Dividend investing is one of the most popular strategies among Canadian investors.

The idea is simple and powerful:

• Generate regular income from dividends

• Benefit from long-term capital appreciation

But there is an important reality many investors overlook.

👉 Not all dividends are safe.

Sometimes a very high yield is not a sign of strength… but a warning signal. When a company’s fundamentals weaken while the dividend remains high, investors may face what is commonly called a dividend trap.

A dividend trap occurs when:

• the stock price falls significantly

• the dividend yield rises artificially

• the payout becomes difficult to sustain

When that happens, companies may eventually have to:

❌ cut the dividend

❌ freeze dividend growth

❌ or restructure their payout policy

And historically, dividend cuts often trigger sharp stock price declines. For long-term investors, dividend safety matters just as much as dividend yield. In this article we examine five Canadian dividend stocks currently under closer scrutiny by analysts in 2026. This does not mean a dividend cut is inevitable, but it does mean investors should pay closer attention to the financial fundamentals.

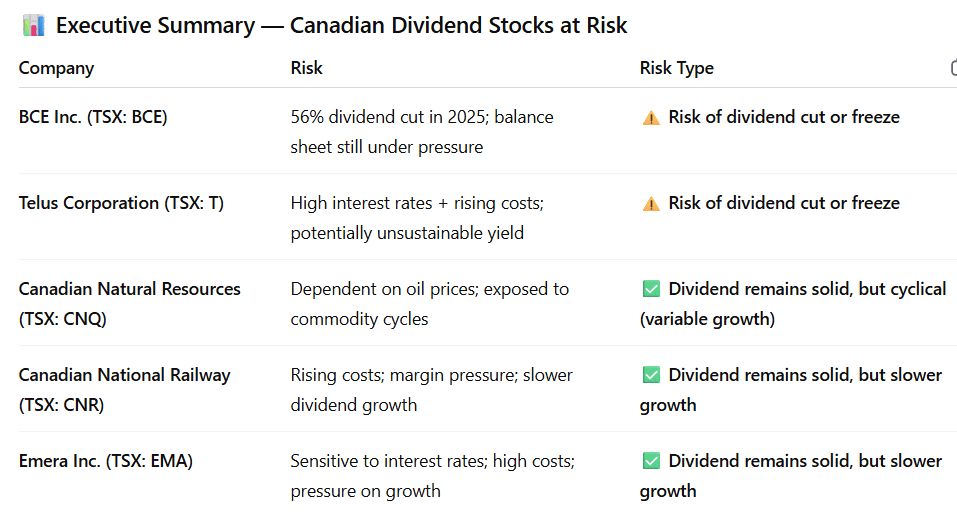

Executive summary

Why Dividend Safety Matters

A sustainable dividend usually comes from companies with several key characteristics:

✔ stable and predictable cash flows

✔ reasonable payout ratios

✔ manageable debt levels

✔ strong competitive positions

When one or more of these factors deteriorates, the dividend can become vulnerable.

The risk increases when companies simultaneously face:

• rising interest rates

• slower economic growth

• heavy capital spending requirements

• declining commodity prices

In those cases, maintaining a large dividend may compete with other priorities such as:

• debt reduction

• infrastructure investment

• business transformation

For dividend investors, the key is not just the yield today — but the sustainability of the payout tomorrow.

5 Canadian Dividend Stocks That Could Cut Their Dividend in 2026

1. BCE Inc. (TSX: BCE)

Key Takeaways

- Dividend cut by ~56% in 2025

- Still under financial pressure

- Investing heavily in new growth areas

- Debt remains elevated

- No longer a “defensive” dividend stock

Analysis

BCE was long considered one of the most reliable dividend-paying companies in Canada, often viewed as a cornerstone holding for income-focused investors. That perception changed significantly in 2025, when the company reduced its dividend by approximately 56%, highlighting the reality that even established businesses can face meaningful financial constraints. While the reset has lowered the payout burden, BCE is still navigating a challenging transition period.

The company is actively repositioning its business model by allocating more capital toward growth initiatives such as AI infrastructure and U.S. enterprise services, moving away from its traditional telecom focus. Although this strategy may strengthen long-term competitiveness, it also requires substantial upfront investment, which continues to weigh on financial flexibility. At the same time, BCE’s debt levels remain elevated, limiting its ability to comfortably support both expansion and shareholder returns in a higher interest rate environment.

As a result, the investment case has shifted. BCE can no longer be viewed as a purely defensive income stock, but rather as a company in transition with execution risk. The key consideration for investors is whether the business can generate sufficient cash flow to stabilize its balance sheet while maintaining its dividend. Until there is clearer evidence of improvement, a degree of caution remains warranted.

round play, not a defensive anchor. The value “trap” risk remains high until the company proves it can grow earnings faster than it spends on fiber maintenance. Investors should demand a “margin of safety”—buying only when the entry price offers a significant discount to historical book value.

2. Telus Corporation (TSX: T)

Key Takeaways

- Dividend yield near ~9.5% signals elevated risk

- Dividend growth model under pressure

- Debt remains high (~3.8x range)

- Expansion outside telecom not delivering as expected

- Risk of dividend freeze or cut increasing

Analysis

Telus has historically been viewed as one of Canada’s most consistent dividend growth stories, supported by its long-standing commitment to increasing shareholder payouts. However, that same commitment is now becoming a source of pressure. For the first time in many years, the market is questioning whether the current dividend policy is sustainable, particularly given the company’s elevated yield and financial positioning.

A key factor behind this shift is Telus’s diversification strategy. The company has expanded into areas such as health, agriculture, and international services, but these segments have not yet generated the level of profitability initially expected. As a result, the core telecom business continues to carry the majority of the financial burden, including supporting the dividend.

At the same time, Telus operates with relatively high leverage, which becomes more challenging in a higher interest rate environment. While capital spending is expected to moderate following years of heavy investment in network infrastructure, the timing and magnitude of this improvement remain important variables.

3. Canadian Natural Resources (TSX: CNQ)

Key Takeaways

- Dividend strength tied directly to oil prices

- Strong track record, but cyclical risk remains

- Cash flow can fluctuate significantly

- Dividend appears safe if commodity prices hold

- Vulnerable in a downturn

Analysis

Canadian Natural Resources is widely recognized as one of Canada’s strongest energy companies, with a long history of disciplined capital allocation and consistent dividend growth. However, unlike telecoms or utilities, its business model is inherently tied to the commodity cycle. This means that while the dividend can appear very secure during periods of strong oil prices, it is ultimately dependent on external factors that the company cannot control.

The key dynamic to understand is that CNQ’s financial strength rises and falls with the price of oil. When crude prices remain elevated, the company generates significant free cash flow, allowing it to comfortably fund dividends, reduce debt, and return capital to shareholders. In this environment, the dividend looks both sustainable and attractive.

However, the situation can change quickly if market conditions deteriorate. A meaningful decline in oil prices would reduce cash flow and limit financial flexibility, forcing management to prioritize balance sheet stability over shareholder returns. While CNQ has proven resilient in past cycles, it is not immune to prolonged downturns.

👉 The dividend is strong, but not immune.

👉 This is not a defensive income stock — it is a cyclical income play.

For investors, the key is not just evaluating the company, but also forming a view on the broader commodity environment.

For decades, CNR was the ultimate “set it and forget it” stock. As a duopoly in the Canadian rail sector with a massive moat, it has raised dividends for 28 consecutive years. However, in 2026, the narrative is shifting from “guaranteed growth” to “stagnant margins.”

4. Canadian National Railway (TSX: CNR)

Key Takeaways

- Dividend remains very safe

- Yield relatively low (~2%)

- Growth slowing due to higher costs

- Heavy investment cycle underway

- Risk is slower dividend growth, not a cut

Analysis

Canadian National Railway remains one of the highest-quality businesses in Canada, supported by a dominant market position and a long track record of dividend growth. However, the story is evolving. In 2026, the key question is no longer whether the dividend is safe, but rather how fast it can continue to grow.

The company is currently going through a significant investment phase. In order to maintain its competitive advantage and adapt to new environmental and operational standards, CNR is allocating substantial capital toward infrastructure upgrades and new technologies. While these investments are necessary for long-term efficiency, they reduce the amount of cash available for immediate distribution to shareholders.

At the same time, cost pressures are beginning to build. Rising labor expenses, fuel costs, and operational complexity are gradually impacting margins, which historically supported strong dividend growth. As a result, future increases in the dividend may be more modest than what investors have been accustomed to in the past.

👉 The dividend itself remains secure.

👉 The real risk is a slowdown in growth, not a cut.

If dividend growth moderates from historical levels toward a lower range, the stock could also see a shift in valuation. For investors, CNR remains a core holding, but expectations may need to adjust to a more moderate return profile.

g, but it is no longer a “get rich quick” income play. In 2026, the value lies in its inflation-hedging power. If you own CNR, you aren’t buying for the yield (currently ~2%); you are buying for the “monopoly” power to raise freight rates when prices rise elsewhere

5. Emera Inc. (TSX: EMA)

Key Takeaways

- Attractive yield (~6–7%)

- Dividend track record remains strong

- Heavy investment phase underway

- Sensitive to interest rates and borrowing costs

- Risk of dividend growth slowing or freezing

Analysis

Emera has long been viewed as a dependable utility for income investors, supported by a stable business model and a consistent history of dividend increases. However, its traditionally defensive profile is being tested in the current environment. The company is in the middle of a capital-intensive phase, investing heavily in infrastructure and energy transition projects, particularly in Florida and Nova Scotia. While these investments are necessary to support long-term growth, they require significant financing.

Utilities rely heavily on debt, and in a higher interest rate environment, the cost of that debt becomes a key pressure point. As borrowing costs rise, more cash flow is directed toward servicing debt rather than supporting dividend growth. At the same time, utilities operate under regulatory frameworks that limit how quickly they can pass increased costs onto customers, which adds another layer of constraint.

👉 The dividend itself appears relatively secure.

👉 The main risk is slower growth, not an immediate cut.

Management has already signaled a more cautious approach, with expectations for lower annual increases as the company focuses on maintaining its financial strength. For investors, Emera remains primarily a yield-focused investment, but those expecting strong dividend growth may need to adjust their expectations in the current environment.

eats inflation, Emera’s current transition phase may make it a laggard compared to less-leveraged utilities like Fortis (FTS).

What Investors Should Watch

What Dividend Investors Should Watch

A high yield alone does not make a stock attractive. In many cases, the real story is found in a few core signals that help reveal whether a dividend is solid, stretched, or vulnerable.

Payout Ratio

If a company is paying out too much of its profits, the dividend becomes harder to maintain. A payout that looks manageable today can quickly become a problem if earnings weaken.

Too high = warning signDebt Levels

Companies carrying heavy debt are more exposed when interest rates stay high. More money goes toward interest payments, leaving less room to support the dividend.

Higher rates increase pressureCash Flow Stability

Sustainable dividends are built on dependable cash coming into the business. When cash flow becomes uneven or starts falling, dividend safety becomes much less certain.

Stable cash = stronger dividendIndustry Dynamics

Every sector has its own risks. Telecoms face heavy infrastructure costs, utilities are sensitive to rates and regulation, and commodity companies depend heavily on market cycles.

Different sectors, different risksConclusion — High Yield Is Not Always Safe

Dividend investing can be an excellent strategy for building long-term wealth.

But investors should remember a key principle:

👉 A sustainable dividend is far more valuable than a high but fragile yield.

The five companies discussed in this article — BCE, Telus, Canadian Natural Resources, Canadian National Railway and Emera — remain important players in the Canadian market.

However, analysts are currently monitoring their financial metrics more closely due to factors such as:

• elevated payout ratios

• industry challenges

• interest rate pressure

• commodity price sensitivity

This does not necessarily mean dividend cuts are imminent.

But it does mean investors should pay attention to the underlying fundamentals rather than focusing only on the dividend yield.

In dividend investing, quality and sustainability remain the most important long-term drivers of income and stability.

Educational clause

This article is intended for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell securities. Investors should evaluate their own risk tolerance, investment horizon and financial situation before making investment decisions.