Canadian firm specializing in income-oriented products, particularly split-share corporations.

1. What Is DGS?

DGS is a split share fund that holds a diversified portfolio of large-cap Canadian dividend growth stocks. Instead of issuing a single class of units like a standard ETF, it issues two separate securities:

- Preferred Shares (DGS.PR.A)

Designed to provide relatively stable income and capital priority. - Class A Shares (DGS)

Designed to provide higher income and potential capital appreciation.

Each “unit” of the fund consists of:

- 1 Preferred share

- 1 Class A share

This structure creates embedded leverage for the Class A shares.

2. What Does DGS Invest In?

DGS holds a portfolio of established Canadian dividend-paying companies, primarily large-cap issuers with a history of earnings growth and cash-flow generation.

The portfolio includes:

- Major Canadian banks and insurers

- Infrastructure and utilities

- Consumer staples and defensive growth companies

- Select resource and industrial names

This is not a speculative portfolio. The underlying assets are fundamentally strong businesses commonly found in dividend growth and quality-focused strategies.

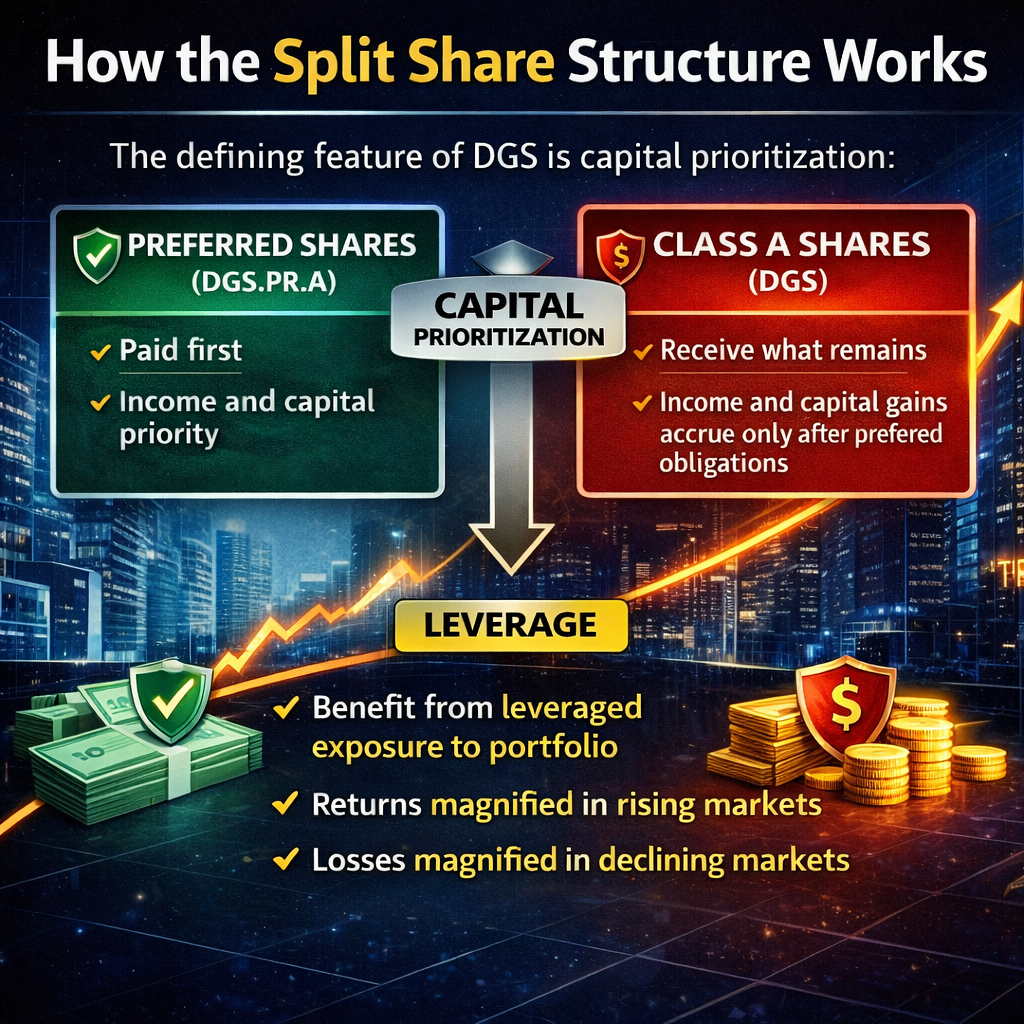

3. How the Split Share Structure Works

The defining feature of DGS is capital prioritization:

- Preferred shareholders are paid first

They have priority on dividends and on capital at maturity. - Class A shareholders receive what remains

Income and capital gains accrue only after preferred obligations are met.

As a result:

- Class A shares benefit from leveraged exposure to the underlying portfolio

- Returns are magnified in rising markets

- Losses are magnified in declining markets

This leverage is structural, not optional.

4. Where Do Class A Distributions Come From?

Class A distributions are monthly and are primarily return of capital (ROC).

This means distributions may be funded by:

- Dividends received from portfolio holdings

- Capital gains

- Portfolio cash flow

- A return of investors’ original capital

Return of capital is not inherently negative, but it has two important implications:

- It reduces the fund’s net asset value (NAV) if not offset by asset appreciation

- It lowers the investor’s adjusted cost base (ACB) in taxable accounts

Income investors should focus on NAV sustainability, not just headline yield.

5. The Most Important Risk: Distribution Suspension

The single most important risk for investors in Class A shares (DGS) is the risk of distribution suspension. This risk is structural and embedded in how split share funds are designed.

How the rule works

Class A distributions are not guaranteed. They are paid only if two conditions are met:

- Preferred shareholders are fully paid first

If preferred share distributions (DGS.PR.A) are in arrears, Class A receives nothing. - NAV coverage test is respected

After paying the Class A distribution, the Net Asset Value per unit must remain above a predefined minimum level.

If paying income would push NAV below that threshold, the distribution is automatically suspended.

This is not a discretionary decision by the manager—it is a hard rule written into the fund’s structure.

What this means in real markets

During sharp or prolonged market declines:

- Class A distributions can stop entirely

- The Class A share price often falls faster than the underlying stocks because leverage works in reverse

- Income-focused investors may experience months (or longer) with zero cash flow

Meanwhile, preferred shares continue to receive priority payments as long as coverage allows.

Why this matters

Many investors focus on the headline yield of Class A shares without fully appreciating that:

- The income is conditional

- The leverage is structural and permanent

- Income risk increases precisely when markets are under stress

Understanding this risk is essential before using DGS Class A as an income replacement rather than a tactical or satellite position in a portfolio.

6. Leverage Risk and Market Drawdowns

Because Class A shares are effectively leveraged:

- Gains are amplified in rising markets

- Drawdowns are deeper during market stress

A moderate decline in the portfolio can translate into a disproportionate decline in Class A NAV. This makes DGS unsuitable for investors who require stable income in all market environments.

7. Interest Rate Sensitivity

Although DGS holds equities, it is indirectly sensitive to interest rates:

- Preferred shares are rate-sensitive instruments

- Rising interest rates can pressure preferred valuations

- That pressure flows through to Class A NAV

This means DGS can underperform during periods of rising rates even if equity markets are stable.

8. Term and Extension Risk

DGS has a stated maturity date, after which:

- The fund may be terminated, or

- The term may be extended by the board

At maturity or extension:

- Dividend terms may change

- Market prices may diverge from NAV

- Investors face reinvestment risk

This makes DGS less predictable than perpetual ETFs.

9. Is DGS “Safe”?

DGS is not a low-risk product, but it is also not inherently flawed.

It may be suitable for:

- Experienced income investors

- Portfolios that can tolerate income variability

- Tactical allocations during stable or rising equity markets

It is not suitable as:

- A bond substitute

- A guaranteed income vehicle

- A core retirement holding requiring steady cash flow

Historical performance

Source: Brompton Funds site

Preferred Shares: Stable, Bond-Like Returns

The Preferred series shows very consistent returns, generally in the 5.4%–6.9% range year after year.

This reflects its senior, quasi-fixed-income nature:

- Fixed distribution paid first (~6%)

- Priority claim on assets

- Low volatility

- Limited participation in portfolio upside

👉 Preferred shareholders are buying income stability, not growth.

Class A: Residual + Embedded Leverage

The Class A returns are dramatically higher—but also far more volatile:

- 1-Year: 37.6%

- 5-Year: 32.7%

- 10-Year: 19.1%

- Individual years range from +92% to −41%

This happens because Class A:

- Receives only what remains after the Preferred distribution is paid

- Absorbs all upside and downside beyond the Preferred claim

- Has structural leverage built into it

In practical terms:

The Preferred distribution acts like a fixed financing cost, and Class A is the equity layer above it.

When markets are strong, this structure amplifies returns.

When markets are weak, losses are magnified.

10. How DGS Fits in a Portfolio

DGS should be viewed as a satellite income position, not a core holding. Its split-share structure introduces structural leverage and conditional distributions, which can enhance income in favorable markets but increase downside risk during periods of stress. For this reason, position sizing is critical.

A prudent approach is to limit exposure and integrate DGS alongside more stable income assets. It pairs best with traditional dividend ETFs, which provide diversified, unlevered exposure to dividend-paying companies, as well as utilities or infrastructure investments that offer regulated, predictable cash flows. Adding bonds or cash equivalents can further stabilize the portfolio and provide liquidity during market drawdowns, when DGS distributions may be suspended.

Importantly, investors should focus less on headline yield and more on NAV trends. A declining NAV can signal rising risk to Class A distributions, regardless of current payout levels. In practice, DGS works best as an opportunistic income enhancer within a diversified, risk-aware portfolio—not as a primary income foundation.

Summary:

- Treat DGS as a satellite income position

- Limit position size

- Combine with:

- Traditional dividend ETFs

- Utilities or infrastructure

- Bonds or cash equivalents

Monitoring NAV trends is more important than monitoring yield alone.

Final Thoughts

DGS can be a powerful income tool when used correctly. Its appeal lies in its ability to convert a high-quality dividend growth portfolio into enhanced income through structural leverage.

However, that same structure introduces:

- Income interruption risk

- Amplified volatility

- Sensitivity to market cycles and interest rates

The key question for investors is not:

“Is the yield attractive?”

But rather:

“Can I tolerate leveraged drawdowns and suspended income during market stress?”

Answering that honestly is essential before investing in DGS